Market headlines are thin today, with Japan stealing the spotlight as the Nikkei saw a steep pullback following yesterday’s record-setting close. The drop appears driven by traders cashing in on an extended rally rather than any shift in economic outlook. Fundamentally, Japanese equities remain supported, with the economic fallout from US tariffs proving milder than many had feared.

With major trade risks out of the way, Japan’s economy looks increasingly well-positioned to escape its decades-long battle with deflation for good. That structural optimism, however, did not stop short-term traders from locking in gains, leading to a pullback that has triggered a notable rebound in Yen. The Japanese currency is currently the day’s best performer, fueled by a combination of risk position adjustments and the Nikkei retreat.

Aussie is the second strongest performer, supported by solid employment figures released earlier in the day. While the job gain came in just below expectations, the composition of the data—highlighted by a strong rise in full-time employment—points to a labor market that is softening gradually rather than facing a sharp downturn.

One key takeaway from the numbers is that the unemployment rate remains slightly below RBA’s estimated full employment level of 4.3%. This reinforces the view that the central bank is in no rush to accelerate its easing cycle. Instead, policymakers are likely to stick to a measured and gradual approach to further rate cuts.

On the weaker side of the currency spectrum, Sterling is the day’s worst performer, though the move largely reflects a modest pullback after recent strong gains. Traders will look to upcoming UK GDP figures for fresh direction. Euro is the second weakest, followed by D, which will face its next test with today’s PPI data and jobless claims releases. The Swiss Franc and Loonie are trading mixed.

In Asia, at the time of writing, Nikkei is down -1.40%. Hong Kong HSI is down -0.26%. China Shanghai SSE is down -0.10%. Singapore Strait Times is down -0.42%. Japan 10-year JGB yield is up 0.03 at 1.551.

Overnight, DOW rose 1.01%. S&P 500 rose 0.32%. NASDAQ rose 0.14%. 10-year yield fell -0.055 to 4.238.

Australia jobs rebound with 24.5k growth in July, unemployment ticks lower

Australia’s labor market showed renewed strength in July, with employment rising by 24.5k, just shy of expectations for a 25.3k gain and a marked improvement from June’s tepid 1k increase. The headline was boosted by a sharp 60.5k jump in full-time positions, which more than offset a -35.9k drop in part-time jobs.

The unemployment rate eased from 4.3% to 4.2%, in line with forecasts, while the participation rate held steady at 67.0%. Signs of underlying resilience were also reflected in a 0.3% mom increase in total hours worked.

The strong full-time hiring points to ongoing momentum in higher-quality job creation, which could temper any immediate RBA shift toward further easing as policymakers weigh domestic strength against global uncertainties.

Fed’s Goolsbee says fall FOMC meetings will be “live”

Chicago Fed President Austan Goolsbee said overnight that the next few months will bring “live” policy meetings, as the Fed faces one of the hardest tasks in central banking—getting the “timing” right during “moments of transition”.

Goolsbee expressed caution over assuming the inflationary impact of tariffs will fade quickly, preferring to wait for upcoming wholesale and consumer price data before deciding on the need for a rate cut.

On jobs, Goolsbee downplayed the signal from recent payroll slowing, suggesting it may reflect reduced immigration rather than a broad cooling. With unemployment at 4.2%, “I think the state of the labor market is pretty strong, pretty solid,” he said.

Fed’s Bostic urges patience, says tariffs may redefine inflation path

Atlanta Fed President Raphael Bostic signaled that the strength of the US labor market gives policymakers breathing room before deciding on rate moves. With unemployment near full employment, he said the Fed can avoid rushing into policy changes. “My predisposition is to try not to do that,” he said, emphasizing the need for more clarity before acting.

Bostic stressed that while inflation remains the primary mandate risk, the job market is in solid shape, and the coming weeks should be spent assessing its underlying health. That evaluation will be key in setting the tone for the Fed’s September meeting, he said.

Turning to tariffs, Bostic noted that Trump’s trade measures differ from past experiences in scope, scale, and intent. Rather than simply raising prices temporarily, he said they could fundamentally alter global supply chains, meaning post-tariff inflation could follow an entirely different trajectory. “It is actually a different economy,” he added.

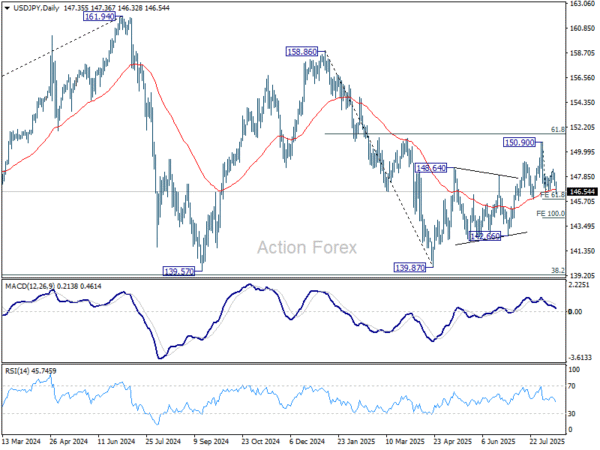

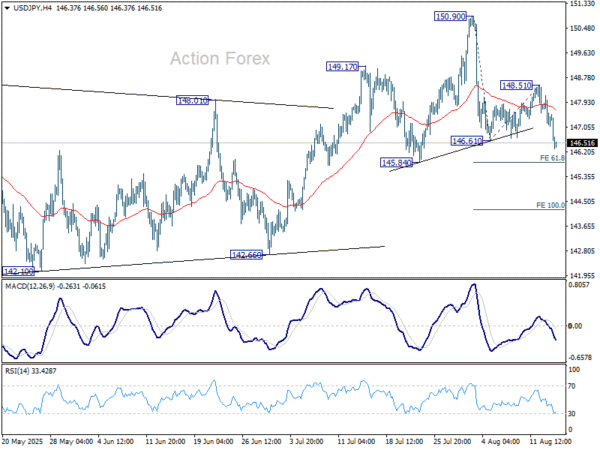

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.92; (P) 147.55; (R1) 148.00; More…

USD/JPY’s fall from 150.90 resumed by breaking 146.61 support, and head and should top pattern is in place (ls: 149.17, h: 150.90, rs: 148.15). Intraday bias is back on the downside for 145.84 support next. Decisive break there will suggest that whole rebound from 139.87 has completed at 150.90, and turn outlook bearish. Next target is 100% projection of 150.90 to 146.41 from 148.51 at 144.22. On the downside, above 148.51 will bring retest of 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.