Dollar is trading mixed in early US trading on Tuesday, reflecting a cautious tone across the broader market. Treasury yields appeared to have found a foothold, with 10-year stabilizing around 4.2%, helping to curb recent Dollar softness. Traders appear to be waiting for the next catalyst — likely today’s ISM Services data — to drive a more decisive move in yields and FX.

US President Donald Trump’s wide-ranging CNBC interview, which touched on Fed leadership and upcoming tariffs, stirred little immediate market reaction. Still, the content could hold longer-term implications for monetary policy and trade. Trump indicated he has narrowed the list of potential Fed chair successors to four names, excluding current Treasury Secretary Scott Bessent. The field is believed to include Kevin Warsh, Kevin Hassett, and possibly Fed Governor Christopher Waller — all considered policy doves.

Trump didn’t rule out the possibility of appointing a “shadow chair” to undermine Jerome Powell before his term ends in May 2026. That comment, while speculative, will likely raise eyebrows among investors concerned about central bank independence. The identity and stance of the next Fed chair — or their perceived influence — could become a growing driver of market expectations in the coming months.

Currency markets remain broadly indecisive. Yen is the weakest performer today sofar, reversing early gains seen during the Asian session. Euro follows as the second-softest, while the Kiwi also underperforms. Sterling is leading the day, boosted by relative strength in crosses, with Aussie and Dollar rounding out the top three. Swiss Franc and Canadian Dollar are sitting in the middle of the pack.

On the trade front, Trump revealed plans to impose new tariffs on semiconductors and chip imports, citing the need to re-shore manufacturing. He said the announcement could come “within the next week or so,” but offered few specifics.

Meanwhile, Switzerland is scrambling to head off a 39% tariff hike on its exports to the US. Swiss President Karin Keller-Sutter and Economy Minister Guy Parmelin have flown to Washington to hold emergency talks with US officials. The Swiss government has offered to improve its trade terms, but it remains unclear whether the outreach will lead to a meeting with Trump or concrete concessions.

European data wrap: Eurozone PMI leaves room for one more ECB cut

In the Eurozone, PPI rose 0.8% mom and 0.6% yoy in June, slightly missing monthly expectations but beating on the annual rate. Energy prices surged 3.2% on the month, offsetting modest gains elsewhere. Intermediate goods prices slipped -0.2%, reflecting some ongoing input cost disinflation in the manufacturing sector.

More encouragingly, Eurozone PMI Services was finalized at 51.0 in July, up from June’s 50.5. Composite PMI rose to 50.9 from 50.6. Germany and Italy showed gains, while Spain led the bloc at a five-month high of 54.7. France, however, slipped to a three-month low of 48.6. HCOB noted that services inflation is easing, with input costs growing at the slowest pace in nine months. That, alongside decelerating wage growth, strengthens the case for one more ECB rate cut in the second half of the year.

In the UK, the tone was more cautious. July’s PMI Services was finalized at 51.8, down from June’s 52.8, while Composite PMI eased to 51.5 from 52.0. Despite softer prints, S&P Global noted that business confidence improved, supported by receding US tariff concerns and hopes for domestic rate cuts later this year.

BoJ minutes hint at hikes post-tariff deal, AUD/JPY extends decline

BoJ’s June meeting minutes, released today, confirmed that several policymakers were open to resuming rate hikes once trade uncertainty subsides. While the minutes are somewhat dated — the meeting took place before the announcement of the US–Japan trade agreement — they reveal a growing consensus that the central bank may return to a normalization path sooner than previously expected. Markets are now turning to Friday’s Summary of Opinions from the more recent July meeting, which should reflect a more upbeat outlook following the tariff deal.

Some BoJ members noted that as wages remain firm and inflation slightly exceeds expectations, the Bank would likely “shift away from the current wait-and-see approach and consider resuming rate hikes, if trade friction de-escalates” Others emphasized that while the BoJ should pause rate hikes for now due to uncertainty, it must stay “flexible and nimble,” ready to resume hikes depending on US policy and global developments.

China’s Caixin Services PMI surges to 52.6, on stronger demand and renewed optimism

China’s Caixin Services PMI jumped sharply from 50.6 to 52.6 in July, well ahead of expectations at 50.4, marking the fastest pace of expansion since May 2024. PMI Composite, however, fell from 51.3 to 50.8 as dragged down by weak manufacturing.

According to S&P Global’s Jingyi Pan, the rise was driven by better domestic demand and a notable improvement in external demand, with new export business expanding for the first time in three months. Business sentiment also improved, reaching the highest level since March.

Firms also began hiring again, albeit mostly part-time. Importantly, companies felt confident enough to raise output charges for the first time in six months — a sign that inflation pressures are being more easily passed on to clients.

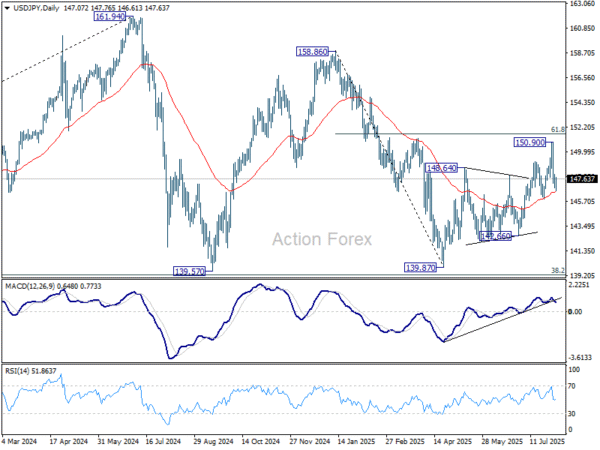

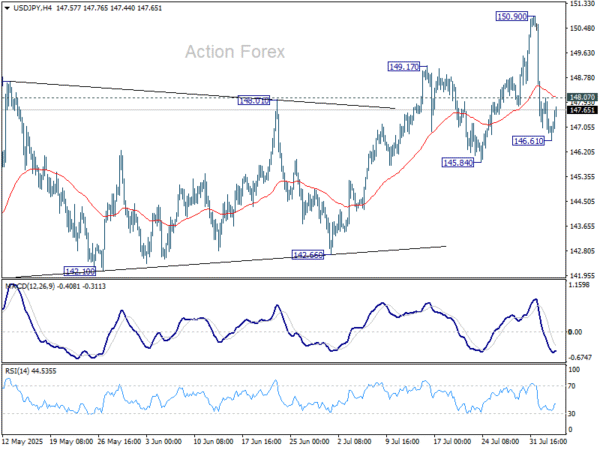

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.60; (P) 147.35; (R1) 147.82; More…

USD/JPY recovered after brief dip to 146.61 and outlook is unchanged. Intraday bias stays neutral at this point. As long as 145.84 support holds, larger rebound from 139.87 is still in favor to continue. On the upside, above 148.07 minor resistance will bring stronger rebound back to retest 150.90. However, on the downside, firm break of 145.84 support will argue that whole rise from 139.87 might have already completed. Deeper fall should then be seen to 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.