Markets are recovering modestly at the start of the week after last week’s sharp risk-off move. European equities are inching higher, and US futures point to a positive open. While sentiment appears to be improving, the backdrop remains fragile, as reflected in the continued slide in global bond yields, a signal that some investors are still seeking safety.

Yen is among the better performers today, drawing strength from falling yields and lingering caution. Sterling is also relatively firm, supported by weakness in both Euro and Franc. Sterling may face its own test later this week when the Bank of England meets, but for now it is benefiting from cross-asset flows.

Meanwhile, Swiss Franc sits at the bottom of the FX board despite Swiss CPI slightly beating expectations, offering no support to the currency. Euro is not faring much better. Sentix Investor Confidence data painted a grim picture of investor sentiment toward the EU-US trade deal. Dollar remains soft, with attempts to rebound proving shallow so far. Commodity currencies are mixed in the middle.

On the trade front, Japan’s Prime Minister Shigeru Ishiba told the parliament today he is ready have to direct talks with US President Donald Trump to accelerate the implementation of the US auto tariff reduction. Although the deal was struck last month, cutting tariffs on Japanese goods including cars, the timeline remains vague. Trade Minister Akazawa also said in the same session that even under favorable conditions, implementation could take more than a month, as seen in the UK’s case.

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 1.44%. CAC is up 0.99%. UK 10-year yield is down -0.21 at 4.509. Germany 10-year yield is down -0.031 at 2.649. Earlier in Asia, Nikkei fell -1.25%. Hong Kong HSI rose 0.92%. China Shanghai SSE rose 0.66%. Singapore Strait Times rose 1.04%. Japan 10-year JGB yield fell -0.041 to 1.511.

Eurozone Sentix sentiment crashes to -3.7, investors reject US-EU trade deal

Investor confidence in the Eurozone took a sharp hit in August, with Sentix Investor Confidence Index plunging from 4.5 to -3.7, well below expectations of 6.2. Current Situation Index dropped further into negative territory, falling from -7.3 to -13.0. Expectations Index fell steeply from 17.0 to 6.0. Germany’s figures were even more troubling: the overall index dropped from -0.4 to -12.8, with the Current Situation down from -18.8 to -29.0 and Expectations collapsing from 19.8 to 5.0.

According to Sentix, the sentiment collapse reflects investors’ early judgment of the EU-US tariff deal — and the assessment is “devastating.” The agreement, instead of offering clarity or relief, has triggered renewed concerns about Eurozone export sectors. Recent optimism about Germany’s recovery is now in doubt, with export-oriented industries seen facing more pressure in the months ahead. Investors are also increasingly anxious about rising government debt across the bloc.

Adding to the gloom, inflation shows no signs of easing. Sentix’s inflation theme index fell to -11.75, reinforcing the view that the ECB has limited room to ease policy further. With sentiment deteriorating, debt concerns mounting, and no clear inflation relief in sight, the Eurozone’s path to recovery looks increasingly fragile.

Swiss CPI beats forecast, easing pressure on SNB to go negative

Swiss CPI came in firmer than expected in July, with headline inflation unchanged mom versus forecasts of a -0.2% mom decline. Core CPI — which excludes fresh and seasonal products, energy, and fuel — fell slightly by -0.1% mom, while domestic product prices rose 0.2% mom and imported product prices dropped -0.9% mom.

On an annual basis, headline CPI ticked up to 0.2% yoy from 0.1% yoy, also ahead of the 0.1% yoy forecast. Core CPI accelerated from 0.6% yoy to 0.8% y/y yoy. Domestic product inflation remained steady at 0.7% yoy, while imported product prices, although still negative, improved from -1.9% yoy to -1.4% yoy.

Today’s data modestly ease concerns that Switzerland is slipping back into outright deflation. There has been persistent speculation that the SNB might resume negative interest rates following a series of cuts that brought the policy rate back to 0.00%. But July’s inflation uptick may buy policymakers time ahead of the next meeting on September 25.

In the background, the slight weakening in Swiss Franc, as global markets stabilize and trade tensions ease, helps reduce deflationary pressure. If August CPI data show further improvement, expectations will likely shift toward a steady hold in September rather than another policy adjustment.

GBP/CAD faces dual event risk of BoE and Canadian job

GBP/CAD could see heightened volatility this week as two key events take center stage: BoE rate decision on Thursday and Canadian employment data on Friday.

A 25bps BoE cut is widely expected as part of its measured easing cycle, but the decision may not be smooth. In May, the MPC vote split a rare three ways, with two members backing a larger cut and two pushing for no change. In June, Deputy Governor Dave Ramsden joined the dovish camp. But with inflation unexpectedly accelerating, some policymakers may reverse course. That raises the odds of a more contentious outcome, potentially sparking a reaction in GBP crosses.

Canadian Dollar, meanwhile, will look the July jobs report for direction. BoC has left rates unchanged for three straight meetings and hinted it may cut only if weakness persists. June’s robust job data — 83.1k positions added and a dip in unemployment to 6.9% — gives the BoC space to stay on hold for longer. A solid print this week would reinforce that view.

Technically, GBP/CAD remains under pressure as decline from 1.8830 continues. Momentum has slowed, as seen in 4H MACD, but there’s no clear sign of a bottom yet. The decline is seen as the third leg of the corrective pattern from 1.8777, and further dip toward 1.7980 cannot be ruled out. On the other hand, firm break above 1.8484 would suggest the fall is over and open a move back toward 1.8830.

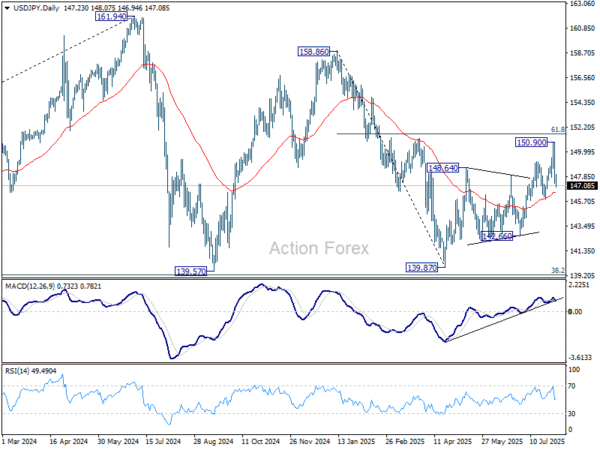

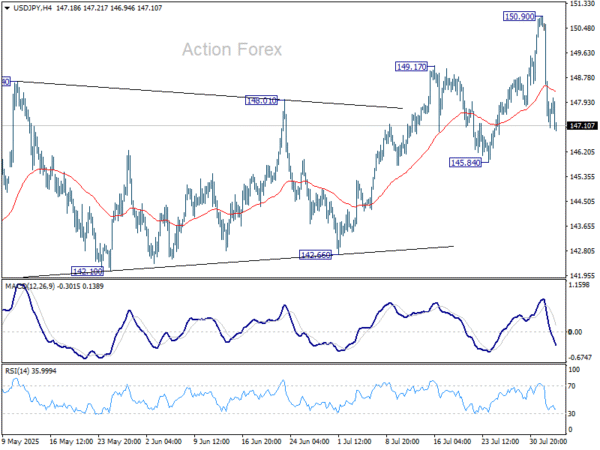

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.17; (P) 148.54; (R1) 149.80; More…

USD/JPY dips mildly today but stays well above 145.84 support. Intraday bias stays neutral first. Rebound from 139.87 could still extend higher. Above 150.90 will target 151.22 fibonacci level. However, on the downside, firm break of 145.84 support will argue that whole rise from 139.87 might have already completed. Deeper fall should then be seen to 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.