Dollar is leading the major currencies this week as investors digest an escalating trade war campaign from Washington. While steep tariffs typically raise concerns about disruption to global supply chains and demand, the Trump administration is clearly framing tariffs as a tool not only for reshoring production but also for offsetting revenue losses from recent tax cuts. That has introduced another dimensions to market interpretation, including the prospect of higher fiscal receipts even amid slower global growth.

Treasury Secretary Scott Bessent said Tuesday that the US has already collected USD 100B in tariff revenue this year and is on track for USD 300B by end-2025. That revenue projection has changed the narrative for some, who now view tariffs not just as inflationary trade barriers but also as sources of budget support. The broader economic impact remains uncertain—likely a mix of stagflationary forces—which helps explain why most Fed officials are still signaling caution over the pace and scale of monetary easing.

Markets will turn to FOMC minutes from June’s meeting for clarity. While the minutes are unlikely to shift the firm market consensus that the Fed will hold rates steady this month, they may shed light on the internal division within the Committee—especially whether dovish shifts from Governors Christopher Waller and Michelle Bowman were already emerging at that stage. For now, futures pricing continues to favor a cut in September, but confidence in additional moves this year has softened.

In the currency space, Aussie is second only to Dollar this week, buoyed by the RBA’s surprise decision to hold rates. The Swiss Franc is also firm as risk hedging remains elevated. At the other end, Yen is the weakest major, pressured by Tokyo’s inclusion in Trump’s tariff letters and ongoing concerns over Japan’s export vulnerability. Kiwi lags too, despite mildly recovery following RBNZ’s dovish hold, while Euro is also softer. Sterling and Loonie are trading in the middle of the pack.

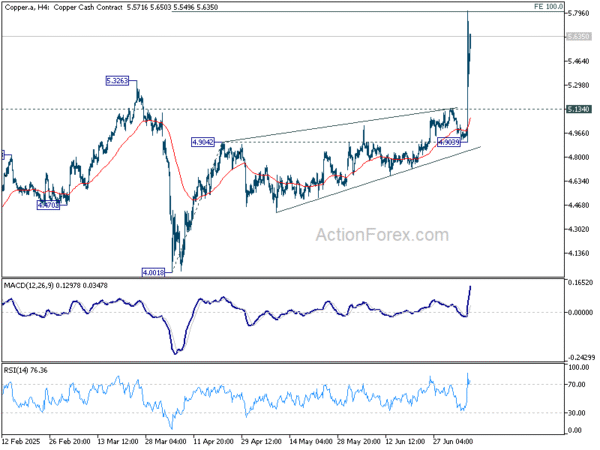

On the trade front, US President Donald Trump on Tuesday proposed a 50% tariff on copper imports, adding to a list of escalating sectoral duties. Commerce Secretary Howard Lutnick said the administration is aiming to bring copper production back home, similar to earlier moves on steel and aluminum. Trump also teased potential 200% tariffs on pharmaceutical imports, reinforcing the administration’s aggressive stance heading into the August deadline.

Copper prices surged to fresh record highs on the news. But technically, copper may be nearing short-term exhaustion after hitting a 100% projection of 4.0018 to 4.9042 from 4.9039 at 5.8063. Upside potential should be limited for now. Though, any retreat should be contained by 5.1340 resistance turned support to bring rebound, to set the range for some sideway trading.

In Asia, at the time of writing, Nikkei is up 0.27%. Hong Kong HSI is down -0.89%. China Shanghai SSE is up 0.38%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is up 0.008 at 1.498. Overnight, DOW fell -0.37%. S&P 500 fell -0.07%. NASDAQ rose 0.03%. 10-year yield rose 0.030 to 4.415.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that “If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further.”

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

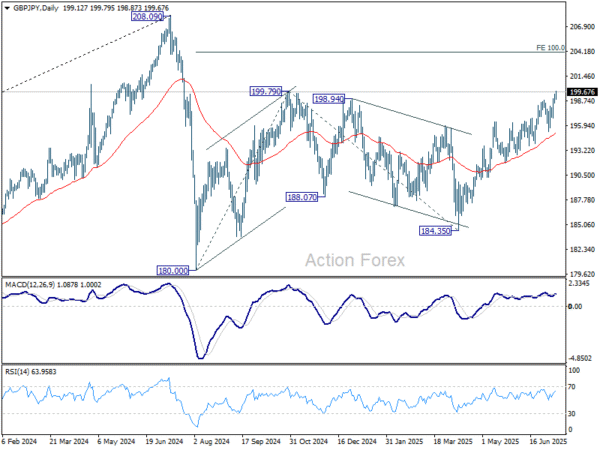

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.66; (P) 199.08; (R1) 199.63; More…

Intraday bias in GBP/JPY remains on the upside for the moment. Firm break of 199.79 resistance will extend the rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14 next. On the downside, below 198.65 minor support will turn intraday bias neutral first. But outlook will continue to stay bullish as long as 195.33 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.