After a week of volatility, the forex markets settled into a quieter rhythm during the Asian session on Friday. Swiss Franc stabilized somewhat, but remains the weakest performer this week after a heavy blow from Washington.

Switzerland’s diplomatic efforts fell short as the harsh 39% US tariff on Swiss imports officially kicked in. The import levy is among the highest imposed under Trump’s “reciprocal tariff” regime. Swiss President Karin Keller-Sutter lamented the impact on industry, calling it “an extraordinarily difficult situation.” Despite intense eleventh-hour negotiations, no compromise was reached, and Swiss officials now say a resolution will take more time.

Nevertheless, talks continue behind closed doors, with Swiss officials offering new concessions in hopes of tariff relief. “Talks are already underway based on the new offer,” Keller-Sutter said, adding that while the US is a key partner, “not at any price.” It’s also estimated that the new tariffs could wipe out US market access for many Swiss manufacturers, trimming GDP by 0.3% to 0.6% over the next year.

On a more positive note, Japan appears to have secured corrective action from the US after a dispute over double tariffs. Tokyo’s lead negotiator Ryosei Akazawa said U.S. officials admitted to “a regrettable error” and would amend the presidential order. Duties already collected on Japanese goods since August 7 will be refunded, and the auto tariff will be formally lowered to 15%—as originally agreed in last month’s deal.

As the week nears its end, Sterling is still leading the pack, supported by BoE’s hawkish rate cut yesterday. With BoE Chief Economist Huw Pill scheduled to speak later today, markets may get a clearer sense of internal debate within the MPC—and whether a follow-up cut later this year is truly on the table.

Aussie and Kiwi follow behind in strength, while Swiss Franc is the weakest, trailed by Dollar and Yen. Euro and Loonie sit in the middle of the pack as markets await the next catalyst.

BoJ Opinions: 2–3 months needed to Gauge Tariff impacts, year-end hike possible

BoJ’s July 30–31 Summary of Opinions revealed a broadly cautious stance on future policy moves, with members emphasizing the need for more data before shifting course.

Despite the recent US–Japan tariff agreement, board members reaffirmed that Japan’s baseline outlook has not improved. “Japan’s economic growth will moderate and the improvement in underlying CPI inflation will be sluggish temporarily,” one policymaker said. Accordingly, the consensus was to maintain current interest rates and financial accommodation, while monitoring trade risks and external demand.

“At least two to three more months are needed to assess the impact of US tariff policy,” one member stated, noting that the direction of US monetary policy and exchange rates could also shift materially depending on inflation and labor conditions.

Still, the door is now open for rate hikes later this year. The Summary suggests that if incoming data shows resilience in the US economy—and Japan avoids major trade fallout—the BoJ could resume policy normalization as soon as year-end.

“It may be possible for the Bank to exit from its current wait-and-see stance, perhaps as early as the end of this year,” one policymaker said. That prospect keeps the door open to further hikes in late 2025 if inflation and growth align.

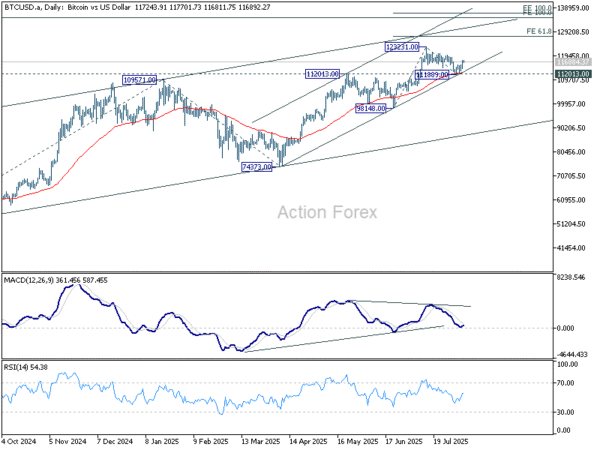

Bitcoin and Ethereum rally as Trump order unlocks 401(k) access to crypto

Crypto markets firmed after US President Donald Trump signed an executive order aimed at broadening investment options in retirement accounts. The policy change clears a path for cryptocurrencies, private equity, and real estate to be included in 401(k) plans, potentially diverting large-scale institutional capital into the digital asset space.

The USD 12 trillion defined contribution market has largely avoided exposure to alternative assets. Trump’s order seeks to reverse that by reducing litigation exposure and regulatory complexity for fund managers. “My Administration will relieve the regulatory burdens and litigation risk that impede American workers’ retirement accounts from achieving competitive returns,” Trump stated. Industry participants see this as a long-awaited greenlight to diversify away from traditional stocks and bonds.

Bitcoin bounces this week but stays well below 123,231 resistance. Near term consolidations could extend. But outlook remains bearish so far with a confluence of support intact, including 112,013 resistance turned support, 55 D EMA, and near term rising channel. Current up trend is expected to resume to 61.8% projection of 98,148 to 123,231 from 111,889 at 127,390 next.

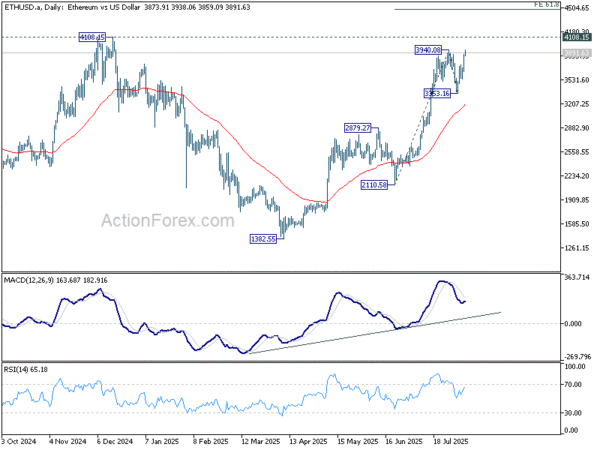

Ethereum’s breach of 3,940.08 resistance suggests that recent rally from 1,382.55 is resuming. Next target is 4,108.15 key resistance. Firm break there will target 61.8% projection of 2,110.58 to 3,940.08 from 3,353.16 at 4,483.19 next. In case of retreat, outlook will stay bullish as long as 3,353.16 support holds.

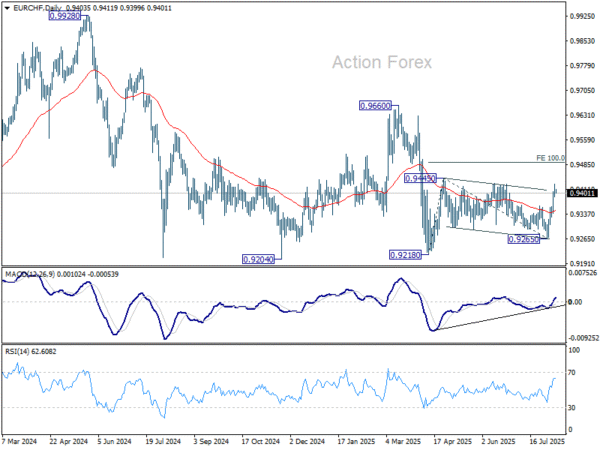

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9352; (P) 0.9380; (R1) 0.9430; More….

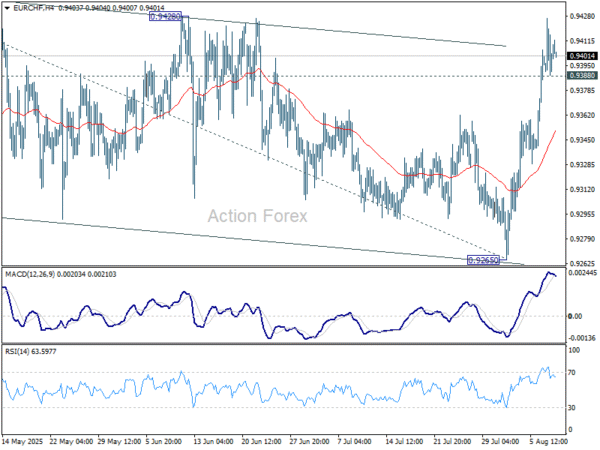

Intraday bias in EUR/CHF remains on the upside with focus on 0.9428 resistance Decisive break there should confirm that corrective pattern from 0.9445 has completed. Rise from 0.9128 should then be ready to resume to 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. On the downside, below 0.9388 minor support will delay the bullish case turn intraday bias neutral again first.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside position should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.