Asian equities traded lower today, tracking the decline on Wall Street overnight, as investors grappled with rising bond yields and renewed trade uncertainty. Even stronger-than-expected Chinese services PMI and robust Australian GDP data failed to lift sentiment, with risk aversion setting the tone across the region. Additionally, markets remain cautious ahead of Friday’s closely watched U.S. nonfarm payrolls report, which will provide critical guidance for the Fed’s September decision. For now, positioning is defensive, with equities in the regional under some pressure.

At the heart of the market stress is a new wave of sovereign risk emanating from Europe. The UK’s fiscal outlook is under sharp scrutiny, pushing gilt yields to 27-year highs, while French bonds are suffering amid political instability and the risk of a government collapse in a confidence vote next week. Both countries embody the vulnerabilities of fiscal fragility and waning investor confidence.

The U.S. is also facing its own risks. A federal appeals court ruled last Friday that most of President Donald Trump’s sweeping global tariffs were illegal. The tariffs, estimated to generate USD 172.1 billion in 2025, face the possibility of some refunds if the ruling is upheld. That would likely force a surge in Treasury issuance to cover the shortfall, putting further pressure on bond markets. U.S. yields are already at elevated levels. The 30-year Treasury yield is trading near 4.985%, with economists warning that a break above 5% would be a troubling signal for the U.S. government and global markets.

In FX, Yen is currently the weakest performer this week so far, weighed down by rising global yields and persistent trade uncertainties. Sterling is the second-worst after sharp losses and an inability to recover with momentum, while Kiwi is also under soft. Dollar is the standout gainer, benefiting from higher U.S. yields and safe-haven demand. Loonie and Aussie follow, while Euro and Swiss Franc are trading mid-pack.

In Asia, at the time of writing, Nikkei is down -0.93%. Hong Kong HSI is down -0.48%. China Shanghai SSE is down -0.87%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.029 at 1.636. Overnight, DOW fell -0.55%. S&P 500 fell -0.69%. NASDAQ fell -0.82%. 10-year yield rose 0.050 to 4.277.

Australia’s GDP rebounds 0.6% qoq in Q2, as spending and exports drive recovery

Australia’s economy grew 0.6% qoq in Q2, beating expectations of 0.5% qoq and expanding 1.8% yoy from a year earlier. The Australian Bureau of Statistics noted that growth rebounded after weather disruptions depressed activity in Q1. GDP per capita also rose 0.2% qoq, reversing the decline recorded in the March quarter.

Domestic final demand was the key driver, supported by a 0.9% qoq rise in household spending and a 1.0% qoq increase in government consumption. Public investment detracted from growth, but private demand proved resilient.

Net trade added 0.1 percentage points to GDP, driven by a rebound in exports of iron ore and LNG as production normalized after severe weather disruptions earlier in the year.

AUD/JPY eyes break A above 97.41 as Aussie strength, Yen weakness align

AUD/JPY extended its rally this week, surging toward the 97.41 resistance level and positioning to resume the broader uptrend from the April low of 86.03. The move has been driven by a powerful combination of Australian Dollar strength and Yen weakness, pushing the cross closer to levels not seen since earlier this year.

For Aussie, Q2 GDP surprised to the upside at 1.8% yoy, its strongest expansion since 2023 and above RBA own forecast of 1.6%. Household consumption and government spending were key contributors, while net trade added to growth thanks to stronger iron ore and LNG exports. The data reinforced a picture of an economy proving more resilient than feared. Meanwhile, inflationary pressures remain sticky. Released last week, July CPI accelerated to 2.8% year-on-year, a reminder that consumer demand is still strong and disinflation is not guaranteed.

Recent data reinforces that the RBA is firmly on hold this month, with November shaping up as the earliest window for another rate cut. Even then, any rate cuts are likely to remain gradual given the still-firm growth and inflation backdrop.

On the Yen side, stalled trade negotiation process is adding strain. Hopes for a U.S. executive order to reduce auto tariffs remain unfulfilled, and Deputy Governor Ryozo Himino’s warning about downside risks to growth underscores the BoJ’s reluctance to tighten further in the near term. Yen’s position has also been eroded by this week’s surge in global bond yields, led by gilts.

Technically, today’s break above 96.81 resistance suggests that AUD/JPY’s correction from 97.41 completed as a five-wave triangle at 94.38. As long as 96.04 minor support holds, the bias remains firmly upward. Decisive break of 97.41 would resume the rise from 86.03, targeting the 38.2% projection of 86.03 to 97.41 from 94.38 at 98.72. Further break there break there could prompt upside acceleration to 61.8% projection at 101.41.

Looking medium term, the broader corrective downtrend from 2024 high at 109.36 should have completed with three waves down to 86.03. If that scenario holds, clearing structural resistance at 102.39 could open the way for a full retest of 109.36.

BoJ’s Ueda meets PM Ishiba, stresses stable FX and policy vigilance

BoJ Governor Kazuo Ueda said he discussed economic and market conditions, including foreign exchange moves, in a meeting with Prime Minister Shigeru Ishiba today. Ueda told reporters afterward that “it’s desirable for currency rates to move stably, reflecting fundamentals,” but declined to elaborate further on the details of the exchange.

On policy, Ueda reaffirmed that the BOJ remains prepared to raise interest rates further if the economy and prices evolve in line with projections. He emphasized that the central bank will “scrutinize without any pre-conception” whether those projections materialize.

China RatingDog services PMI rises to 53.0, optimism improves

China’s services sector gained fresh momentum in August, with the RatingDog PMI rising to 53.0 from 52.6, topping expectations of 52.5 and marking the highest level since May 2024. The composite index also improved, climbing to 51.9 from 50.8.

RatingDog founder Yao Yu highlighted that new business inflows surged to the highest since May of last year, while new export orders expanded at the fastest pace since February. More stable domestic demand and a recovery in foreign demand were key drivers, with service providers also reporting stronger optimism—the highest since March.

Price trends, however, remained challenging. Input costs rose modestly but firms were unable to fully pass them on, with output prices slipping back into contraction. That indicates profit margins have been under sustained pressure since late 2023.

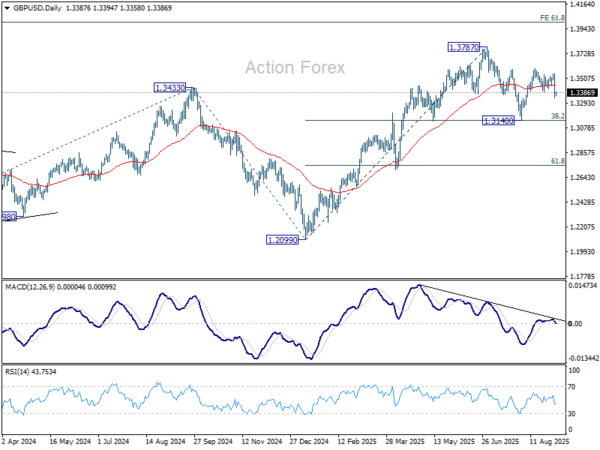

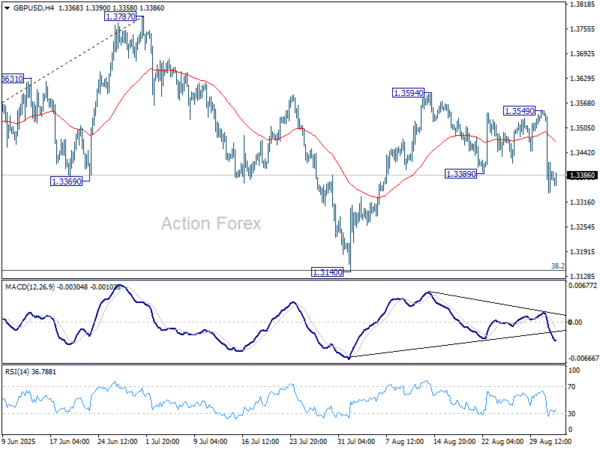

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3306; (P) 1.3428; (R1) 1.3515; More…

Intraday bias in GBP/USD remains on the downside for the moment. Corrective pattern from 1.3787 is extending with another falling leg. Deeper decline would be seen back to 1.3140 support. But downside should be contained by 38.2% retracement of 1.2099 to 1.3787 at 1.3142. But still, for now, risk will stay mildly on the downside as long as 1.3459 resistance holds, in case of recovery.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3104) holds, even in case of deep pullback.