Dollar is staging a firm rebound heading into Friday’s New York session, reversing most of the earlier weekly losses. While durable goods orders for June came in better than expected, markets largely dismissed the data, recognizing that recent swings in transportation orders are tied more to tariff-driven volatility than to underlying demand.

Instead, the greenback’s strength appears rooted in rising confidence that Fed Chair Jerome Powell will not be fired by President Donald Trump. Despite ongoing verbal pressure, Trump told reporters he doesn’t believe dismissing Powell is “necessary,” suggesting that while political interference will persist, the Fed’s leadership remains intact—for now.

On the trade front, Japan clarified the structure of its USD 550B investment deal with the US, which accompanied this week’s tariff agreement. Japan’s top negotiator Ryosei Akazawa emphasized that profit-sharing will be proportional and privately managed, countering claims that Tokyo is giving away funds without returns. US-Japan coordination on joint investments appears to be strengthening.

Meanwhile, South Korea’s push to secure a tariff exemption from the US is entering its final phase. Top ministers are meeting again in Washington with US Commerce Secretary Howard Lutnick, reaffirming a commitment to reach a deal by the August 1 deadline. Seoul is signaling confidence that an agreement is close, though time is short.

Across the currency markets, Dollar remains the weakest performer for the week but could recover further if sentiment holds. Sterling and Loonie follow as laggards. Aussie and Euro. Yen and Swiss franc are trading mid-pack.

In Europe, at the time of writing, FTSE is down -0.33%. DAX is down -0.67%. CAC is down -0.10%. UK 10-year yield is up 0.033 at 4.658. Germany 10-year yield is up 0.036 at 2.741. Earlier in Asia, Nikkei fell -0.88%. Hong Kong HSI fell -1.09%. China Shanghai SSE fell -0.33%. Singapore Strait Times fell -0.28%. Japan 10-year JGB yield rose 0.002 to 1.605.

US durable goods slump -9.3% mom on transport orders

US durable goods orders plunged -9.3% mom to USD 311.8B in June, marking the steepest drop since April 2020. Still, the result was better than consensus forecasts of -11.0% mom decline. The weakness was driven almost entirely by transportation equipment, which tumbled -22.4% mom to USD 113.0B, pulling headline orders sharply lower.

Beneath the surface, however, core figures were more resilient. Orders excluding transportation rose 0.2% mom to USD 198.8B, beating the 0.1% mom forecast. Ex-defense orders slumped -9.4% mom, reinforcing the outsized drag from specific sectors.

ECB forecasters see no enduring disinflation from tariffs

The ECB’s Q3 Survey of Professional Forecasters showed that headline inflation expectations have been revised down across the medium term. HICP inflation is now projected at 2.0% for 2025 (down from 2.2%) and 1.8% for 2026 (down from 2.0%), while 2027 remains unchanged at 2.0%. Core HICP inflation for 2025 is unchanged at 2.3%, but was revised down from 2.1% to 2.0% for both 2026 and 2027.

Respondents cited tariffs as having a small downward effect on inflation in the short term, subtracting roughly -0.06 percentage points from the HICP in both 2025 and 2026, but anticipated no lasting impact beyond that.

On growth, forecasters revised up their 2025 GDP forecast by 0.2 percentage points, trimmed 2026 by 0.1 points, and left 2027 unchanged at 1.4%.

ECB’s Villeroy emphasizes agile pragmatism

French and Finnish ECB officials are urging caution but not complacency as the central bank navigates an increasingly uncertain global environment. Speaking today, François Villeroy de Galhau said growth risks remain “tilted to the downside” and emphasized that “agile pragmatism in light of data and forecasts is of the essence.”

Villeroy also noted that US tariffs—though still not fully defined—are unlikely to spark inflation to rise in the Eurozone. Instead, the recent appreciation of Euro is already exerting a “significant disinflationary effect,” which could aid in anchoring inflation near the ECB’s 2% target.

Separately, Finnish policymaker Olli Rehn echoed the theme of strategic patience, warning that while caution is warranted, the ECB should avoid “waiting in vain.” He stressed the high “option value of waiting.”

ECB’s Kazaks sees pause to continue as inflation settles at 2%

Latvian ECB Governing Council member Martins Kazaks said there is now “value in holding rates at the current levels,” signaling that the era of obvious rate hikes or cuts is over. Speaking in an interview, the central banker stressed that a “steady-hand policy is appropriate,” suggesting little urgency for additional easing from the ECB in the near term.

Kazaks further emphasized that unless the Eurozone economy suffers a major blow, there’s limited justification for lowering interest rates. His stance comes after ECB President Christine Lagarde also struck a cautious tone following yesterday’s decision to keep the deposit rate unchanged at 2.00%.

Separately, Lithuanian Governing Council member Gediminas Šimkus noted “inflation is expected to stay at 2% level in the medium term.”

German Ifo rises to 88.6, but recovery still sluggish

Germany’s Ifo Business Climate Index edged up from 88.4 to 88.6 in July, indicating only marginal improvement in business confidence. Current Assessment Index also ticked higher from 86.2 to 86.5, while Expectations Index held steady at 90.7. The Ifo Institute noted the recovery remains “sluggish,” with no clear acceleration in sight.

By industry, sentiment in manufacturing improved from -13.9 to -11.8, while construction also saw a modest rebound to -14.0. However, services weakened slightly to 2.7, and trade sentiment deteriorated again to -20.2.

UK retail sales rise 0.9% mom in June, but miss forecasts

UK retail sales rose 0.9% mom in June, a solid rebound from May’s -2.8% mom drop, but shy of expectations for a 1.2% mom increase. On a quarterly basis, sales volumes grew 0.2% qoq in Q2, indicating modest underlying momentum.

Fuel sales jumped 2.8% mom—the strongest monthly gain in over a year—while food store volumes also posted a 0.7% mom rise. Online activity remained robust, with non-store sales volumes climbing 1.7% mom and reaching their highest level since February 2022.

Tokyo CPI core slows to 2.9%, but stays elevated

Tokyo’s core CPI (ex-fresh food) eased slightly from 3.1% to 2.9% yoy in July, coming in just below expectations of 3.0% yoy, but still notably above the BoJ’s 2% target.

Headline inflation also slowed from 3.1% yoy to 2.9% yoy. Core-core measure—excluding fresh food and energy—held steady at 3.1%. The stickiness in core-core inflation highlights persistent underlying price pressures.

The figures will feed into the BoJ’s upcoming July 30–31 policy meeting, where the board is widely expected to upgrade its inflation forecast for the current fiscal year. While the data alone may not push the BoJ to act immediately, it strengthens the case for further normalization as inflation remains well above target.

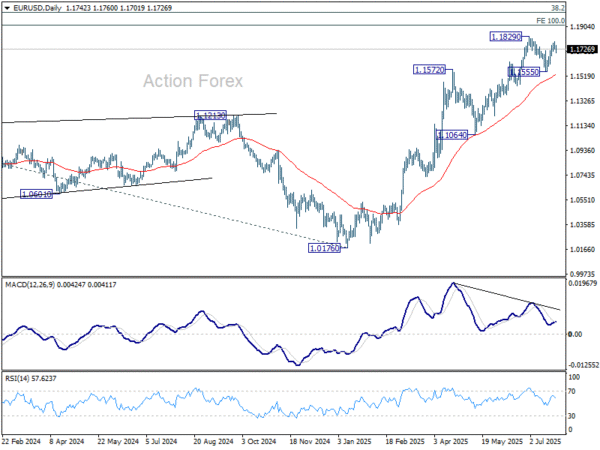

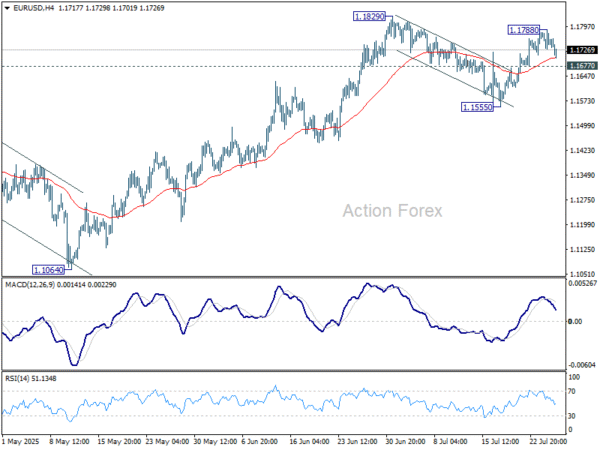

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1756; (R1) 1.1781; More…

Intraday bias in EUR/USD is turned neutral with current retreat. Further rise is favor as long as 1.1677 minor support holds. Firm break of 1.1829 will resume whole rally from 1.0176, and target 1.1916 projection level. However, break of 1.1677 will turn bias to the downside, and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.