The foreign exchange market remains largely range-bound as traders await today’s U.S. non-farm payrolls report. Recent labor indicators, including ISM employment components, point to downside risk for NFP. Both manufacturing and services sub-indexes remain in contractionary territory, while ADP payrolls growth slowed sharply in August. This suggests a soft report is more likely than not.

Besides, the implications for Dollar are asymmetric. A weak payrolls print—particularly a sizeable miss—could spark a sustained wave of Dollar selling as traders price in more aggressive Fed action, including the possibility of back-to-back cuts. By contrast, a stronger report may only limit the pace of easing rather than shift the direction, implying any lift for the dollar would be temporary.

Canada’s employment report is also in focus, with markets watching closely to see if the data justify expectations that BoC could resume rate cuts this month.

On trade, US President Donald Trump signed an executive order Thursday to finalize the July agreement with Japan, imposing a 15% baseline tariff on most Japanese imports, including autos. The confirmation removes a significant uncertainty for the BoJ, which can now reassess the scope for further rate hikes later this year.

Trump also signaled fresh pressure on the tech sector, warning that “fairly substantial” tariffs are coming on semiconductor imports from firms that refuse to relocate production to the U.S. Companies with domestic expansion plans, such as Apple, would be spared.

For the week so far, Dollar remains the best performer. Aussie and Euro follow, while Yen lags as the weakest major. Kiwi and Swiss Franc also underperform, while Sterling and Loonie sit mid-table.

In Asia, Nikkei rose 1.06%. Hong Kong HSI is up 1.29%. China Shanghai SSE is up 1.21%. Singapore Strait Times is up 0.32%. Japan 10-year JGB yield fell -0.03 to 1.575. Overnight, DOW rose 0.77%. S&P 500 rose 0.83%. NASDAQ rose 0.98%. 10-year yield fell -0.035 to 4.176.

Dollar on watch as NFP looms, risks tilt to downside

All attention is on U.S. non-farm payrolls today, with markets bracing for heightened volatility. Consensus expectations point to job growth of 78k in August, an uptick in the unemployment rate to 4.3%, and average hourly earnings at 0.3% mom. Risks appear skewed to the downside for Dollar, with potentially larger reaction if the data disappoints.

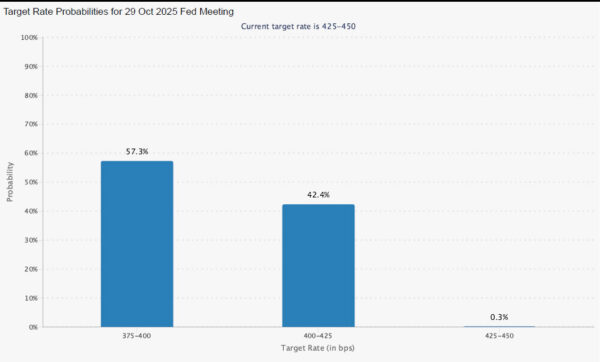

While some policymakers, including Chicago Fed President Austan Goolsbee, remain undecided, the broader consensus is that the Fed will cut rates by 25 bps later this month. A slightly stronger-than-expected NFP print could temper expectations for additional easing but is unlikely to derail the September cut.

In fact, a robust report would most likely reduce odds of a follow-up move in October, currently priced at just above 50%. Any Dollar bounce on strong payrolls may prove temporary, as the Fed remains on a path toward lower rates, albeit at a slower pace.

Conversely, a weaker-than-expected report could spark fears that the Fed is already falling behind the curve. In such a scenario, traders may begin to price in the possibility of a 50 bps cut this month—currently given a zero chance—or boost bets on back-to-back cuts in October and December. That would almost certainly trigger renewed dollar selling.

Supporting the downside risk narrative, recent labor indicators have softened. The ISM services employment subindex held at 46.5, while manufacturing employment edged only slightly higher to 43.8. The ADP private payrolls report showed just 54k new jobs in August, down sharply from 106k in July. Initial jobless claims have also trended higher, with the four-week average rising to 231k from 221k.

For EUR/USD, technicals reinforce the potential for Dollar weakness. The pair remains supported by its 55 Day EMA, consolidating between 1.1573 and 1.1741. Break above 1.1741 would pave the way toward 1.1829to resume the larger up trend from 1.0176.

Alternatively, a break below 1.1573 would extend the corrective pattern from 1.1829 with another falling leg back towards 1.1390 support. Uptrend resumption is only delayed in this case.

Fed’s Williams sees gradual return to neutral rates, tariffs still a drag

New York Fed President John Williams said Thursday that monetary policy is now “modestly restrictive” and appropriate for current conditions, but signaled that rates may eventually be guided back toward neutral if progress continues on inflation and employment. Speaking at the Economic Club of New York, Williams said he sees scope for gradual adjustments if his baseline forecast holds.

Williams projected GDP growth between 1.25% and 1.50% this year, with the unemployment rate edging up from 4.2% currently to 4.5% next year. He noted the job market has cooled, and it’s “clearly the case” that hiring risks are tilted to the downside.

On inflation, Williams said tariffs are clearly pushing prices higher, adding an estimated 1.0% to 1.5% to inflation this year. He forecast PCE inflation to average between 3% and 3.25% in 2025 before falling to 2.5% next year and back to the Fed’s 2% goal in 2027. Speaking to reporters, Williams added that upside risks from tariffs have eased “on the margin,” noting that inflation dynamics remain contained despite ongoing trade disruptions.

Separately, Chicago Fed President Austan Goolsbee struck a more cautious tone, saying he has not yet decided whether a cut is appropriate at the September 16–17 FOMC meeting. he described the gathering as a “live meeting,” adding that Friday’s jobs report and upcoming inflation data will be pivotal to his decision.

Bonuses lift Japan’s real wages to growth, but consumption recovery weak

Japan’s wage data showed a notable improvement in July, with real wages rising 0.5% yoy, the first increase in seven months. Nominal cash earnings jumped 4.1% yoy, far above expectations of 3.0% yoy, marking the 43rd consecutive month of annual gains.

Wage growth was boosted by a 7.9% yoy surge in special earnings, primarily reflecting summer bonuses, alongside a 2.5% yoy rise in base salaries and a 3.3% yoy increase in overtime pay, the strongest since late 2022.

However, inflation continues to erode some of those gains. Consumer prices used to calculate real wages rose 3.6% in July, still well above the BoJ’s 2% target. Food prices, especially rice, remained a major driver.

Also released, household spending increased 1.4% yoy, falling short of forecasts, though seasonally adjusted monthly spending posted a stronger 1.7% mom gain. A Ministry official said the uptick in spending was largely due to higher electricity bills and auto-related costs, while purchases of everyday food items remain subdued. “The recovery in consumer spending is not robust,” the official cautioned.

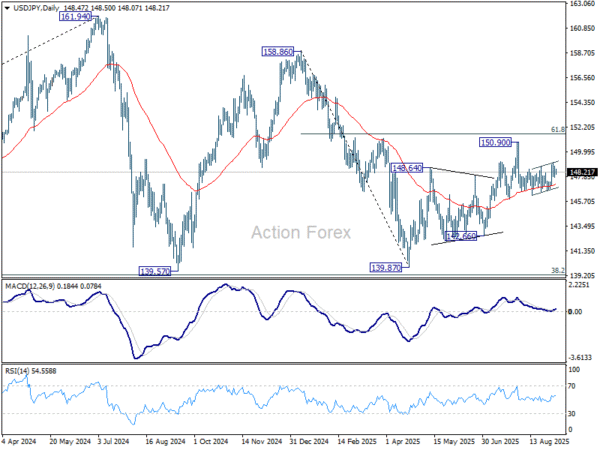

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.91; (P) 148.35; (R1) 148.90; More…

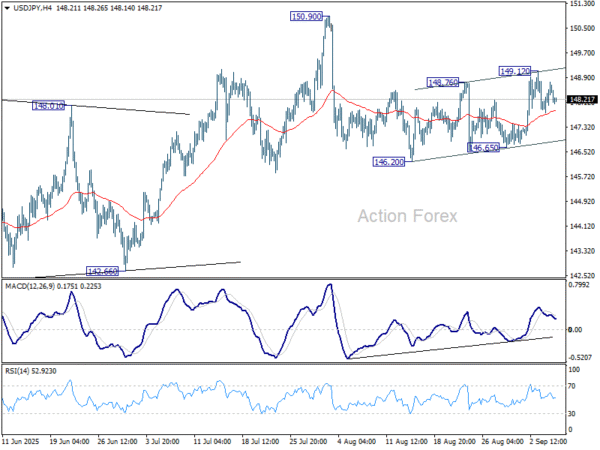

Intraday bias in USD/JPY remains neutral and outlook is unchanged. On the upside, above 149.12 will resume the rebound from 146.20 to retest 150.90 high. Break there will resume the rise from 139.87 to 151.22 fibonacci level. However, on the downside, break of 146.65 support will resume the decline from 150.90 through 146.20 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.