Dollar weakened broadly today, though without a clear catalyst. Month-end flows are likely in play, while traders turned cautious ahead of what is expected to be a volatile September. With key U.S. releases looming, positioning appears lighter as investors await more decisive signals. Beyond tomorrow’s US PCE data, the focus now is squarely on the next two weeks. U.S. nonfarm payrolls and CPI will shape the Fed’s policy outlook, determining whether markets are correct to price a September cut.

For now, Dollar was the weakest currency of the day, followed by Swiss Franc and Sterling. On the other side, Aussie outperformed, while Euro rebounded from earlier weakness. Kiwi also gained ground, while Yen and Loonie held mid-pack.

While overall market conditions remain sluggish, the standout move came from the Chinese Yuan. USD/CNY fell to its lowest level since last November, reflecting stronger demand for Chinese assets. A-shares surged to a 10-year high earlier in the week, signaling renewed investor appetite.

Reports suggest that since mid-April, the CNY’s daily central parity has followed a steady, controlled strengthening trend, with regulators guiding the exchange rate higher deliberately. If incoming data continue to show stabilization in China’s growth outlook, the room for further CNY appreciation could widen……

In Europe, at the time of writing, FTSE is down -0.30%. DAX is up 0.17%. CAC is up 0.52%. UK 10-year yield is down -0.007 at 4.732. Germany 10-year yield is up 0.013 at 2.716. Earlier in Asia, Nikkei rose 0.73%. Hong Kong HSI fell -0.81%. China Shanghai SSE rose 1.14%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield fell -0.008 to 1.619.

US initial jobless claims fall to 229k vs exp 231k

US initial jobless claims fell -5k to 229k in the week ending August 23, below expectation of 231k. Four-week moving average of initial claims rose 2.5k to 228.5.

Continuing claims fell -7k to 1954k in the week ending August 16. Four-week moving average of continuing claims rose 4.5k to 1956k.

ECB sees case for another cut but greater value in waiting for September

ECB’s July meeting accounts highlighted that, while current conditions remain consistent with another rate cut, policymakers see a “high option value” in waiting until September.

Rates were judged to be in “broadly neutral territory” after eight cuts in nine meetings, financial conditions remained stable, and inflation was viewed as “in a good place” relative to the medium-term target.

The minutes stressed that uncertainty—ranging from trade disputes to geopolitical risks—warrants patience. Holding policy steady provides time to evaluate the impact of earlier cuts and to monitor data on manufacturing, services inflation, exchange rates, and financial markets, as well as the outcome of trade negotiations.

September was singled out as the point when fresh staff projections and new data would give a clearer reading of the economy’s underlying direction. Policymakers highlighted that this would help to resolve “counteracting forces” currently obscuring the signals.

While some argued for “a further rate cut” given “increasing downside risks to output and inflation”, the dominant view favored patience. By waiting until September, the ECB preserves flexibility and ensures any further move is better informed by the latest evidence.

Switzerland posts 0.1% Q2 GDP growth, SECO cuts forecasts on US tariffs, rules out deep recession

Switzerland’s economy grew just 0.1% qoq in Q2, in line with expectations, as SECO noted that the “anticipated correction” followed above-average growth earlier this year. Industrial output and exports contracted sharply, while services posted broad-based gains.

SECO also issued an updated scenario reflecting the drag from new U.S. tariffs on Swiss imports, warning the economy is now likely to expand more slowly than previously projected. T

The Federal Government’s June forecast had already pointed to below-average growth, with GDP seen at 1.3% in 2025 and 1.2% in 2026. The revised simulation now pegs growth at just 1.2% in 2025 and 0.8% in 2026, citing the August introduction of higher tariffs.

While a severe recession is not anticipated, SECO warned that the impact could be significant for exporters and certain industries exposed to U.S. demand.

NZ ANZ business confidence rises to 49.7, weak spots reinforce RBNZ’s dovish tilt

New Zealand’s ANZ Business Confidence index improved modestly in August, rising to 49.7 from 47.8. However, firms’ Own Activity Outlook slipped to 38.7 from 40.6. Sector pressures also persisted, with reported employment in construction falling sharply.

Inflation indicators eased further. The share of firms expecting to raise prices in the next three months fell to 43%, while cost expectations edged down to 74%. One-year inflation expectations also dipped to 2.63% from 2.68%. Wage growth expectations 12 months out softened to 2.4% from 2.5%.

ANZ said the survey aligns with the RBNZ’s updated view that the economy requires “a little more support” to ward off downside risks. While confidence is stabilizing, the recovery will unfortunately “not come soon enough for some”.

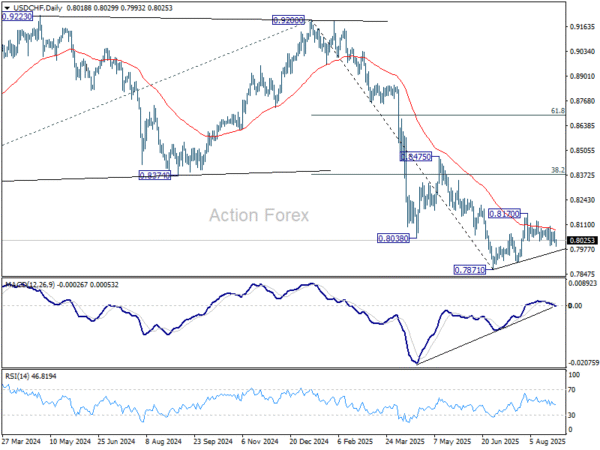

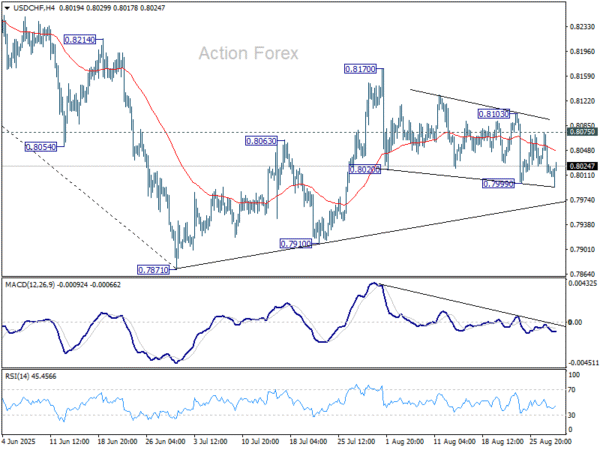

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8001; (P) 0.8038; (R1) 0.8061; More….

Intraday bias in USD/CHF is back on the downside with breach of 0.7999 temporary low. Fall from 0.8170 is resuming, and should target 0.7910 support first. Break there will bring retest of 0.7871 low. On the upside, however, break of 0.8073 will turn bias to the upside for 0.8103. Further break there will resume the rebound from 0.7871 through 0.8170 resistance.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.