Global risk appetite extended higher, with S&P 500 and NASDAQ both setting new record highs overnight. DOW also surged over 500 pts, driven by optimism following the US-Japan trade deal. In Asia, Japan’s Nikkei continued its charge, with current momentum suggesting a record high could be imminent. The breakthrough between Washington and Tokyo boosted hopes for similar progress in other key trade relationships. The worst-case tariff scenarios seem to be receding quickly, even though uncertainty still lingers.

In the currency markets, Yen has outperformed this week so far, with Aussie not far behind. Australian Dollar was supported by both risk-on flows and cautious remarks from RBA Governor Bullock, who refrained from confirming an August cut. Kiwi is also firm, while Dollar is the week’s laggard, followed by Loonie and Swiss Franc. Euro and Sterling sit mid-pack.

The ECB takes center stage today, though few surprises are expected. Deposit are expected to remain unchanged at 2.00%, and President Christine Lagarde will probably avoid strong forward guidance given global uncertainties. September, with its updated projections and clearer trade outlook, is likely to bring a more decisive signal from the central bank. For now, today’s decision is seen largely as a placeholder.

Meanwhile, US President Donald Trump is set to visit the Fed, marking the first time in nearly two decades that a president makes an official appearance at the central bank. The symbolic move raises concerns about Fed independence, especially amid Trump’s repeated criticisms of Chair Jerome Powell. While speculation over Powell’s removal has circulated, Treasury Secretary Bessent said a successor will only be nominated near year-end, helping to dampen immediate fears.

On the trade front, in South Korea, hopes for a last-minute trade agreement were dealt a blow as the key 2+2 meeting with US officials was postponed. With tariffs looming from August 1, Seoul’s window to reach a deal is closing fast. The best outcome now may be an extension of negotiations.

Meanwhile, in Beijing, EU leaders met with Chinese President Xi Jinping to mark 50 years of relations. But with tensions over trade and the Ukraine war, expectations were low. European Commission President Ursula von der Leyen stressed rebalancing in trade, while Chinese President Xi Jinping urged “strategic choices” and deeper cooperation. The summit was cut to one day amid rising geopolitical and economic frictions, highlight the fragile state of EU-China relations.

In Asia, at the time of writing, Nikkei is up 1.81%. Hong Kong HSI is up 0.37%. China Shanghai SSE is up 0.48%. Singapore Strait Times is up 0.75%. Japan 10-year JGB yield is up 0.004 at 1.601. Overnight, DOW rose 1.14%. S&P 500 rose 0.78%. NASDAQ rose 0.61%. 10-year yield rose 0.052 to 4.388.

German GfK consumer sentiment dips to -21.5 as saving preference rises

German consumer confidence took another step back heading into August, with GfK Consumer Climate index falling to -21.5, down from -20.3 and missing expectations of -19.

The decline highlights persistent caution among households, delaying any meaningful rebound in consumer spending. According to Rolf Bürkl at NIM, the rise in saving appetite reflects a broader reluctance to commit to major purchases amid lingering uncertainty and elevated prices.

A durable improvement in sentiment, he emphasized, will require clearer signs of stability to reduce uncertainty and unlock household demand.

Japan’s PMI composite unchanged at 51.5, inflation to ease over the summer

Japan’s Composite PMI was unchanged at 51.5 in July. Services drove growth, rising from 51.7 to 53.5, while Manufacturing slipped into contraction at 48.8, down from 50.1.

S&P Global noted that manufacturers saw weaker output and new orders, weighed down by tariff uncertainty and cautious customer behavior. Confidence weakened across the board, with optimism falling to the second-lowest level since August 2020. Firms responded by slowing hiring to the weakest pace in 18 months.

On the positive side, cost pressures eased, with input inflation at a four-year low—suggesting headline “inflation may ease further over the summer”.

RBA’s Bullock flags slower disinflation, sticks with gradual easing bias

RBA Governor Michele Bullock signaled in a speech caution over the inflation outlook, warning that the fall in trimmed mean inflation in Q2 “may not be quite as much as we forecast”. While headline CPI is expected to dip into the lower half of the 2–3% target range, Bullock stressed that temporary cost-of-living relief is playing a role, and underlying pressures may prove more persistent. The RBA still anticipates inflation drifting toward 2.5%, but Bullock emphasized “we are looking for data to support this expectation”.

On the labor market, Bullock dismissed surprise around the recent rise in unemployment to 4.3%, saying the outcome was in line with RBA’s May forecasts. Although the June monthly figure saw a noticeable uptick, vacancy rates remain stable and leading indicators “are not pointing to further significant increases in the unemployment rate in the near term.”

Overall, she reaffirmed that a “measured and gradual” policy approach remains appropriate, especially with global risks—such as the trade war—showing signs of easing. Her remarks suggest the RBA remains on track for further easing, but will move cautiously, with the pace largely dictated by data flow—particularly the upcoming Q2 CPI print.

Australia PMI composite surges to 53.6, but inflation concerns linger

Australia’s private sector expanded more strongly in July, with the S&P Global Composite PMI rising from 51.6 to 53.6. Services led the way with a sharp rise from 51.8 to 53.8. Manufacturing returned to firmer growth at 51.6, up from 50.6.

S&P Global noted that business activity growth “hastened” at the start of Q3, supported by one of the fastest paces of new manufacturing orders in over two-and-a-half years.

However, the upbeat data came with warning signs. Business confidence slipped to an eight-month low, while manufacturers cut back on purchasing and slowed hiring. More critically, price pressures “intensified” during the month, pointing to renewed upside risks for inflation and “adding to the uncertainty for the interest rate outlook.”

RBNZ’s Conway: Tariff fallout to cool NZ inflation

Speaking today, RBNZ Chief Economist Paul Conway said rising global tariffs and economic uncertainty are likely to “reduce medium-term inflation pressures” in New Zealand, and drag on the country’s economic rebound through mid-2026. While the US faces rising costs from tariff-induced supply chain disruptions, Conway said New Zealand is more likely to experience disinflation due to lower global growth and falling import prices.

He highlighted that strong export prices—particularly for dairy and beef—alongside lower domestic interest rates are supporting the economy for now. But widespread uncertainty is causing both consumers and firms to take a wait-and-see approach, which is curbing spending and delaying investment decisions.

Given this backdrop, Conway confirmed that the RBNZ retains a dovish tilt. If inflation continues to ease as expected, there is “scope to lower the OCR further”.

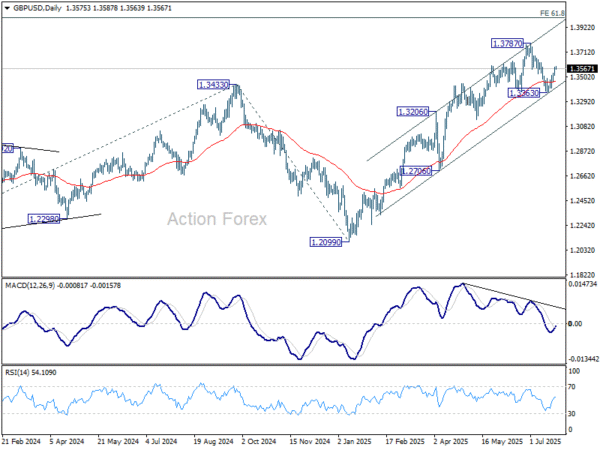

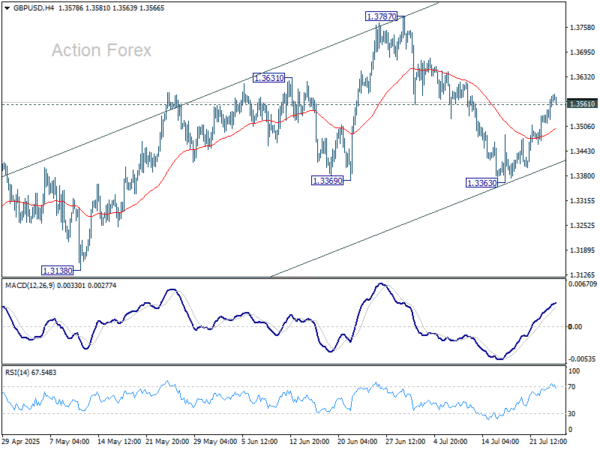

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3535; (P) 1.3560; (R1) 1.3604; More…

GBP/USD’s break of 1.3561 support turned resistance suggests that correction from 1.3787 has completed at 1.3363 already. Intraday bias is back on the upside for retesting 1.3787. Firm break there will resume whole rally from 1.2099 to 1.4004 fibonacci level. For now, risk will stay on the upside as long as 1.3363 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.