Dollar tumbled sharply in early New York trading Friday after much weaker-than-expected non-farm payrolls report. 10-year Treasury yield plunging through the 4.1% level while Gold also surged to fresh record high.

Traders moved swiftly to reprice Fed expectations, with a 25bps cut this month fully baked in and fresh speculation that policymakers may opt for a larger 50bps move. Looking ahead, odds of another 25bps cut in October spiked above 75%, underscoring market conviction that the central bank will need to move aggressively to shield the labor market.

That places next week’s CPI report in sharp focus. Should inflation show further signs of easing, it would open the door for the Fed to accelerate its easing cycle.

In weekly performance terms, Canadian Dollar is faring worst after its own dismal jobs data, while Yen remains under pressure but may recover some ground. Dollar is sliding toward the bottom of the performance table, likely to surpass Yen before the week closes. Euro leads gains, followed by the Aussie and Sterling, with Swiss Franc and Kiwi holding mid-pack.

In Europe, at the time of writing, FTSE is up 0.35%. DAX is up 0.09%. CAC is up 0.15%. UK 10-year yield is down -0.066 at 4.659. Germany 10-year yield is down -0.054 at 2.668. Earlier in Asia, Nikkei rose 1.03%. Hong Kong HSI rose 1.43%. China Shanghai SSE rose 1.24%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield fell -0.029 to 1.576.

US payrolls add just 22k, unemployment edges to 4.3%

US non-farm payrolls showed a sharp slowdown in hiring in August, with employment rising by only 22k, far below the 78k expected. Revisions painted a mixed picture, with July adjusted slightly higher to 79k but June lowered into contraction at -13k.

Unemployment rate ticked up from 4.2% to 4.3% as expected, while the participation rate edged higher by 0.1% to 62.3%. The employment-population ratio was steady at 59.6%, suggesting little improvement in labor utilization despite modest gains in the workforce.

Wage growth remained steady, with average hourly earnings rising 0.3% mom and up 3.7% over the past year. While pay increases are holding, the weak job creation numbers highlight the Fed’s dilemma: inflation may be edging down, but labor market cooling is becoming more pronounced.

Canada employment falls -65.5k, jobless rate jumps to 7.1%.

Canada’s labor market weakened further in August, with employment falling by -65.5k, far below expectations of 4.9k gain. This marked the second consecutive monthly contraction, driven almost entirely by a sharp -60k drop in part-time jobs, while full-time employment was little changed.

Unemployment rate climbed to 7.1% from 6.9%, above expectations, marking the highest level since May 2016 outside the pandemic years. Both the employment rate and participation rate slipped, falling to 60.5% and 65.1%.

Wage growth offered little relief, with average hourly earnings rising 3.2% yoy, slightly slower than July’s 3.3% yoy.

Bonuses lift Japan’s real wages to growth, but consumption recovery weak

Japan’s wage data showed a notable improvement in July, with real wages rising 0.5% yoy, the first increase in seven months. Nominal cash earnings jumped 4.1% yoy, far above expectations of 3.0% yoy, marking the 43rd consecutive month of annual gains.

Wage growth was boosted by a 7.9% yoy surge in special earnings, primarily reflecting summer bonuses, alongside a 2.5% yoy rise in base salaries and a 3.3% yoy increase in overtime pay, the strongest since late 2022.

However, inflation continues to erode some of those gains. Consumer prices used to calculate real wages rose 3.6% in July, still well above the BoJ’s 2% target. Food prices, especially rice, remained a major driver.

Also released, household spending increased 1.4% yoy, falling short of forecasts, though seasonally adjusted monthly spending posted a stronger 1.7% mom gain. A Ministry official said the uptick in spending was largely due to higher electricity bills and auto-related costs, while purchases of everyday food items remain subdued. “The recovery in consumer spending is not robust,” the official cautioned.

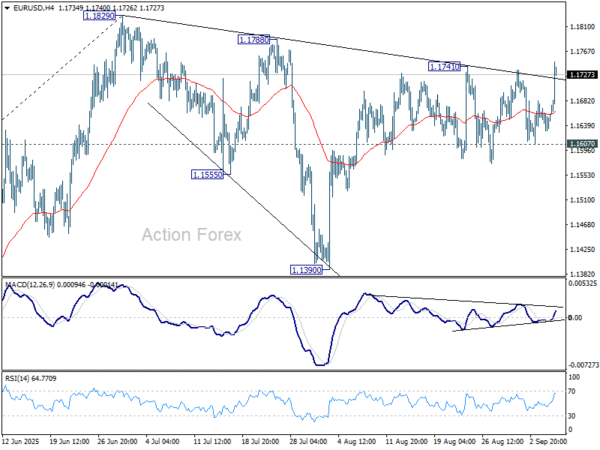

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1650; (R1) 1.1669; More…

Intraday bias in EUR/USD is back on the upside with breach of 1.1741 resistance. Further rise should be seen to retest 1.1829 high. Firm break there will resume larger up trend and target 1.1916 projection level. Further rally is now expected as long as 1.1607 support holds, in case of retreat.

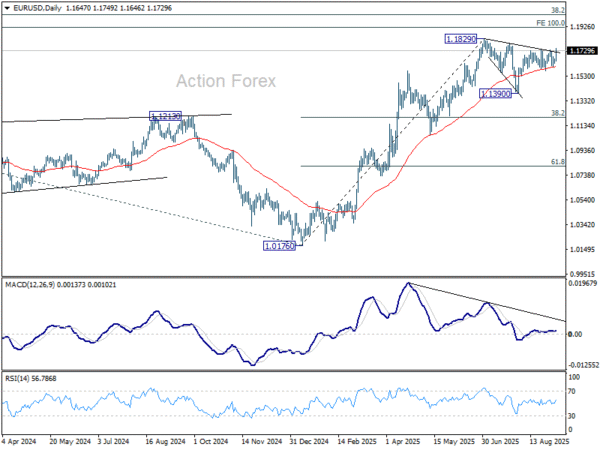

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.