Dollar regained its footing in early US trade after much stronger-than-expected July PPI figures sharply reduced expectations for aggressive Fed easing. While a 25bps rate cut at the September FOMC meeting remains the market’s base case, the data has made a 50bps move far less likely.

Importantly, this PPI print captures only July’s data—before the August tariff escalation began impacting prices. That means upside risks to inflation could intensify over the coming months. Even if one takes the view that tariff-driven price gains are transitory, the duration of this “transition” is uncertain, making it difficult for policymakers to commit to deeper or faster cuts.

Labor market indicators offered little reason for the Fed to rush. Weekly jobless claims were steady. This stability highlights the Fed’s “luxury” of waiting for more data before making major moves, as Atlanta Fed’s Raphael Bostic noted earlier this week.

In currency markets, the Yen is holding as the day’s strongest performer. The -1.45% profit-taking pullback in the Nikkei triggered strong Yen buying, while a sharp drop in US equity futures after the PPI release further supported the safe-haven bid. Dollar ranks as the second strongest, followed by Sterling, which got an extra boost from much stronger-than-expected UK Q2 GDP data.

The UK growth figures, paired with this week’s labor data showing wage growth staying elevated despite some cooling, give the BoE little reason to deviate from its current pace of one rate cut per quarter. That policy stance, coupled with solid fundamentals, has kept Sterling well supported.

At the other end of the spectrum, risk-sensitive currencies are under pressure. Both Kiwi and Aussie are suffering from the risk sentiment turn, while Euro is among the day’s laggards, weighed down in part by a sharp selloff against Sterling. Swiss Franc and Loonie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is up 0.40%. CAC is up 0.38%. UK 10-year yield is up 0.019 at 4.614. Germany 10-year yield is up 0.012 at 2.695. Earlier in Asia, Nikkei fell -1.45%. Hong Kong HSI fell -0.37%. China Shanghai SSE fell -0.46%. Singapore Strait Times fell -0.38%. Japan 10-year JGB yield rose 0.031 to 1.552.

US PPI surges 0.9% mom in July, undermining case for aggressive Fed easing

US producer prices surged in July, with final demand PPI jumping 0.9% mom, far exceeding expectations of a 0.2% rise and marking the sharpest monthly gain since mid-2022.

The increase was broad-based, with over three-quarters driven by final demand services, which climbed 1.1% mom, while goods prices rose 0.7% mom. The core measure excluding food, energy, and trade services climbed 0.6% mom, the largest increase since March 2022.

On an annual basis, headline PPI accelerated from 2.4% to 3.3% yoy, well above the 2.5% yoy forecast and the highest since February. PPI excluding food, energy, and trade services rose to 2.8% yoy.

The data may temper market enthusiasm for an aggressive September Fed rate cut, despite political pressure and calls from Treasury Secretary Bessent for a 50 bps move.

US initial jobless claims fall to 224k vs exp 227k

US initial jobless claims fell -3k to 224k in the week ending August 9, slightly below expectation of 227k. Four-week moving average of initial claims rose 750 to 222k.

Continuing claims fell -15k to 1953k in the week ending August 2. Four-week moving average of continuing claims rose 500 to 1951k.

Fed’s Daly: No case for 50bps urgent cut, dismisses ‘catch-up’ argument

San Francisco Fed President Mary Daly pushed back against the idea of a 50bps rate cut at the September FOMC meeting, a move strongly advocated earlier this week by Treasury Secretary Scott Bessent. In a Wall Street Journal interview, Daly said such a large cut would send an “urgency signal” that doesn’t match her view of the economy’s strength.

“I’m worried it would send an urgency signal that I don’t feel about the strength of the labor market,” she noted.

Daly stressed there’s no need to “catch up,” pointing to a still-solid job market. That’s in contrast to Bessent’s view that if the Fed had seen recent job market data sooner, it could have cut in June and July and now “needs to catch up.”

Eurozone industrial production falls -1.3% mom in June, broad weakness across sectors

Eurozone industrial production fell sharply by -1.3% mom in June, missing expectations of a -0.8% mom drop. The breakdown showed a mixed picture, with energy output up 2.9% mom, but declines in other categories: intermediate goods -0.2% mom, capital goods -2.2% mom, durable consumer goods -0.6% mom, and a steep -4.7% mom fall in non-durable consumer goods.

Across the EU, output slipped -1.0% mom. The largest monthly declines came from Ireland (-11.3%), Portugal (-3.6%), and Lithuania (-2.8%). On the upside, Belgium (+5.1%), France (+3.8%), Sweden (+3.8%), and Greece (+3.3%) posted notable gains

UK GDP beats forecasts with 0.3% growth in Q2, as June data delivers strong finish

UK GDP expanded 0.3% qoq in Q2, beating expectations of a 0.1% gain, though slowing sharply from Q1’s robust 0.7% pace. In output terms, growth was supported by a 0.4% qoq rise in services and a solid 1.2% qoq gain in construction, while the production sector contracted by -0.3% qoq. Real GDP per head grew 0.2% qoq over the quarter, underlining modest but broad-based expansion despite headwinds.

Some of the Q2 slowdown was likely due to front-loading in Q1, with activity pulled forward into February and March ahead of April’s stamp duty changes and US tariffs.

June posted a strong 0.4% mom rebound—double consensus, back-to-back declines in April and May. Within the monthly data, services output climbed 0.3% mom, production rose 0.7% mom, and construction gained 0.3% mom.

Australia jobs rebound with 24.5k growth in July, unemployment ticks lower

Australia’s labor market showed renewed strength in July, with employment rising by 24.5k, just shy of expectations for a 25.3k gain and a marked improvement from June’s tepid 1k increase. The headline was boosted by a sharp 60.5k jump in full-time positions, which more than offset a -35.9k drop in part-time jobs.

The unemployment rate eased from 4.3% to 4.2%, in line with forecasts, while the participation rate held steady at 67.0%. Signs of underlying resilience were also reflected in a 0.3% mom increase in total hours worked.

The strong full-time hiring points to ongoing momentum in higher-quality job creation, which could temper any immediate RBA shift toward further easing as policymakers weigh domestic strength against global uncertainties.

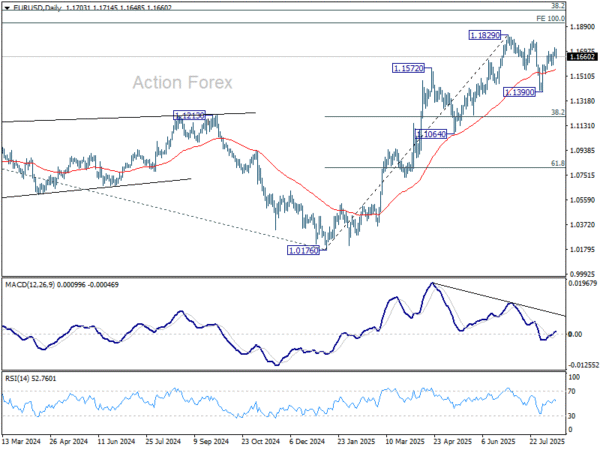

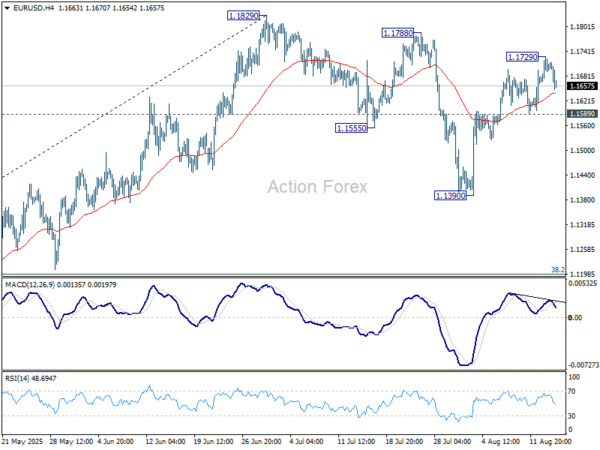

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1673; (P) 1.1701; (R1) 1.1734; More…

Intraday bias in EUR/USD is turned neutral again with current retreat. Some consolidations would be seen below 1.1729. Further rise is expected as long as 1.1589 support holds. Above 1.1729 will target a retest on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, however, break of 1.1589 support will delay the bullish case and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.