Yen dominated currency moves in an otherwise subdued Asian session, with broad-based selling gathering pace. After weeks of range-bound trading, the Japanese currency may finally be breaking lower, particularly in the crosses where momentum is building.

Trade uncertainty is a central factor. Japan is still waiting for a formal executive order from U.S. President Donald Trump to reduce auto tariffs, a key sticking point in bilateral negotiations. Talks hit another setback last week when Tokyo’s top negotiator abruptly canceled a visit to Washington, leaving no new date on the calendar. Ryosei Akazawa confirmed today that no rescheduling has been arranged. The lack of progress casts doubt on Japan’s hopes for near-term relief, adding pressure to a currency that has already been undermined by shifting policy expectations.

At the same time, a senior BoJ official warned that the risk of a “larger-than-expected impact” from tariffs now deserves greater attention than the prospect of a mild slowdown. With a confirmed trade deal, the BoJ might be able to raise rates again later this year. But without clarity on the tariff front, comments from Deputy Governor Ryozo Himino suggest patience will be required. The central bank looks more likely to wait for stronger confirmation that trade risks are subsiding before adjusting policy again.

As a result, Yen is underperforming across the board, currently the weakest currency of the week. It is followed by Kiwi and Swiss Franc. Sterling leads the pack, followed by Euro and Dollar. Aussie and Loonie are trading mid-range.

Looking ahead, attention will turn to Eurozone CPI flash data and the U.S. ISM manufacturing survey later in the day. Eurozone headline CPI is expected to tick up to 2.1% with core slipping slightly to 2.2%. With inflation hovering near target, the ECB faces little pressure to cut further unless economic activity worsens in response to August’s tariff escalations.

In the U.S., ISM manufacturing is expected to remain in contraction at 48.6, with employment and prices subcomponents drawing close scrutiny. Still, the main event of the week will be Friday’s nonfarm payrolls report, which is poised to shape expectations for the Fed’s September policy move.

In Asia, at the time of writing, Nikkei is down -0.18%. Hong Kong HSI is down -0.67%. China Shanghai SSE is down -1.05%. Singapore Strait Times is up 0.47%. Japan 10-year JGB yield is down -0.018 at 1.607.

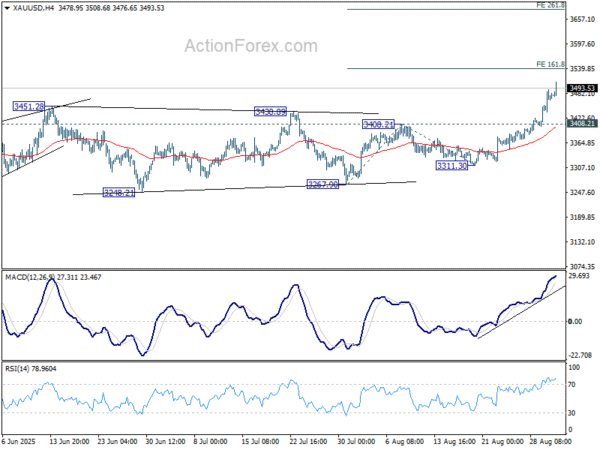

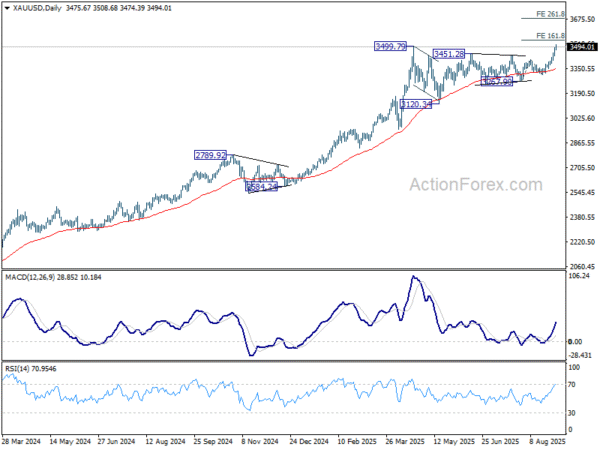

Gold breaks above 3,500, Fed pressure adds fuel

Gold’s rally accelerated this week, surging past 3,500 level for the first time in history. The move reflects growing conviction that the Fed’s rate-cut cycle will extend deep into 2026, eventually bringing policy back to neutral at around 3.00%. With global uncertainty mounting and political interference in Washington intensifying, the precious metal continues to draw strong demand as a hedge.

U.S. President Donald Trump has amplified calls for more aggressive easing, declaring in a social media post that “Prices are WAY DOWN in the USA, with virtually no inflation.” Treasury Secretary Scott Bessent added to the pressure, accusing the Fed of “a lot of mistakes” and backing Trump’s effort to remove Governor Lisa Cook. Bessent also urged swift Senate confirmation of White House economic adviser Stephen Miran to temporarily replace Adriana Kugler, who resigned earlier this month, for the upcoming FOMC meeting this month.

Investors increasingly view Gold as a shield against political intrusion into monetary policy, particularly as institutional frictions grow louder in the run-up to key policy meetings. The combination of dovish expectations and political pressure has fueled the current strong rally.

Technically, while there may be some jitters for Gold at the current 3,500 psychological resistance, near term outlook will stay bullish as long as 3,408.21 resistance turned support holds.

Current rally should target 161.8% projection of 3,267.90 to 3,408.21 from 3,311.30 at 3,538.32 in the near term. Firm break there will pave the way to 261.8% projection at 261.8% projection at 3,678.63 next.

BoJ’s Himino: Risk of larger-than-expected tariff impact warrants focus

BoJ Deputy Governor Ryozo Himino warned in a speech today that U.S. trade policies are likely to weigh on Japan’s economy, with overseas slowdowns and weaker corporate profits feeding through domestically. While accommodative financial conditions should cushion the hit, Himino said the baseline scenario is for Japan’s growth to “moderate,” with downside risks from tariffs deserving greater attention.

Looking further ahead, Himino said Japan’s growth should eventually recover as overseas economies return to a more stable expansion path. But in the near term, the tariff shock remains the key uncertainty, with the risk of a “larger-than-expected impact” now seen as more pressing than the chance of a mild outcome.

On inflation, Himino noted that headline prices remain above the BoJ’s 2% target, by a “considerable margin”, due in part to surging rice prices and spillovers to other goods. However, he stressed headline inflation is expected to “decline in due course” as food-related effects fade. Underlying inflation, meanwhile, remains below target but is steadily rising, despite some potential “temporary halts”, supported by a wage–price feedback loop.

Summing up, Himino said the BoJ’s baseline scenario assumes headline inflation will cool, while core prices continue to edge toward 2%. If that path holds, it would be appropriate for the central bank to keep raising rates gradually, fine-tuning monetary accommodation in line with improving economic activity and stable price gains.

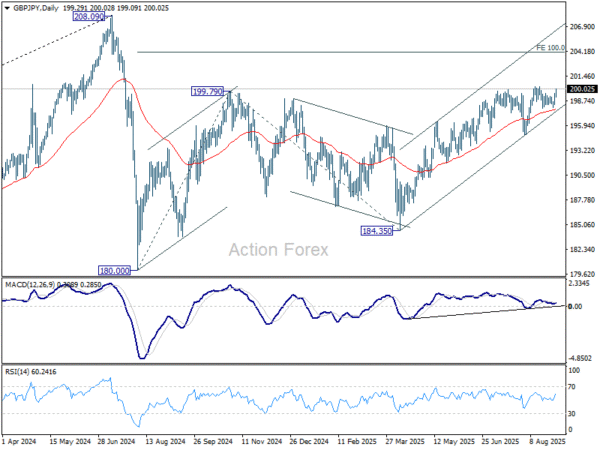

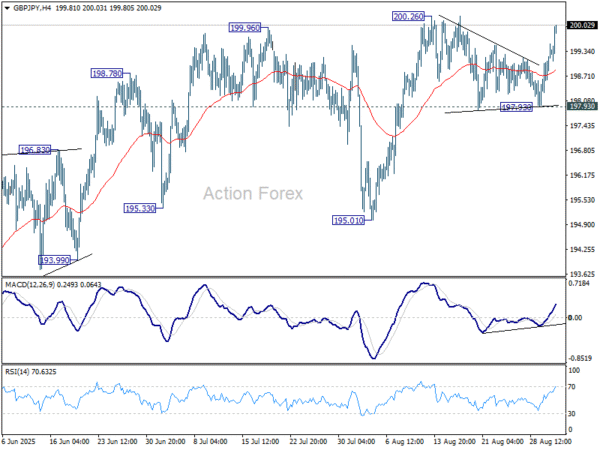

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.65; (P) 199.10; (R1) 199.83; More…

Immediate focus is now on 200.26 resistance in GBP/JPY with today’s strong rally. Firm break there will confirm resumption of whole rise from 184.35, and that from 180.00. Further rally should then be seen to 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, however, break of 197.93 support should confirm short term topping, and turn bias to the downside for 195.01 support next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.