Dollar is softening again across the board in a session marked by light news flow and no scheduled economic data from the US. With little fresh macro direction, traders are shifting their attention to upcoming comments from Fed officials, including Boston Fed President Susan Collins and Fed Governor Lisa Cook. Their views on the labor market will be closely parsed following last Friday’s disappointing nonfarm payrolls report.

Markets have increasingly priced in a September rate cut, with odds now near 87%. The focus will be on whether Collins and Cook signal comfort with further easing, particularly in light of slowing job growth. Any indication that the Fed is moving closer to action could reinforce the Dollar’s slide, especially in a low-volume environment.

Elsewhere in FX, Swiss Franc is among the weakest performers. Markets are increasingly resigned to the reality that Switzerland is unlikely to secure a last-minute reduction in the 39% US import tariffs set to take effect this week. Meanwhile, Meanwhile, Yen also remains weak, as traders show little appetite for safe-haven positioning without a clearer risk-off signal.

On the stronger side, Kiwi and Aussie are leading gains. The move may reflect a mild shift toward risk-on positioning, although that’s not yet clearly confirmed by global equity indices. Euro is also firming, with EUR/CHF in particular showing signs of readiness for bullish breakout from its recent consolidation range. Sterling and the Canadian Dollar are trading more mixed in the middle.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is down -0.03%. CAC is up 0.17%. UK 10-year yield is down -0.012 at 4.51. Germany 10-year yield is up 0.007 at 2.641. Earlier in Asia, Nikkei rose 0.60%. Hong Kong HSI rose 0.03%. China Shanghai SSE rose 0.45%. Singapore Strait Times rose 0.45%. Japan 10-year JGB yield rose 0.025 to 1.501.

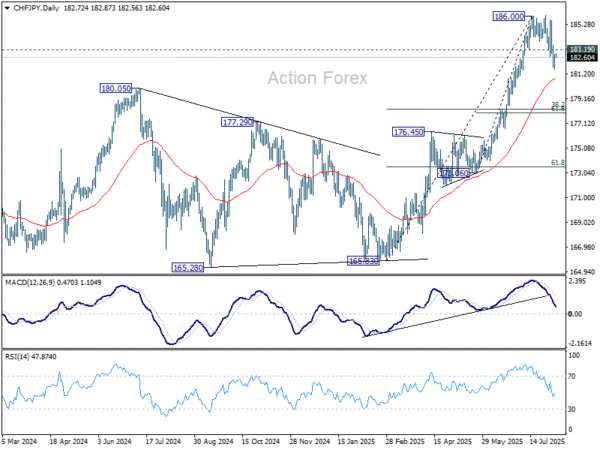

Franc hit by tariff shock, CHF/JPY drops towards 180, but 178 should hold

Swiss Franc has come under heavy pressure since early August, with trade tensions driving much of the weakness. The US stunned markets last week by imposing a 39% tariff on Swiss imports, accusing Bern of failing to make “meaningful concessions” on trade. The duties, effective Thursday, will impact a broad swath of Swiss exports — including high-value goods like pharmaceuticals and luxury watches — which are heavily reliant on access to the US market.

Swiss officials have scrambled to Washington in a final attempt to prevent the tariffs from being implemented. President Keller-Sutter and Business Minister Parmelin arrived Tuesday, and a meeting with US Secretary of State Marco Rubio is scheduled for Wednesday. With no confirmed talks yet with US trade or commerce officials, hopes for a breakthrough might be fading, further weighing on the Franc.

CHF/JPY is reflecting this pressure technically, with the pair confirming a short-term top at 186.60 after breaking support at 183.19. Near-term outlook favors a deeper correction to (now at 180.79) and possibly below.

But strong support should emerge around 178 support zone, (61.8% retracement of 173.06 to 186.00 at 178.00 and 38.2% retracement of 163.83 to 186.00 at 178.29) to contain downside. Large up trend is expected to resume through 186.00 at a later stage, if tensions with Washington ease in the coming weeks.

European data wrap: UK construction slumps, Eurozone data miss

The UK construction sector saw a sharp deterioration in July, with the PMI plunging to 44.3 from 48.8 — its lowest level since May 2020 and far below the expected 49.2.

According to S&P Global, British firms cited a lack of tender opportunities and growing hesitancy from clients amid both domestic and international uncertainty. The data reinforces broader concerns about the UK’s economic momentum heading into the second half of the year.

In the Eurozone, June retail sales rose 0.3% mom, shy of the expected 0.4% mom. Modest gains were seen across food, non-food, and fuel categories. Adding to the downbeat tone, German factory orders unexpectedly declined by -1.0% mmm in June, missing forecasts for a 1.0% mom rise.

Japan real wages remain negative despite stronger 2.5% nominal growth

Japan’s real wages continued to contract in June, falling -1.3% yoy — the sixth straight month of decline. While that marked an improvement from May’s revised -2.6% yoy drop, persistent inflation, particularly in food prices, continues to erode household purchasing power. Consumer prices used for wage calculations rose 3.8% yoy in June, far outpacing nominal wage gains.

Nominal wages climbed 2.5% yoy, up from 1.4% yoy in May and rising for the 42nd consecutive month. However, the reading missed expectations of 3.2% yoy, tempering the positive headline. Base pay rose 2.1% yoy, and special earnings — mainly bonuses — grew 3.0% yoy, supporting a modest rise in overall pay levels during the reporting month.

NZ unemployment rate rises to 5.2%, RBNZ August cut in play

New Zealand’s Q2 labour market report confirmed continued softening, with employment falling -0.1% qoq and unemployment edging up to 5.2%. That marks the highest jobless rate since 2020, though still slightly below consensus of 5.3%. Participation rate also dropped -0.2 points to 70.5%, its lowest since early 2021, suggesting a cooling in demand.

Wage growth offered a mixed signal to the RBNZ. The private sector wage index rose 0.6% qoq, higher than expected 0.5% qoq and up from Q1’s 0.4%. But annual wage inflation slowed from 2.5% to 2.2% — the lowest in over three years — hinting that longer-term wage pressures are easing.

The overall report doesn’t deviate much from RBNZ’s May projections and is unlikely to alter its near-term stance. With inflation running at 2.7% yoy in Q2, markets still expect one more 25bps rate cut from the current 3.25% this month. But the central bank is likely to stay cautious on signaling further easing until price and wage dynamics show more decisive downside momentum.

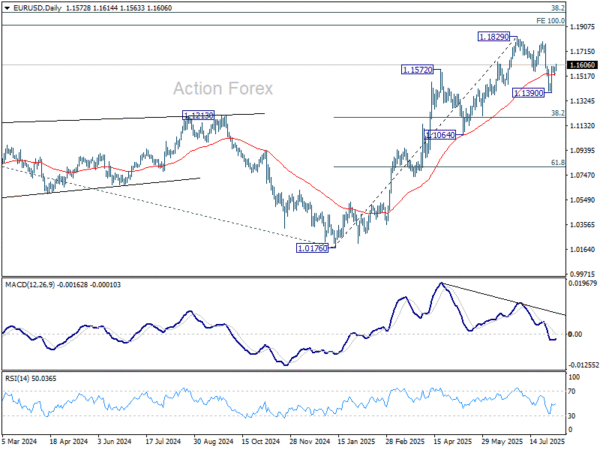

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1539; (P) 1.1564; (R1) 1.1599; More…

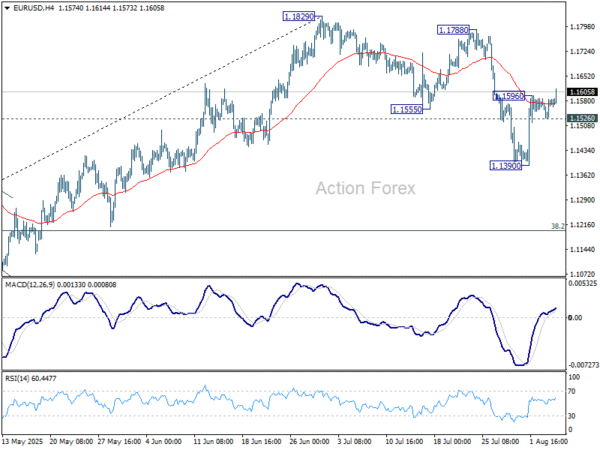

EUR/USD’s rebound from 1.1390 resumed after brief consolidations and intraday bias is back on the upside. Current development affirms that case that fall from 1.1829 has completed as a three-wave correction. Further rally should be seen to retest 1.1788/1820 resistance zone. On the downside, however, break of 1.1526 minor support will dampen this view and bring retest of 1.1390 instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.