A strong wave of risk appetite is sweeping through global markets, with equities gaining ground across the board. Major European indexes are firmly higher, Japan’s Nikkei marked its second straight record close, and US futures are pointing to another day of record highs for S&P 500 and NASDAQ. Investors are finding comfort in a mix of supportive policy narratives.

In the US, Treasury Secretary Scott Bessent again pressed for an outsized move from the Fed at its September meeting. In a Bloomberg interview today, he argued that poor-quality US jobs data earlier this year delayed necessary rate cuts and suggested that, had the data been more accurate, easing could have begun months ago. He placed the odds of a 50 basis point cut at “very good”.

Bessent further said the Fed could embark on a “series” of cuts starting next month, and eventually rates should be lowered by as much as 150-175 basis points in total. That makes his stance far more aggressive than current market expectations. Futures markets still overwhelmingly price a 25 basis point move next month, with little shift toward the larger cut Bessent is advocating.

From Asia, China unveiled a new program to stimulate consumption by offering interest subsidies on loans to households and businesses. Vice Finance Minister Liao Min said the policy aims to strengthen domestic demand as a key driver of growth, targeting both consumer sectors and service industries. The move comes as Beijing looks to bolster the economy without putting undue pressure on bank profitability.

The scheme will provide a one percentage point annual interest subsidy on eligible loans in eight consumer service sectors and for personal borrowing. Crucially, the government—not the banks—will bear the subsidy cost, in contrast to prior measures that forced lenders to lower rates directly. This approach should preserve bank margins while encouraging greater credit uptake.

On the FX side, Dollar is bearing the brunt of today’s risk-on tone, sliding to the bottom of the performance table alongside Loonie and Yen. Kiwi is out front, with Sterling and Swiss Franc also firm. Euro and Australian Dollar are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.80%. CAC is up 0.57%. UK 10-year yield is down -0.013 at 4.616. Germany 10-year yield is down -0.041 at 2.706. Earlier in Asia, Nikkei rose 1.30%. Hong Kong HSI rose 2.58%. China Shanghai SSE rose 0.48%. Singapore Strait Times rose 1.23%. 10-year JGB yield rose 0.021 to 1.521.

EUR/USD clears 1.17, Trump’s lawsuit threat against Powell adds to Dollar’s woe

Dollar’s selloff gathered pace in European trading, with EUR/USD breaking above the 1.17 mark and appearing ready to retest 1.1829 short-term top. Momentum in the pair reflects broad pressure on the greenback, though Fed rate expectations have shifted only modestly.

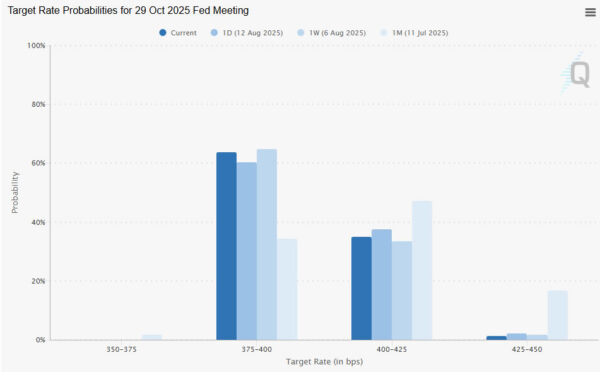

Markets now assign a 96.22% probability to a 25bps cut at the September FOMC, up slightly from 94.59% a week ago. Odds of a follow-up move to 3.75–4.00% stand at 63.77%, even slightly lower than last week’s 64.71%. This muted change suggests that neither US President Donald Trump’s political pressure nor Treasury Secretary Scott Bessent’s call for a 50bps cut have meaningfully shifted rate expectations.

Instead, Dollar weakness may be more closely tied to concerns over Fed’s institutional credibility. White House press secretary Karoline Leavitt confirmed Tuesday that Trump is “considering a lawsuit” against Fed Chair Jerome Powell. The president also attacked Powell on social media, blaming him for being “Too Late” in policy decisions and criticizing what he claimed was a USD 3B overspend on Fed building renovations.

The political rhetoric raises questions about perceived threats to the Fed’s independence, a factor that could be weighing on the currency even more than rate speculation. The potential legal action, while unprecedented, may be seen as part of a broader effort to influence monetary policy direction ahead of upcoming meetings.

Technically, EUR/USD’s rally from 1.1390 has resumed with a break above 1.1698. The next target is a retest of the 1.1829 resistance,. Decisive break there would resume the medium-term uptrend.

More importantly, the next leg higher would bring the pair to face a long-term resistance zone around 1.20. This includes the 38.2% retracement of the 1.6039 (2008 high) to 0.9534 (2022 low) at 1.2019. Sustained break would strengthen the case that the rise from 0.9534 is the start of a long-term uptrend reversing more than 14 years of prior decline.

ECB Vice President Luis de Guindos remarked in early July that an exchange rate of 1.17–1.20 is “perfectly acceptable” but suggested that moves beyond $1.20 could pose complications, particularly in terms of deflationary pressures. This makes 1.20 a critical line to watch — both technically and from a policy perspective — in the weeks ahead.

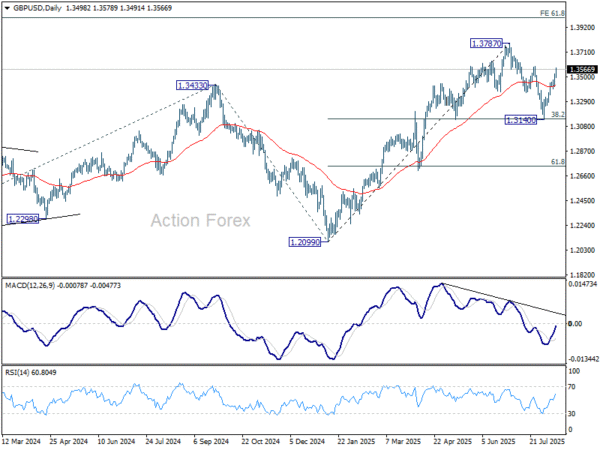

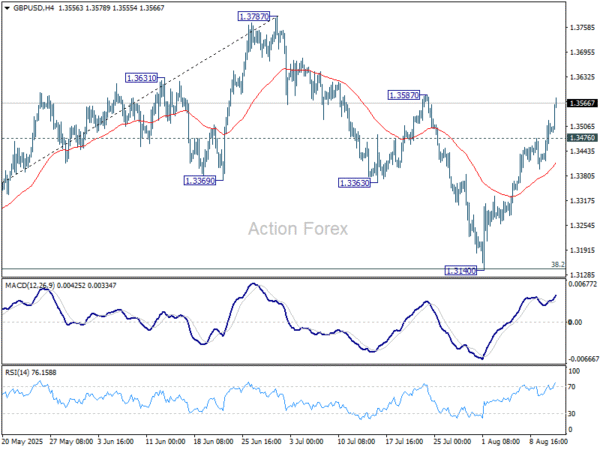

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3438; (P) 1.3481; (R1) 1.3543; More…

GBP/USD’s rally from 1.3140 re-accelerates higher today and intraday bias stays on the upside. Correction from 1.3787 should have completed with three waves down to 1.3140. Firm break of 1.3587 will bring retest of 1.3787 high. On the downside, below 1.3476 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3068) holds, even in case of deep pullback.