Euro strengthened notably against Sterling and Swiss Franc as expectations for a September rate cut from the ECB began to fade. Some analysts now see October as a more likely timing, after President Christine Lagarde maintained an optimistic outlook during her post-decision press conference yesterday. Lagarde emphasized that June’s baseline forecasts remain valid, even amid US tariff threats. Latest improvement in July’s services PMI also reduced the urgency for another near-term cut.

In the US, Dollar clawed back modest ground following signs that Fed Chair Jerome Powell’s job is safe—at least for now. During a symbolic visit to the Fed, US President Donald Trump reiterated his frustration with Powell’s reluctance to cut rates but walked back threats of dismissal. Trump said that firing the chair would be “a big move” and likely unnecessary. The shift eases some institutional risk concerns that had weighed on the greenback.

Meanwhile, Australia’s decision to allow US beef imports marks another bright spot in global trade relations. Australian Agriculture Minister Julie Collins noted that biosecurity concerns have been addressed through improved US monitoring systems. Trump welcomed the move, touting it as a win for American ranchers and a sign of stronger US-Australia ties.

Overall for the week so far, Yen is currently the strongest one, followed by Kiwi, and then Euro. Dollar remains at the bottom, followed by Loonie, and then Sterling. Swiss Franc and Aussie are positioning in the middle. Risk-on sentiment appears to be receding.

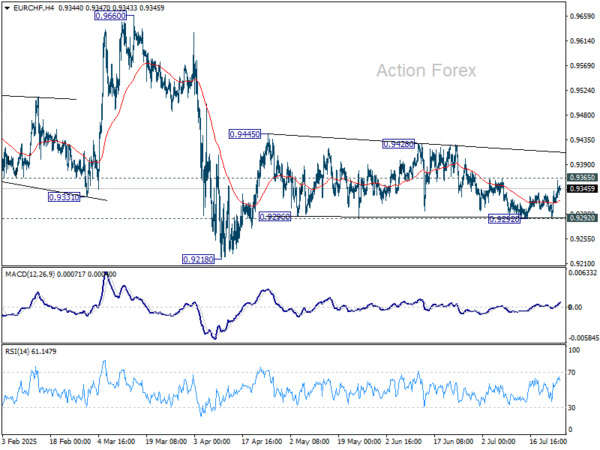

Technically, a focus today is on 0.9365 resistance in EUR/CHF as near term rebound extends. Firm break there will argue that corrective pattern from 0.9445 might have finally completed at 0.9292. Retest of 0.9428/9445 resistance zone should be seen next. Firm break there will resume the rebound from 0.9218.

In Asia, at the time of writing, Nikkei is down -0.87%. Hong Kong HSI is down -0.87%. China Shanghai SSE is down -0.25%. Singapore Strait Times is down -0.35%. Japan 10-year JGB yield is down -0.008 at 1.595. Overnight, DOW fell -0.70%. S&P 500 rose 0.07%. NASDAQ rose 0.18%. 10-year yield rose 0.02 to 4.408.

Tokyo CPI core slows to 2.9%, but stays elevated

Tokyo’s core CPI (ex-fresh food) eased slightly from 3.1% to 2.9% yoy in July, coming in just below expectations of 3.0% yoy, but still notably above the BoJ’s 2% target.

Headline inflation also slowed from 3.1% yoy to 2.9% yoy. Core-core measure—excluding fresh food and energy—held steady at 3.1%. The stickiness in core-core inflation highlights persistent underlying price pressures.

The figures will feed into the BoJ’s upcoming July 30–31 policy meeting, where the board is widely expected to upgrade its inflation forecast for the current fiscal year. While the data alone may not push the BoJ to act immediately, it strengthens the case for further normalization as inflation remains well above target.

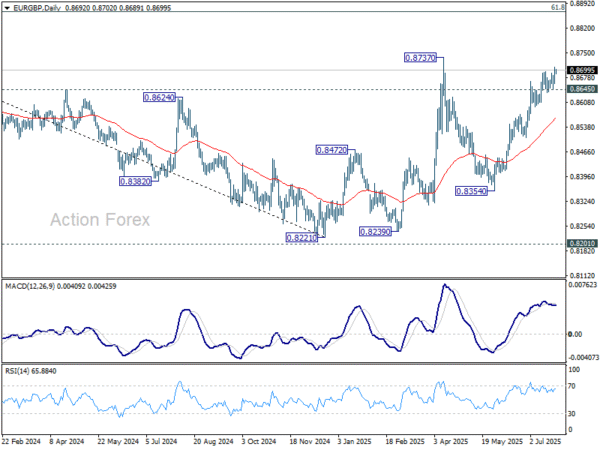

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8672; (P) 0.8691; (R1) 0.8716; More…

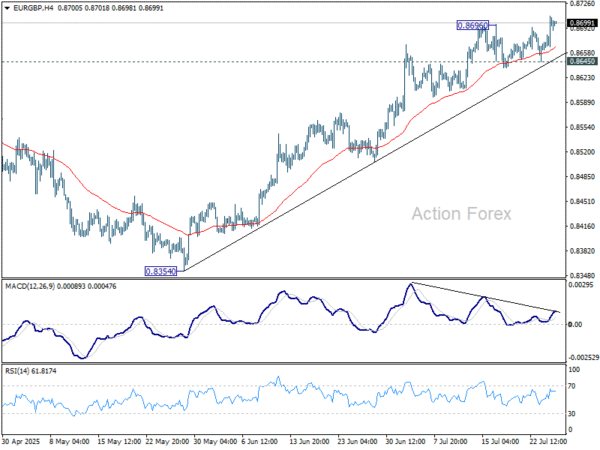

EUR/GBP’s rise from 0.8354 resumed by breaking 0.8696 resistance and intraday bias is back on the upside. Further rally should be seen to retest 0.8737 high. Firm break there will extend the rise from 0.8221 towards 0.8867 fibonacci level. On the downside, however, break of 0.8645 will suggest short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the down trend from 0.9267 (2022 high). But even if it’s a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. For now, further rise will remain in favor as long as 55 W EMA (now at 0.8474) holds.