Activity in the forex market cooled today as traders adopted a cautious stance ahead of June FOMC minutes. With no major surprises expected, the minutes are unlikely to shift current expectations for a Fed hold at the July 30 meeting. That baseline has been reinforced by the latest shift in trade war dynamics, after US President Donald Trump effectively pushed the tariff truce deadline back to August 1.

The new deadline means Fed will be making its next rate decision before key developments on trade materialize, leaving the central bank in the dark on one of the most important macro variables. With clarity on tariffs likely delayed, Fed officials have even more reason to stick with their current wait-and-see approach. The FOMC minutes may still offer insight into how dovish policymakers like Governor Christopher Waller and Michelle Bowman are positioning, but the broad tone is expected to remain cautious.

On trade, Trump said Tuesday evening that at least seven new tariff letters would be issued Wednesday morning, with more to follow later in the day. He also indicated the EU would be informed of its specific tariff rate “probably” within two days, but added that Brussels had grown more cooperative in recent talks.

European Commission President Ursula von der Leyen maintained a guarded tone, reaffirming that the bloc is working in good faith to strike a deal but remains prepared for all scenarios. A Commission spokesperson said talks were advancing and a deal could potentially be reached before the August 1 deadline.

In terms of currency performance, Dollar continues to lead for the week, although it’s struggling to build further momentum, especially against European majors. Swiss Franc and British Pound remain firm, while the Japanese Yen lags sharply. New Zealand and Canadian Dollars are also under pressure, while Euro and Australian Dollar sit in the middle.

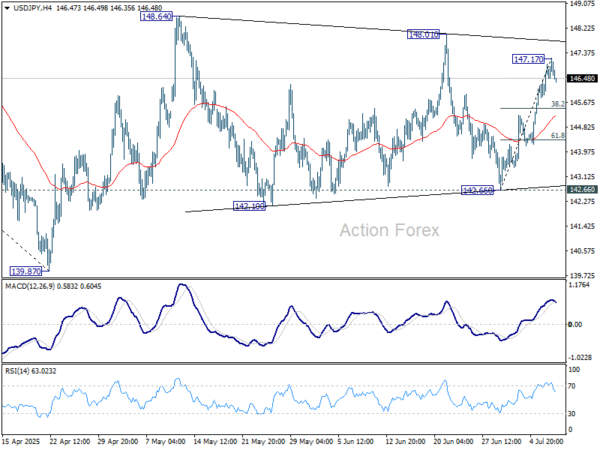

Technically, USD/JPY’s rally from 142.66 appears to be losing steam after hitting 147.17. A short-term pullback is increasingly likely. Recent price action suggests a triangle formation from 148.64, and the next dip may complete that pattern as the fifth leg. Downside would be contained by 61.8% retracement of 142.66 to 147.17 at 144.38. The pair should then be ready to rise through 148.64 to resume the whole rebound from 139.87. Let’s see if it unfolds this way.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is up 1.26%. CAC is up 1.32%. UK 10-year yield is down -0.013 at 4.623. Germany 10-year yield is down -0.012 at 2.68. Earlier in Asia, Nikkei rose 0.33%. Hong Kong HSI fell -1.06%. China Shanghai SSE fell -0.13%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.016 to 1.507.

ECB’s Lane: Global uncertainty goes beyond tariffs, includes investment and security risks

ECB Chief Economist Philip Lane said in a speech today that the recent 25bps rate cut was necessary to prevent temporary inflation undershoots from becoming persistent. Speaking about the June policy decision, Lane emphasized the influence of falling energy prices, a stronger Euro, and a deteriorating materially changed outlook on ECB’s latest projections.

He also highlighted growing uncertainty over the international trade system, citing risks that extend beyond tariffs to include new non-tariff barriers, shifts in investment frameworks, and increased convergence between economic and national security policies.

Against this backdrop, Lane reaffirmed the ECB’s “meeting-by-meeting”. He stressed that “data dependence also extends to the incoming data on policy settings outside the monetary domain”, since shifts in international and domestic policy regimes are highly relevant for future inflation dynamics.

BoE’s Bailey warns of financial vulnerabilities amid global fragmentation

BoE Governor Andrew Bailey cautioned on Wednesday that risks tied to geopolitical tensions and the fragmentation of global trade and financial markets remain high. Speaking on the evolving macroeconomic development, Bailey said the world economy faces “material uncertainty,” and warned that some geopolitical threats have already begun to crystallize, impacting financial market behavior.

He noted a “notable change” in the usual correlations between the US Dollar and other US assets such as equities and Treasury yields. This breakdown, Bailey warned, increases the likelihood of sharp corrections in risk assets, abrupt shifts in allocation, and prolonged periods of market dislocation. Such dynamics could expose vulnerabilities in market-based finance and ripple into the UK by tightening the availability and cost of credit.

Bailey also stressed that trade fragmentation, while geopolitical in nature, has clear economic consequences. “Fragmenting the world economy is bad for activity,” he said, citing basic trade theory. The knock-on effects, he added, would likely weigh on employment and global growth.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that “If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further.”

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

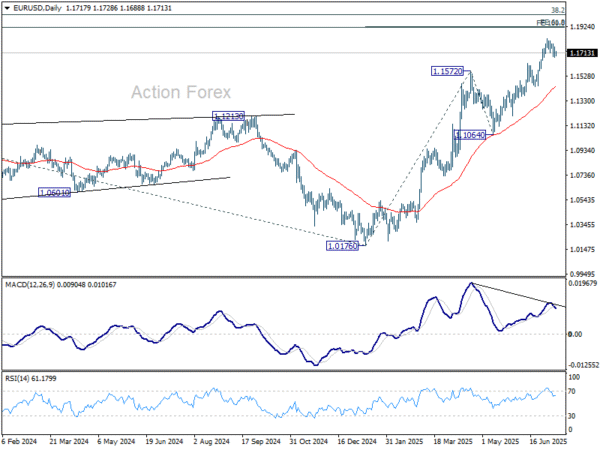

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More…

EUR/USD’s consolidation from 1.1829 is still extending and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.