Dollar swung sharply overnight as speculation swirled around the fate of Fed Chair Jerome Powell. Reports surfaced that US President Donald Trump was preparing to fire Powell imminently, with one claim suggesting a dismissal letter had already been drafted and shown to lawmakers during a meeting on cryptocurrency legislation. Dollar initially plunged on the news amid fears of a major hit to Fed credibility.

However, the greenback recovered swiftly after Trump walked back the rumors, telling reporters, “We’re not planning on doing it… I don’t rule out anything, but I think it’s highly unlikely, unless he has to leave for fraud.” Still, the episode reinforced growing concerns about political interference at the central bank. Persistent pressure from the White House to lower interest rates has already raised questions about Fed independence.

For now, most Fed officials appear focused on managing inflation risks tied to the Trump administration’s sweeping tariffs. While Powell chairs the FOMC, policy decisions remain collective, limiting the scope for direct political influence. But markets remain wary. Any leadership upheaval interpreted as compromising the Fed’s autonomy could trigger a sharp repricing in the dollar, equities, and—most critically—Treasuries.

A selloff in US government bonds would hit the administration hardest, pushing yields sharply higher and raising borrowing costs at a time of ballooning deficits. That prospect may help explain Trump’s decision to distance himself, for now, from the firing chatter.

Elsewhere, Australian Dollar slumped in Asia after June employment data badly missed expectations, with particular weakness in full time work. Some market participants criticized RBA’s July hold as a policy misstep in hindsight. Others caution against overreacting, noting the data may reflect volatility rather than a turning point. Still, the market now sees rising odds of an August cut, contingent on the upcoming Q2 inflation print. If CPI also softens, the case for easing will be hard to dismiss.

In the broader FX space, Dollar remains the week’s best performer, followed by Loonie and then Euro. Kiwi and Aussie are the worst, while Swiss Franc also lagged. Yen and Sterling are treading water in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 0.36%. Hong Kong HSI is up 0.07%. China Shanghai SSE is up 0.23%. Singapore Strait Times is up 0.51%. Japan 10-year JGB yield is down -0.016 at 1.561. Overnight, DOW rose 0.53%. S&P 500 rose 0.32%. NASDAQ rose 0.25%. 10-year yield fell -0.034 to 4.455.

Fed Beige Book: Inflation to rise more rapidly by late summer

The Fed’s latest Beige Book reported a slight pickup in US economic activity from late May through early July, a modest improvement over the previous edition. Five districts saw slight or modest growth, while five were flat and two reported declines.

However, businesses remain wary, with uncertainty still elevated and the overall outlook described as “neutral to slightly pessimistic.” Only two districts expected any pickup in activity moving forward. Labor conditions remained cautious, with only a very slight increase in employment and modest wage growth.

Price pressures continued to build, described as moderate to modest across districts. Input costs tied to tariffs—particularly in manufacturing and construction—were widely cited, with most businesses facing “modest to pronounced” cost pressures.

A growing number of firms are beginning to pass these higher costs to consumers via price hikes or surcharges. Others, constrained by customer price sensitivity, have opted to absorb the increases, compressing margins. With broad expectations for continued cost pressure in the coming months, the Fed noted that “consumer prices will start to rise more rapidly by late summer”.

Fed’s Williams: Inflation to hit 3–3.5% as tariffs bite

New York Fed President John Williams warned that tariff effects are only beginning to show up in the data and could push inflation significantly higher in the months ahead. Speaking overnight, Williams said the full impact of US tariffs will take time to materialize, but expects them to add “about 1 percentage point” to inflation through the second half of this year and into early 2026. While he acknowledged current data shows only “modest” impact, he anticipates upward pressure will grow meaningfully.

Williams forecast inflation to average between 3% and 3.5% in 2025, before cooling to around 2.5% in 2026 and only returning to the Fed’s 2% target by 2027. For June specifically, he expects headline inflation at 2.5% and core at 2.75%. Alongside elevated price pressures, he also projects a slowing economy, with growth easing to around 1% this year and unemployment rising to 4.5% from the current 4.1%.

Against this backdrop, Williams endorsed holding rates at current levels. “Maintaining this modestly restrictive stance of monetary policy is entirely appropriate,” he said, suggesting the Fed is in no rush to cut despite cooling growth.

Fed’s Bostic: Price pressures are real

Atlanta Fed President Raphael Bostic warned that rising inflation linked to import tariffs may delay any rate cuts. Speaking to Fox Business, Bostic acknowledged the uncertainty created by Trump’s trade actions. He added that increasing price pressures is now visible across the Southeast. “The price pressures are real,” he said, citing business feedback and internal surveys.

Bostic suggested the June CPI report, which showed broad-based increases in prices—particularly for heavily imported goods—may mark an “inflection point”. He highlighted that headline inflation moved further away from the Fed’s 2% target. “We’ve seen the highest increase in prices that we’ve seen all year,” he added. That backdrop, he argued, warrants caution.

When pressed about the possibility of no rate cut until 2026, Bostic didn’t rule it out. “Everything is on the table,” he said, stressing that the path of policy will depend entirely on how inflation evolves. “If prices continue to move steadily away from our target, then we’ll have to consider what policy response is appropriate.”

UK payrolled employment slips again, wage growth slows further

UK payrolled employment fell by -41k in June, marking a second straight monthly contraction. Though May’s drop was revised to a milder -24k from an initial -109k, the overall picture still points to a softening labor market. Claimant count rose more than expected by 25.8k. Unemployment rate in the three months to May edged higher from 4.6% to 4.7%.

Wage growth also lost some momentum, with median monthly pay rising 5.6% yoy in June, down from May’s 5.7% yoy. Average earnings growth in the three months to May slowed to 5.0% both with and without bonuses, with the latter still slightly hotter than the 4.9% expected.

Aussie unemployment rate surges to 4.3% as full-time jobs slide

Australia’s June jobs report came in well short of expectations, with only a 2k increase in employment and a sharp divergence between full-time and part-time work. Full-time employment plunged by -38.2k while part-time roles rose 40.2k. Unemployment rate rose to 4.3%, defying forecasts for it to hold at 4.1%, while participation rate remained unchanged at 67.0%.

According to the ABS, the rise in joblessness was driven by a 34k increase in the number of unemployed Australians. ABS labor head Sean Crick added that full-time hours worked declined -1.3% in the month, suggesting further weakness ahead. Despite a marginal rise in total hours worked of 0.1% mom, the data add to signs that the labor market is losing momentum.

Japan auto exports to US plunge -26.7% yoy as carmakers cut prices

Japan logged a trade surplus of JPY 153B in June, with exports down -0.5% yoy and imports up 0.2% yoy. The most striking detail was a sharp -11.4% yoy drop in exports to the US, the steepest decline since February 2021. Imports from the US also fell, declining -2.0% yoy.

Automobile shipments to the US fell -26.7% by value, while auto parts (-15.5% yoy) and pharmaceuticals (-40.9% yoy) also saw double-digit drops. Still, a 3.4% yoy rise in car export volumes suggests Japanese automakers are slashing prices and absorbing costs to maintain market share.

On a seasonally adjusted basis, exports dipped -0.4% mom while imports fell -1.0%, leaving a JPY 235B trade deficit.

The report comes just weeks before a 25% reciprocal US tariff on Japanese goods takes effect on August 1. That is one percentage point higher than the 24% rate first announced on “Liberation Day” in April.

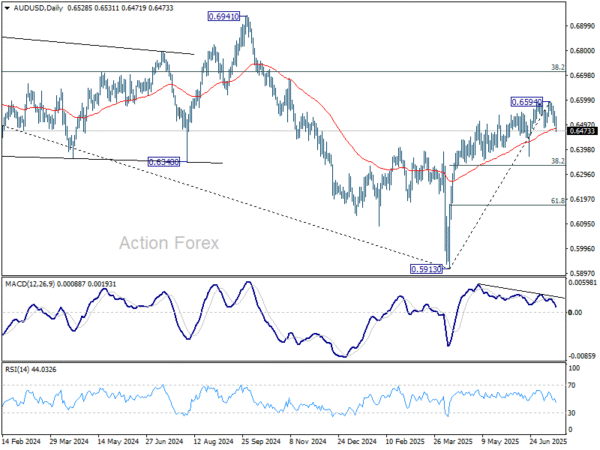

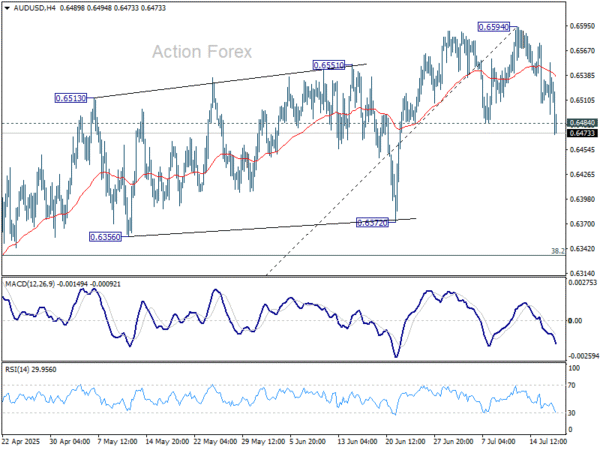

AUD/USD Daily Report

Daily Pivots: (S1) 0.6498; (P) 0.6526; (R1) 0.6557; More…

AUD/USD’s break of 0.6484 support confirms short term topping at 0.6594. Fall from there is tentatively seen as a correction to rise from 0.5913. Intraday bias is back on the downside for 38.2% retracement of 0.5913 to 0.6594 at 0.6334. Strong support could be seen there to bring rebound. But for now, near term outlook is neutral as long as 0.6594 resistance holds, and more consolidations would be seen. Meanwhile, sustained trading below 0.6334 will raise the chance of bearish reversal.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).