Asian trading was uneven today as strong Japanese GDP data contrasted sharply with a softer Chinese macro picture. Tokyo’s Nikkei 225 received a boost from the better-than-expected growth reading, while Yen advanced across the board. Signs of resilience in Japan’s economy despite tariff uncertainty have strengthened market confidence that the BoJ will hike again before year-end.

While September’s policy meeting is still widely seen as a hold, consensus is shifting toward October as a realistic window for the next move. A key focus for policymakers will be whether household consumption starts to recover in Q3, underpinned by improving real wage growth after months in negative territory. A stronger household sector could give policymakers more confidence to resume their gradual policy normalization path.

In contrast, sentiment toward Chinese assets deteriorated after a raft of July economic indicators fell short of expectations. The data pointed to weakening momentum across industrial output, retail sales, and investment, with the drag from the property slump intensifying. Overcapacity in new industries and the fading lift from consumer trade-in programs further cloud the near-term outlook.

This weaker backdrop also hit Aussie and Kiwi, both of which are sensitive to Chinese demand trends. While robust export figures have offered some support, the overall domestic slowdown in China could keep commodity currencies under pressure unless Beijing signals stronger stimulus. For now, policymakers appear inclined to monitor conditions through Q3 before considering fresh action in Q4.

Dollar, meanwhile, is consolidating its gains from Wednesday’s sharp PPI-driven rebound. The challenge for the Fed is that tariff effects on inflation will not dissipate quickly. As St. Louis Fed President Alberto Musalem cautioned, the upward impact on prices could persist for two to three quarters, keeping inflation readings elevated well into 2026.

Such persistence in price pressures would limit Fed’s scope for aggressive rate cuts in the near term, even if growth momentum softens. For Dollar, this dynamic could help slow its selling momentum despite concerns about institutional credibility and political risks.

For the week so far, Sterling remains the top performer, followed by Yen and Swiss Franc. Kiwi is at the bottom of the table, with Loonie and Aussie also lagging. Dollar and Euro are mid-pack. Despite extended rallies in US and Japanese equities, FX flows still reflect caution rather than a full embrace of risk.

In Asia, at the time of writing, Nikkei is up 1.65%. Hong Kong HSI is down -0.91%. China Shanghai SSE is up 0.86%. Singapore Strait Times is down -1.04%. Japan 10-year JGB yield is up 0.017 at 1.569. Overnight, DOW fell -0.02%. S&P 500 rose 0.03%. NASDAQ fell -0.01%. 10-year yield rose 0.055 to 4.293.

Japan’s GDP extends growth streak to fifth quarter on strong investment and exports

Japan’s economy expanded 0.3% qoq in Q2, topping expectations of 0.1% qoq. Q1 figures were also revised up to 0.1% qoq growth from a prior estimate of contraction. On an annualized basis, GDP rose 1.0% , marking a fifth consecutive quarter of expansion—a sign of steady, if moderate, momentum.

Capital investment increased 1.3% qoq, extending its growth streak to five quarters, reflecting resilient corporate spending. Exports also provided a boost with a 2.0% rise, outpacing the 0.6% gain in imports, which act as a drag on GDP. The combination of solid external demand and firm investment highlights a balanced growth profile.

Private consumption, which accounts for more than half of Japan’s economic activity, inched up 0.2% qoq. The soft household spending highlights the need for wage growth and consumer confidence to strengthen if Japan is to build on its investment-led momentum and secure a more balanced recovery.

China’s growth momentum fades as July data misses forecasts

China’s July economic activity slowed more than expected, with industrial production rising 5.7% yoy, short of the 6.0% yoy forecast and easing from June’s 6.8% yoy. Retail sales growth also disappointed, up 3.7% yoy versus the 4.6% yoy expected, marking a slowdown from 4.8% yoy in the prior month.

From January to July, fixed asset investment grew just 1.6% yoy, well below the 2.7% yoy forecast and down from 2.8% previously yoy, marking the weakest pace since September 2000. The persistent downturn in the property sector remains a major drag, with property investment contracting -12% yoy over the first seven months.

NZ BNZ PMI back in growth zone as new orders surge

New Zealand’s manufacturing sector returned to growth in July, with the BusinessNZ Performance of Manufacturing Index rising from 49.2 to 52.8, moving back above the historical average of 52.5.

All five sub-indices registered expansion, led by New Orders at 54.2—its highest since March 2022—and Production at 53.6, the strongest since August 2022. Finished Stocks and Deliveries of Raw Materials also posted modest growth, while Employment (50.1) edged back above the no-change level after two months of contraction.

Despite this encouraging turnaround, sentiment among manufacturers remains guarded. The share of negative comments fell to 58.6% from June’s 65.5%.

Respondents continued to highlight weak demand, rising costs, and ongoing economic uncertainty. Tariffs, subdued construction activity, and soft consumer spending were cited as key headwinds, with many firms noting delayed projects and a tendency for customers to place only essential orders.

Fed’s Musalem: 50bps cut unsupported by current conditions

St. Louis Fed President Alberto Musalem said on CNBC that his outlook has shifted in recent months, with inflation risks revised “slightly lower” and potential labor market weakness assessed “slightly higher”.

Musalem stressed that his views remain fluid and will continue to evolve ahead of the September FOMC meeting. He avoided committing to a September rate cut but was clear that a 50bps move is “unsupported” by current conditions.

On tariffs, Musalem said any inflationary impact is likely to fade within two or three quarters.

Separately, Richmond Fed President Thomas Barkin said the Fed is still weighing whether high unemployment or sustained inflation poses the greater risk to its dual mandate.

“High unemployment is, in fact, disinflationary. Or is inflation high enough or sustained enough that it’s going to put inflation expectations at risk? And I think that’s the trade-off you’re trying to manage,” Barkin said.

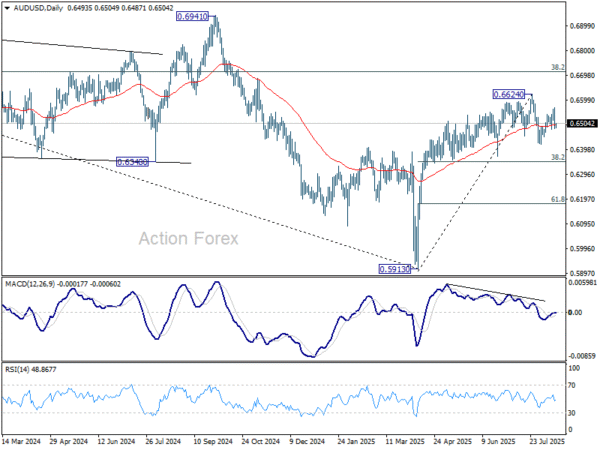

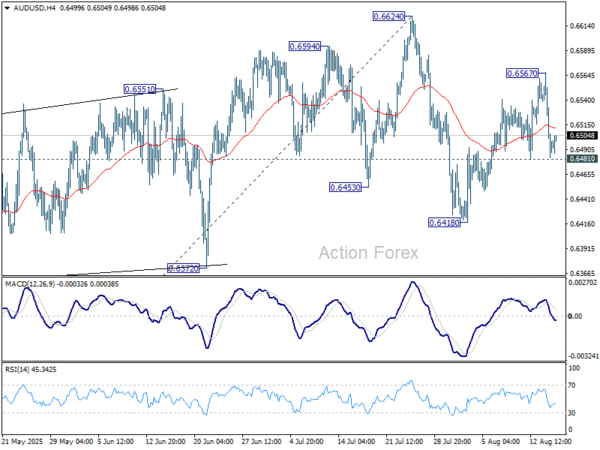

AUD/USD Daily Report

Daily Pivots: (S1) 0.6463; (P) 0.6516; (R1) 0.6549; More…

Intraday bias in AUD/USD is turned neutral first with the current steep retreat. On the downside, firm break of 0.6481 support will argue that corrective pattern from 0.6624 is extending with another falling leg. Intraday bias will be back on the downside for 0.6418 first. Break there will target 38.2% retracement of 0.5913 to 0.6624 at 0.6352. On the upside, above 0.6567 will extend the rebound from 0.6418 to retest 0.6624 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).