Asian markets opened the week on a positive note, with Japan’s Nikkei 225 extending its rally to fresh record highs. The interplay between Nikkei and Yen remains crucial. A softer yen improves exporters’ competitiveness, lifting equities. At the same time, robust equity performance can in turn weigh on the currency as investors channel funds into riskier assets. The feedback loop is evident again today, with Yen sliding broadly.

In the currency markets, Yen leads losses, followed by Dollar and Euro. On the flip side, Kiwi, Aussie and Loonie are outperforming, reflecting demand for higher-beta plays in a risk-on environment. Sterling and Swiss Franc sit in the middle of the pack.

With the economic calendar light today, some attention is turning to geopolitics. US President Donald Trump’s meeting with Ukrainian President Volodymyr Zelenskiy and European leaders will be closely followed. The talks come after Trump’s summit with Russian President Vladimir Putin last Friday, which Trump called “productive” despite yielding no breakthrough.

Before European leaders join the broader conversation, Trump and Zelenskiy are due to meet one-on-one. European capitals are keen to help Zelenskiy avoid another public confrontation like the one in February, when Trump and Vice President JD Vance criticized him in the Oval Office.

To bolster Zelenskiy’s position, German Chancellor Friedrich Merz, French President Emmanuel Macron, and UK Prime Minister Keir Starmer convened allies on Sunday. Their aim is to secure stronger security guarantees for Ukraine, ideally with the US playing a central role.

Beyond geopolitics, the macro calendar is heavy later this week. Markets will parse Canada CPI on Tuesday, RBNZ, UK CPI, and FOMC minutes on Wednesday, global PMIs on Thursday, and Japan CPI on Friday. All of this culminates with the Jackson Hole Symposium from Thursday to Saturday, where Fed officials’ comments will set the tone for September policy expectations.

In Asia, at the time of writing, Nikkei is up 0.87%. Hong Kong HSI is up 0.67%. China Shanghai SSE is up 1.24%. Singapore Strait Times is down -0.84%. Japan 10-year JGB yield is up 0.013 at 1.579.

NZ BNZ services uptick to 48.9, contraction persists

New Zealand’s BusinessNZ Performance of Services Index improved slightly in July, rising from 47.6 to 48.9. But the sector remained in contraction for the sixth consecutive month. Also, the latest reading is still well below the long-run survey average of 52.9.

Details showed mixed conditions. Activity/Sales stayed in contraction at 47.5, and New Orders stalled at 50.0. On the positive side, Inventories expanded for the second month at 51.4. Employment component slid to 47.1, extending its losing streak to 20 months.

Business sentiment, while slightly less negative, continued to reflect difficult conditions. Around 58.5% of comments were pessimistic, down from 66.2% in June. Firms pointed to declining sales, reduced spending, and persistent cost-of-living pressures. Inflation, high interest rates, weather disruptions, staffing shortages, and global uncertainty all weighed on confidence.

Key 112K level in focus as Bitcoin reverses from record

Bitcoin’s near-term outlook now hinges on whether 112,000 zone can hold as support after last week’s brief breakout to a record 124,553. The sharp reversal has shifted attention to this key level, with selling pressure still visible as the new week begins.

The current decline was triggered by U.S. Treasury Secretary Scott Bessent, who unsettled markets by revealing government Bitcoin reserves were worth only USD 15–20 billion, far below estimates. He added that Washington would not buy new Bitcoin for its strategic reserve, instead relying on confiscated assets to build holdings.

While he later clarified on X that Treasury remained open to “budget-neutral pathways” to expand reserves, confidence took a hit. Investors interpreted the comments as a sign Washington is unlikely to bolster demand in the near term.

Combined with stretched technicals, the backdrop encouraged traders to lock in profits, ending Bitcoin’s latest rally attempt prematurely.

Technically, momentum is fading. Bearish divergences in both the daily and 4-hour MACD highlight loss of upside strength. While another test of the highs cannot be ruled out, gains above 124,553 appear constrained.

Instead, focus has shifted to the 111,889 structural support. Decisive break there would confirm correction of the rally from 74,373, opening the door for a pullback to 38.2% retracement of 74,373 to 124,553 at 105,384.

That could set the stage for either prolonged consolidation or a deeper pullback before any fresh bullish leg.

Jackson Hole to test Fed’s September cut resolve; RBNZ cut as last?

The coming week is dominated by the Jackson Hole Economic Policy Symposium on August 21–23, which traditionally serves as the Fed’s most important policy forum outside of formal FOMC meetings. This year, markets are focused less on abstract long-term themes and more on whether Fed officials drop any clues about the likelihood of a rate cut at the September 16-17 meeting.

For now, the Fed still has two critical data points in hand before that decision — August CPI and the next Nonfarm Payrolls report. That gives officials room to remain cautious. Some may argue it is too early to commit, but their tone at Jackson Hole will be parsed carefully for signs of whether the committee is leaning toward action if those reports come in broadly in line with expectations.

The balance of voices will matter. Doves like Christopher Waller and Michelle Bowman dissented at the July meeting in favor of an immediate cut, suggesting internal debate is more intense than usual. The minutes of that meeting, due earlier in the week, will shed light on the arguments for and against moving sooner. Traders will be keen to see whether more members are quietly sympathetic to the dovish camp.

Chair Jerome Powell’s Friday speech is the highlight of Jackson Hole. But investors have learned not to expect Powell to deviate much from his hallmark cautious, even-handed style. He sees himself more as a moderator of the FOMC rather than its chief ideological driver, and is unlikely to give away a firm commitment. Still, even subtle phrasing shifts could tilt expectations on whether the Fed is preparing to cut as soon as September.

Beyond the Fed, markets also turn to New Zealand, where the RBNZ rate decision will be closely watched. A Reuters poll showed 28 of 30 economists expect a 25bps cut to 3.00%, with only two calling for a hold. Inflation has slowed to 2.7% in Q2, inside the bank’s 1–3% target, while unemployment rose to 5.2%, the highest since 2020. These conditions give the RBNZ reason to ease policy further.

The debate is now about where the easing cycle ends. Of 29 economists forecasting year-end levels, half see rates steady at 3.00%, half at 2.75%, with one outlier expecting no further cuts. Local banks are also split: ASB and Westpac think the RBNZ pauses after this week, BNZ sees a path to 2.75%, while ANZ and Kiwibank expect easing down to 2.50% next year. Markets will weigh not just the cut, but also how Governor Christian Hawkesby frames the road ahead.

In the UK, attention will turn to CPI and retail sales after last week’s strong Q2 GDP print reinforced Sterling’s outperformance. With inflation still elevated, the BoE’s cautious approach to cutting rates is unlikely to change, and fresh data could give the Pound another leg higher if it confirms persistent price pressures.

Elsewhere, CPI from Japan, CPI and retail sales from Canada, and global PMI readings will round out the week’s calendar.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan tertiary industry index; Eurozone trade balance; Canada housing starts; US NAHB Housing.

- Tuesday: New Zealand PPI; Australia Westpac consumer sentiment; Canada CPI; US new residential construction.

- Wednesday: Japan trade balance, machine orders; China rate decision; RBNZ rate decision; Germanny PPI; UK CPI; Eurozone CPI final; US FOMC minutes.

- Thursday: New Zealand trade balance; Australia PMIs; Japan PMIs; Swiss Trade balance; Eurozone PMIs; UK PMIs; Canada IPPI and RMPI; US jobless claims, Philly Fed survey, PMIs, existing home sales.

- Friday: UK Gfk consumer sentiment; Japan CPI; Germany GDP final; UK retail sales; Canada retail sales.

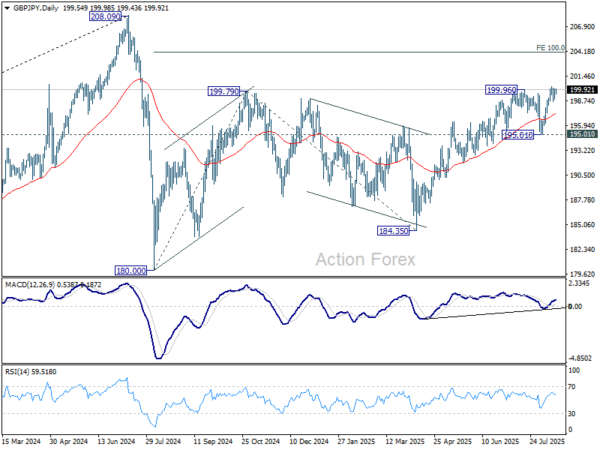

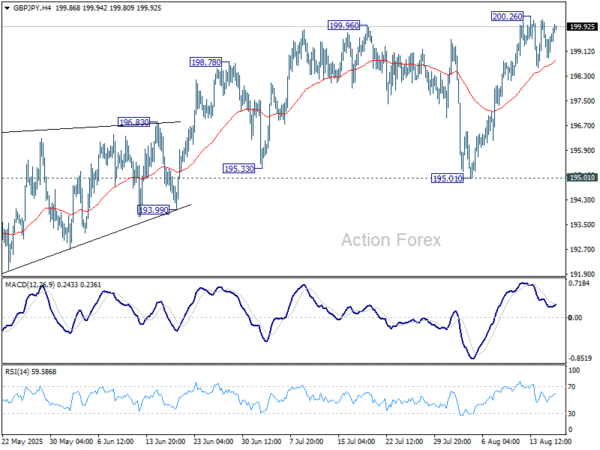

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.92; (P) 199.57; (R1) 200.23; More…

GBP/JPY recovers today but stays below 200.26 resistance and intraday bias remains neutral. Some more consolidations could be seen, but in case of another fall, downside should be contained well above 195.01 support. On the upside, firm break of 200.26 will resume the whole rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.