Risk appetite has remained firm across global equities this week, with NASDAQ hitting a fresh record high overnight and S&P 500 and DOW also closing in the green. These gains followed similar moves in Europe, where Germany’s DAX notched another record. However, the mood in Asia has been less upbeat. Japan’s Nikkei slipped into negative territory, pressured by concerns over US tariffs. The 25% duty imposed on Japanese goods has clearly weighed on sentiment, contrasting with the broader global resilience.

In the currency markets, price action has been more muted. Dollar remains the strongest major currency for the week, but it’s beginning to show signs of a near-term reversal. The latest FOMC minutes revealed a deeply divided committee, with some members focused on rising inflation risks while others remain concerned about a weakening labor market and activity — a classic reflection of stagflation worries. This policy split is understandable, given the uncertain economic impact of tariffs and how they could simultaneously push prices higher while dampening demand.

Outside Dollar, the Swiss Franc and Aussie are gaining ground, eyeing a takeover in relative strength rankings. Yen is the weakest, hurt by tariffs. Kiwi and Loonie are also underperforming, while Euro and pound are stuck in the middle.

On the trade front, tensions escalated further. US President Donald Trump informed Brazil that its “reciprocal” tariff would rise from 10% to 50% effective August 1, citing national security concerns and referencing Brazil’s handling of former President Bolsonaro’s prosecution. Brazilian President Luiz Inácio Lula da Silva pledged to respond in kind, invoking a new economic reciprocity law that permits countermeasures. Lula’s strongly worded response emphasized Brazil’s sovereignty and refusal to accept external pressure.

Trump also confirmed a new 50% tariff on all US copper imports starting August 1, citing a Section 232 national security review. The move sent copper prices sharply higher, though near-term technicals suggest the rally may be losing steam. Meanwhile, US–EU negotiations are ongoing, with reports of potential compromises on auto tariffs through quota limits, tariff reductions, or credit systems aimed at shielding European carmakers.

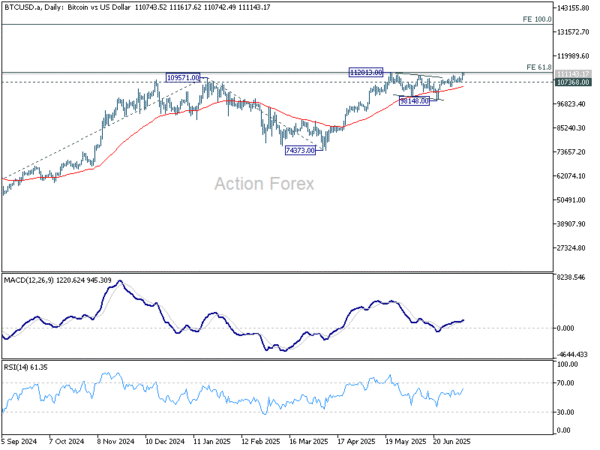

Technically, Bitcoin made a new record high by a hair today but struggles to extend rally. Nevertheless, near term outlook will stay bullish as long as 107368 support holds. Sustained trading above 61.8% projection of 49008 to 109571 from 74373 at 111800 will pave the way 100% projection at 134946. However, break of 107368 will delay the bullish case and bring more consolidations.

In Asia, at the time of writing, Nikkei is down -0.66%. Hong Kong HSI is up 0.36%. China Shanghai SSE is up 0.66%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is down -0.015 at 1.492. Overnight, DOW rose 0.49%. S&P 500 rose 0.61%. NASDAQ rose 0.94%. 10-year yield fell -0.073 to 4.342.

Fed minutes reveal deep division on rate path

Minutes from the FOMC’s June 17–18 meeting highlighted a notable divergence among policymakers on whether rate cuts are needed this year. “Most participant” still see at least one cut as likely, citing temporary tariff effects, stable inflation expectations, and signs of cooling in the labor market. “A couple” went further, indicating they would be open to a rate cut at the upcoming July meeting if economic data confirms their outlook.

However, “some participants” pushed back against easing and suggested “”no reductions” this year, pointing to stubbornly high inflation and warning of upside risks. They argued that “upside risks to inflation remained meaningful”, with businesses and consumers still expecting higher prices, and with economic activity holding up, rate cuts could be premature. Several added that “may not be far above its neutral level”, diminishing the case for near-term action.

Participants generally agreed that risks of both elevated inflation and a weakening labor market have eased somewhat, but remain elevated. “Some” emphasized inflation risks as still “more prominent”, while “a few” flagged labor market deterioration as the more pressing concern. The broad message from the minutes was one of uncertainty, with many policymakers seeing the need take a “careful approach” in adjusting monetary policy.

Japan’s PPI slows to 2.9% yoy in June, stronger Yen helps ease import costs

Japan’s Producer Price Index rose 2.9% yoy in June, easing from May’s 3.3% yoy pace and in line with expectations. The slowdown reflects a moderation in upstream price pressures, as firms begin to benefit from a firmer Yen.

Yen-based import price index dropped -12.3% yoy from a year earlier, deepening from May’s -10.3% yoy fall and signaling that Japan’s currency rebound is dampening raw material costs. Food and beverage prices remained elevated with a 4.5% yoy increase, largely due to persistently high rice costs, though that was slightly softer than the prior month’s 4.7% yoy rise.

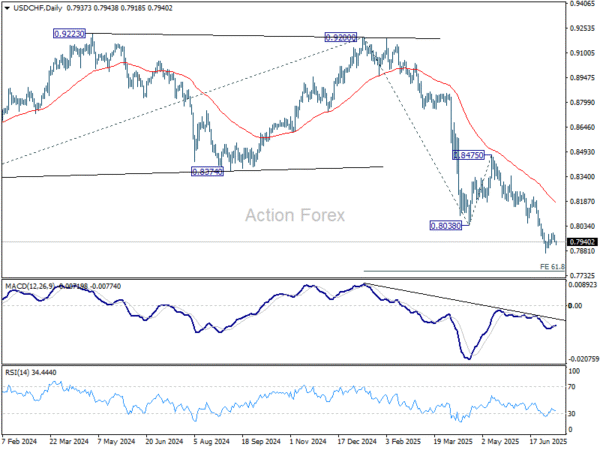

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7954; (R1) 0.7968; More….

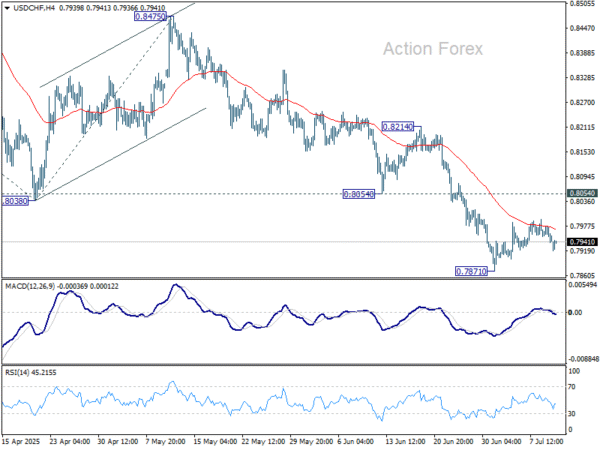

USD/CHF dipped after rejection by 55 4H EMA but stays above 0.7871 support. Intraday bias remains neutral for the moment. Consolidations could extend and another rise cannot be ruled out. But , upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.