Australian and New Zealand Dollars fell sharply to start the week, leading losses alongside Yen. The moves come just ahead of central bank meetings in both countries, with RBA widely expected to cut rates by 25bps to 3.60% and RBNZ likely to hold at 3.25%. But given how well those outcomes are priced in, the sharp declines are more tied to a sharp escalation in US-led trade threats, which now openly target nations aligned with the BRICS economic bloc.

US President Donald Trump and Treasury Secretary Scott Bessent confirmed over the weekend that unilateral tariffs first announced in April will take effect August 1 for countries that have not finalized deals with the US The warning comes alongside new “take-it-or-leave-it” letters being sent to trading partners, with a clear message: accept the revised deal or revert to harsher April 2 tariff rates.

Adding fuel to the risk-off tone, Trump explicitly warned that any country aligning itself with BRICS “anti-American policies” will face an additional 10% tariff. That’s a direct signal to countries like Australia and New Zealand, which maintain strong trade ties with China, India, and Indonesia—all key BRICS or BRICS-aligned nations. Markets are increasingly viewing the region as vulnerable to secondary economic fallout if bilateral relations deteriorate further.

Currency markets quickly repriced exposure. Dollar led gains, followed by Euro and Swiss Franc, as investors rotated toward perceived safety. AUD and NZD were the worst performers, with Yen not far behind. Sterling and Canadian dollar held near the middle of the pack .

Technically, while today’s decline in NZD/USD is steep, it’s not yet structurally damaging. Deeper pullback might be seen but near term outlook should stay bullish as long as 0.5802 cluster support holds (38.2% retracement of 0.5484 to 0.6119 at 0.5876 holds. Rally from 0.5484 is still in favor to resume at a later stage.

In Asia, at the time of writing, Nikkei is down -0.53%. Hong Kong HSI is down -0.45%. China Shanghai SSE is down -0.21%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.018 at 1.453.

Japan real wages post sharpest drop Since 2023 as bonuses shrink

Japan’s real wages fell -2.9% yoy in May, a sharp acceleration from April’s -2.0% drop yoy and the steepest decline since September 2023. This also marks the fifth consecutive monthly fall in inflation-adjusted income, as households remain squeezed by rising prices and underwhelming nominal pay growth. Consumer inflation, used to deflate nominal wages, stood at 4.0% yoy, driven by higher food costs, particularly rice.

Nominal wages rose just 1.0% yoy, well short of the 2.4% yoy forecast and down from 2.0% yoy in April. While base salary growth held at 2.0% yoy and overtime pay rose 1.0% yoy, a sharp -18.7% yoy plunge in special payments—largely one-off bonuses—dragged down the overall figure. May marked the 41st consecutive monthly rise in nominal wages, but the pace failed again to keep up with price growth.

Government officials cautioned that the wage data may not yet reflect the full impact of spring labor negotiations, especially as many small firms surveyed lack unions and implement pay increases more slowly than large corporations. Nonetheless, the prolonged real wage squeeze could weigh on consumer spending and affect BoJ’s plans to gradually normalize policy.

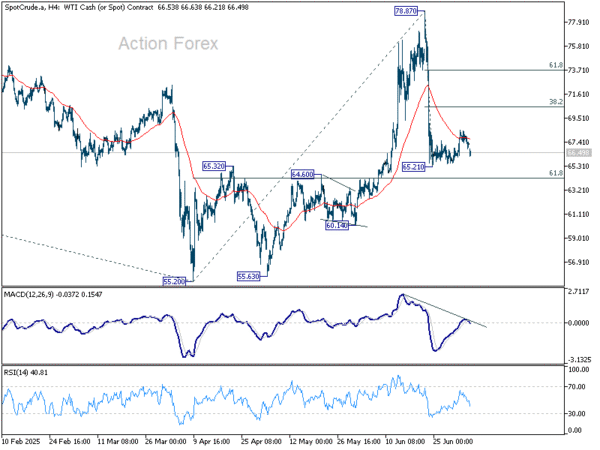

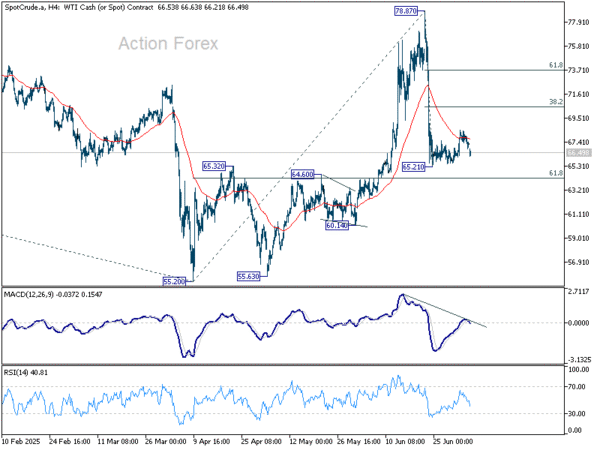

OPEC+ raises supply by 548k bpd, WTI dips mildly in range

OPEC+ surprised markets over the weekend by agreeing to boost crude production by 548k bpd barrels in August, outpacing expectations for a more modest 411k bpd increase. The alliance said the move reflects confidence in “a steady global economic outlook and healthy market fundamentals,” noting that inventories remain low.

WTI crude dipped slightly at the Monday open but continues to hold above its short-term bottom at 65.21. Price action remains consolidative, and a near-term bounce is possible, though gains are likely to be capped by 38.2% retracement of 78.87 to 65.21 at 70.42. The main question is whether 61.8% retracement of 55.20 to 78.87 at 64.24 could hold as fall from 78.87 resumes later.

While OPEC+ is leaning into demand strength, the market appears cautious about upside potential given rising supply and uncertain macro drivers.

RBA to cut, RBNZ to hold, FOMC minutes also watched

Two central banks will take center stage this week, with RBA expected to resume easing while the RBA likely holds steady.

Markets are positioning for a 25bps rate cut from RBA to 3.60%, and the key focus will be whether Governor Michele Bullock signals a faster pace of easing ahead as inflation recedes and economic activity slows.

A Reuters poll conducted between June 30 and July 3 showed that 23 of 36 economists expect RBA to cut rates to 3.35% this quarter, with many major banks forecasting August as the likely window. ANZ, Commonwealth Bank, and NAB all expect a cut to 3.35% in August, while NAB sees further easing to 3.10% by year-end. Westpac also anticipates 3.35%, but sees that level reached by December.

RBA’s tone will be decisive in shaping market expectations. If policymakers suggest that the disinflation trend is durable and growth risks are mounting, markets may begin pricing in more aggressive cuts, particularly if domestic demand shows further signs of stalling. AUD could soften if guidance points to an accelerated easing path.

In contrast, RBNZ is expected to keep its official cash rate unchanged at 3.25% at its July 9 meeting. The central bank has already delivered 225bps of cuts since August 2024, supporting an economy that exited recession late last year. GDP rose 0.8% in Q1, giving RBNZ room to pause and assess new data before deciding on further moves.

According to a separate Reuters poll, 19 of 27 economists forecast no change this week, with only eight expecting a cut. All major New Zealand banks expect rates to remain on hold. While inflation data has been mixed, policymakers are likely to wait for clearer signals on inflation expectations before acting in August.

In the US, the FOMC minutes from the June meeting are unlikely to shift market expectations. With a solid June NFP print behind them, Fed futures price near-zero odds of a July cut. Although Governors Christopher Waller and Michelle Bowman have signaled more dovish leanings recently, the broader Committee remains cautious amid tariff and fiscal uncertainties.

The ultimate shape of the Fed’s easing cycle—whether two cuts as implied in the dot plot, or fewer—will hinge more on how the tariff situation evolves after the truce ends than on debates at the June meeting.

Markets will also keep an eye on incoming data including UK and Canadian GDP, China CPI, and Eurozone Sentix confidence for broader macro signals.

Here are some highlights for the week:

- Monday: Japan labor cash earnings; Germany industrial production; Swiss foreign currency reserves; Eurozone Sentix investor confidence, retail sales.

- Tuesday; Australia NAB business confidence, RBA rate decision; Germany trade balance; France trade balance; Canada Ivey PMI.

- Wednesday: China CPI, PPI; RBNZ rate decision; FOMC minutes.

- Thursday: Japan PPI; US jobless claims.

- Friday: New Zealand BNZ manufacturing; Germany CPI final; UK GDP, trade balance; Swiss SECO consumer climate; Canada employment.

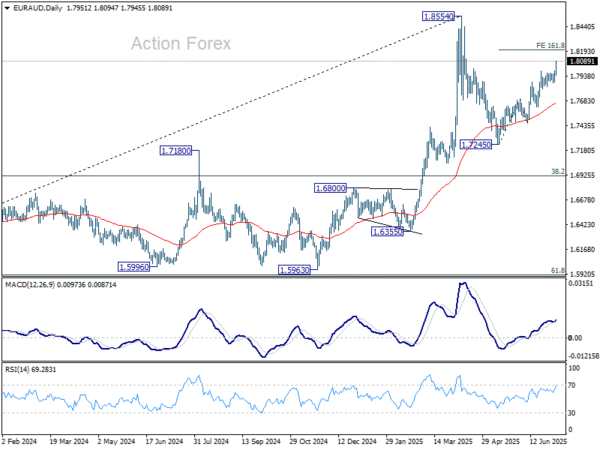

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7905; (P) 1.7950; (R1) 1.8019; More…

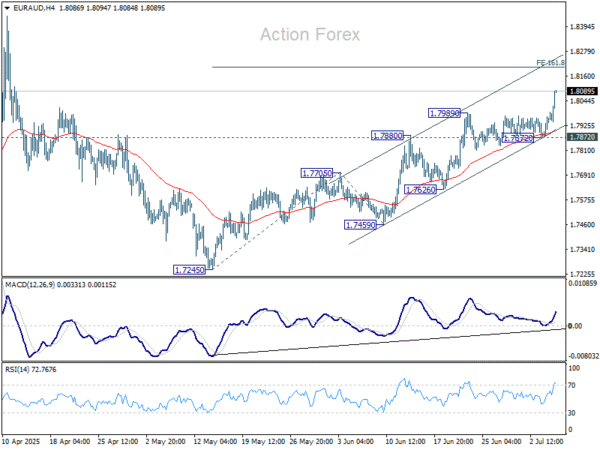

EUR/AUD’s rally from 1.7245 resumed by breaking through 1.7989 resistance decisively. Intraday bias is back on the upside. Next target is 161.8% projection of 1.7245 to 1.7705 from 1.7459 at 1.8203. Firm break there will target 1.8554 resistance. For now, further rise will remain in favor as long as 1.7872 support holds, in case of retreat.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.