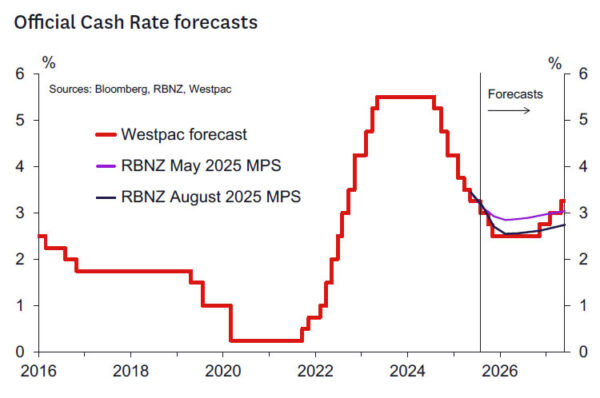

- The RBNZ reduced the OCR by 25bps to 3.00% as expected.

- But the forward guidance was very dovish – 1.5 cuts by year end are projected.

- The decision was reached following a 4 – 2 vote on the options of a 25bp vs 50bp cut – emphasising the significant shift in strategy.

- The RBNZ unexpectedly made large cuts to the near-term growth view – 1.6% growth is now expected in 2025, some way south of our own 2.4% estimate.

- The Governor said there was comfort around the midpoint of the new forecasts but more of a deviation of views around the balance of risks.

- Westpac expects two further 25bp cuts this year and the OCR to trough at 2.5% from there.

- We retain the view that interest rates will rise from at least the end of 2026 – we will review the timing further in coming months.

Key messages from the RBNZ today.

As was widely expected and almost fully priced by the market, today the RBNZ announced a further 25bps reduction in the OCR to 3.0%. However, in a dovish surprise to the market, two of the six committee members voted for a 50bps cut, and the revised projections lowered the terminal rate by 30bps to 2.55% (versus 2.85% in their previous forecasts).

The following are the key take-outs from the record of meeting:

- The OCR forecast of 2.71% for the December quarter implies at least one cut in the OCR at the next meeting in October, with around a 50% chance of a follow-up cut at the November meeting.

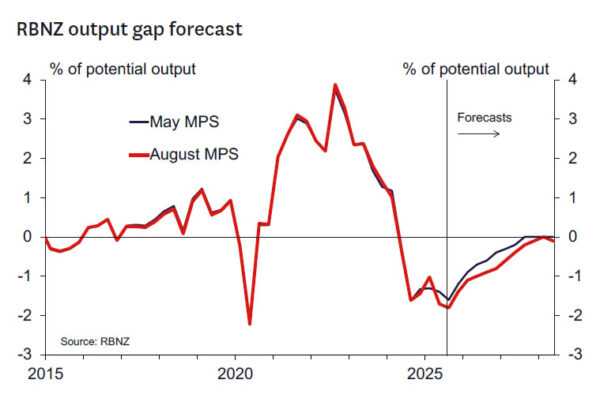

- The RBNZ estimates that economic activity contracted 0.3% in the June quarter and expects that growth will remain subdued in the September quarter (forecast: +0.3% qtr). The resulting output gap is more negative in the near term than forecast in May, despite the positive growth surprise in Q1.

- While the impact of uncertainty about the impact of global conditions is expected to be a little less persistent than previously assumed, this is still expected to be a drag on business investment and household spending.

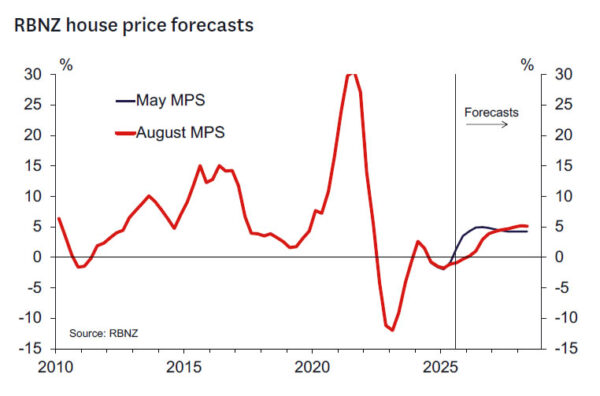

- Some members expressed concern with the speed of monetary policy transmission, with the record noting that: “Some members also drew attention to slow growth in parts of the economy that are most sensitive to interest rates. Residential construction, house prices, and retail activity have not materially recovered, despite monetary easing to date”.

- The RBNZ significantly revised down its forecast for house price inflation and noted that: “Ongoing weakness in the housing market is contributing to subdued residential construction and household consumption.”

- Recent weakness in the labour market also appears to have been factored in: “The Committee discussed constraints on household wealth and discretionary income. Employment and hours worked have declined, and wage inflation has slowed sharply over the last year.”

- The RBNZ acknowledged the support provided by high export commodity prices: “High commodity export prices are supporting activity in the agricultural sector, resulting in stronger spending in rural areas. However, to date, many agricultural businesses have used higher export revenues to pay down debt, limiting the passthrough to consumption and investment.”

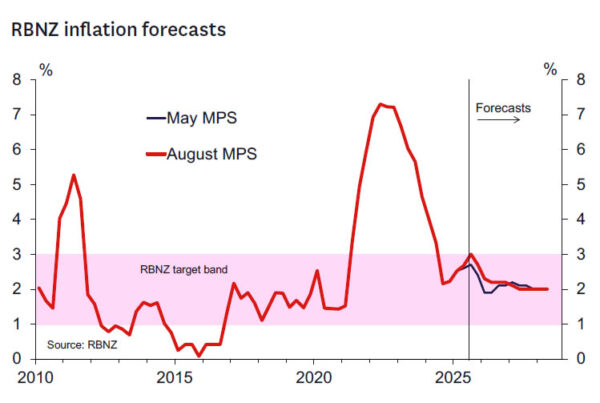

- Regarding inflation, the record notes: “On a quarterly basis, non-tradables inflation excluding central and local government charges is consistent with inflation at or below the target mid-point. Some members suggested that this may represent a downside risk to medium-term inflation.”

- With respect to the global environment, the RBNZ notes that: “Some members emphasised the fact that some measures of uncertainty have improved considerably since May and noted a possibility that the domestic economy recovers more rapidly as the effects of uncertainty dissipate. Other members highlighted that excess supply in China and some parts of emerging Asia has the potential to lower tradable inflation in New Zealand over the medium term.”

- The risk distribution around the baseline forecast is viewed as balanced: “Some members considered the balance of risk [to the OCR] to be to the upside relative to the projected path, while others considered the balance of risk to be to the downside.”

Westpac’s view on the policy outlook.

The RBNZ seems set on taking the OCR significantly lower and the bar for a pause in the meetings before Christmas seems high. The RBNZ would have expected that presenting such a low OCR forward track would lead markets to conclude cuts in October and November were likely, and we certainly take on board that message.

This is an occasion where the data doesn’t really tell the story. What we have here is a change in strategy where the RBNZ is choosing to look through the CPI inflation outlook for the next six months and instead take action to underwrite an improvement in growth. The RBNZ likely won’t move away from this insurance strategy until totally comfortable that the economy is on track to grow at rates that will eliminate the current spare capacity.

The story seems to be one where there are concerns that the output gap will be much more negative in the second half of 2025 and take longer to close. This is being driven by a combination of economic uncertainty (mentions of uncertainty have not declined in the August Statement relative to May) and, in the eyes of some MPC members, the idea that interest rates are not having the leverage expected. The weaker housing market profile is part of that picture.

We likely won’t see evidence of any decisive bounce in growth towards trend in the Q2 GDP data, which is due in September – although we expect to see a bounce in some of the more sentiment driven-indicators (business confidence, PMIs, perhaps the housing market) in the next few months.

Our forecasts for CPI inflation are notably higher than the RBNZ’s for the next six months. We see the September quarter CPI at 1.1% vs the RBNZ’s 0.9%, and we expect inflation over calendar 2025 will print at 3.1% vs the RBNZ’s forecast for 2.7%. But the RBNZ doesn’t seem to be very focused on that. Some MPC members advocating a less dovish approach noted risks to inflation expectations. But while we will see little information on that before October, there will be more in November. We think this is a big risk to the MPC’s strategy and could be relevant for the November Statement.

We noted in our recent Hawks and Doves note that historically the OCR has moved 50-125bp below neutral in a non-crisis cycle. The OCR at 2.5% would bring the OCR into that range based on the RBNZ’s estimates (these still range between 2.9-3.5%). Policy will be clearly stimulative on our own estimate of a 3.75% neutral OCR.

It’s prudent to assume a 25bp cut in October. Another cut in November also seems more likely than not. But there is a lot more water to go under the bridge between now and November. The RBNZ has clearly signalled they will be data dependent.

Key data and events before the RBNZ’s October meeting.

Looking ahead to the RBNZ’s next policy review on 8 October, the key domestic data and events will be:

- The August Selected Price Indexes (16 September): This will provide further insight regarding the likely outcome of the Q3 CPI report, which will not be released until 20 October. • The Q2 GDP report (18 September): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum.

- The Q3 QSBO survey (7 October): The focus in this report will be on indicators of Q3 activity, capacity use and direct measures of cost/selling price pressures.

In addition to the above, key monthly activity indicators such as the BusinessNZ manufacturing and services indexes (mid-September) and the ANZ business and consumer confidence surveys (late August and late September) will also be of interest, as will the monthly retail spending and housing market reports (mid- September). Indicators relating to the labour market will likely be tracked especially closely. Should it occur, a lift in filled jobs and job advertising would provide some reassurance that the recovery is becoming selfsustaining. Inflation expectations measures from the ANZ’s business and consumer surveys will also be monitored see whether their recent lift has endured.

Outside of New Zealand, interest will clearly centre on any clarity that emerges regarding the final form of US tariff policy and its implications for growth in New Zealand’s major trading partners, the outlook for key export commodity prices and the prices of goods imported into New Zealand. Decisions taken by the US Federal Reserve will also be of importance to the extent that they impact financial conditions in New Zealand, including the behaviour of the exchange rate.

Finally, it is also worth noting that there will likely be a new external member of the MPC in place at the October OCR review (replacing Professor Bob Buckle, whose term ended with the August meeting). It is also possible that we may have a new RBNZ Governor in place, although it seems more likely that this will happen between the October and November meetings. New personnel with potentially different perspectives and judgments mean that the policy outlook could shift even if the data flow falls in line with the projections in the August MPS.