Dollar turned weaker in early US session on Friday despite solid US retail sales data that matched expectations. After a week packed with inflation reports and commentaries from Fed officials, traders are paring back some of their more aggressive Fed easing bets. However, this recalibration has offered little extra support to the greenback.

Market pricing now shows the odds of a September rate cut slipping below the 90% threshold. While a 25bps cut is still the firm consensus for the next FOMC meeting, conviction has softened, with traders looking for further confirmation before committing. Importantly, there’s still one more CPI and nonfarm payrolls print before policymakers gather in September, leaving the situation highly fluid.

The focus has shifted sharply toward Alaska, where US President Donald Trump meets Russian President Vladimir Putin later today. The summit is being closely watched for any breakthrough toward ending the war in Ukraine. Trump has publicly lowered expectations, framing the talks as exploratory, yet has repeated threats of “very severe consequences” if Moscow refuses to move toward a ceasefire. Markets will be alert to whether those threats take tangible form.

Ukraine and European allies, left out of the talks, remain doubtful. Kyiv warns that Russia’s gestures toward peace are disingenuous and claims fresh offensives are being prepared. These accusations, if validated by post-summit developments, could quickly sour global risk sentiment and drive safe-haven flows.

In weekly performance, Dollar’s weakness is most notable against Sterling and Yen, while Euro is also holding gains. Kiwi is the week’s laggard, followed by Loonie and Aussie. Swiss Franc and the greenback itself are stuck in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is up 0.05%. CAC is up 0.52%. UK 10-year yield rose 0.016 to 4.664. Germany 10-year yield rose 0.045 to 2.760. Earlier in Asia, Nikkei rose 1.71%. Hong Kong HSI fell -0.98%. China Shanghai SSE rose 0.83%. Singapore Strait Times fell -0.61%. Japan 10-year JGB yield rose 0.014 to 1.566.

US retail sales match forecasts with 0.5% mom gain

US retail sales rose 0.5% mom in July to USD 726.3B, in line with expectations, suggesting consumer spending momentum remains intact.

Excluding autos, sales rose 0.3% mom, also matching forecasts, while ex-gasoline sales climbed 0.5% mom. The narrower measure excluding both autos and gasoline advanced 0.2% mom.

Over the May–July period, total sales were 3.9% higher than a year ago, pointing to steady year-on-year growth despite elevated price pressures.

Separately, import prices rose 0.4% mom in July, beating expectations for no change. The gain hints at renewed external price pressures, which may partly reflect higher energy prices, but could also be linked to currency movements and tariffs.

Meanwhile, Empire State Manufacturing Index surprised sharply to the upside, jumping from 5.5 in July to 11.9 in August, far exceeding the expected -1.

Japan’s GDP extends growth streak to fifth quarter on strong investment and exports

Japan’s economy expanded 0.3% qoq in Q2, topping expectations of 0.1% qoq. Q1 figures were also revised up to 0.1% qoq growth from a prior estimate of contraction. On an annualized basis, GDP rose 1.0% , marking a fifth consecutive quarter of expansion—a sign of steady, if moderate, momentum.

Capital investment increased 1.3% qoq, extending its growth streak to five quarters, reflecting resilient corporate spending. Exports also provided a boost with a 2.0% rise, outpacing the 0.6% gain in imports, which act as a drag on GDP. The combination of solid external demand and firm investment highlights a balanced growth profile.

Private consumption, which accounts for more than half of Japan’s economic activity, inched up 0.2% qoq. The soft household spending highlights the need for wage growth and consumer confidence to strengthen if Japan is to build on its investment-led momentum and secure a more balanced recovery.

China’s growth momentum fades as July data misses forecasts

China’s July economic activity slowed more than expected, with industrial production rising 5.7% yoy, short of the 6.0% yoy forecast and easing from June’s 6.8% yoy. Retail sales growth also disappointed, up 3.7% yoy versus the 4.6% yoy expected, marking a slowdown from 4.8% yoy in the prior month.

From January to July, fixed asset investment grew just 1.6% yoy, well below the 2.7% yoy forecast and down from 2.8% previously yoy, marking the weakest pace since September 2000. The persistent downturn in the property sector remains a major drag, with property investment contracting -12% yoy over the first seven months.

NZ BNZ PMI back in growth zone as new orders surge

New Zealand’s manufacturing sector returned to growth in July, with the BusinessNZ Performance of Manufacturing Index rising from 49.2 to 52.8, moving back above the historical average of 52.5.

All five sub-indices registered expansion, led by New Orders at 54.2—its highest since March 2022—and Production at 53.6, the strongest since August 2022. Finished Stocks and Deliveries of Raw Materials also posted modest growth, while Employment (50.1) edged back above the no-change level after two months of contraction.

Despite this encouraging turnaround, sentiment among manufacturers remains guarded. The share of negative comments fell to 58.6% from June’s 65.5%.

Respondents continued to highlight weak demand, rising costs, and ongoing economic uncertainty. Tariffs, subdued construction activity, and soft consumer spending were cited as key headwinds, with many firms noting delayed projects and a tendency for customers to place only essential orders.

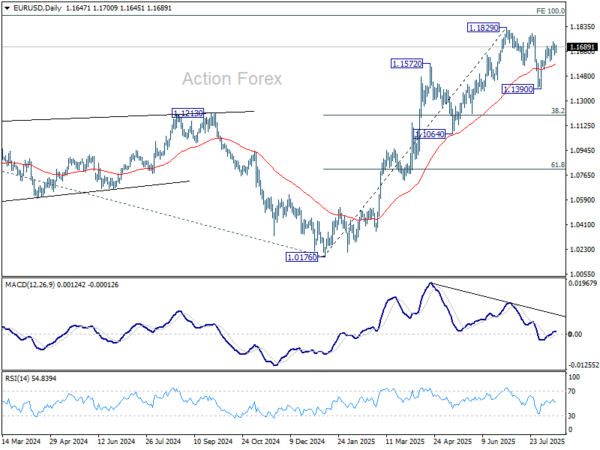

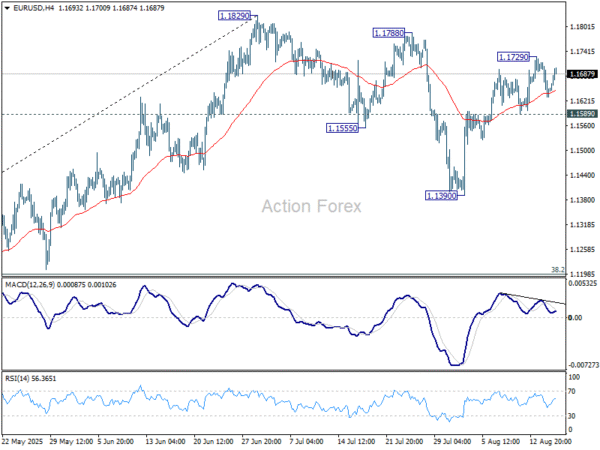

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1615; (P) 1.1665; (R1) 1.1700; More…

EUR/USD recovered after hitting 55 4H EMA but stays below 1.1.729 temporary top. Intraday bias remains neutral and more consolidations could be seen. But further rally is expected as long as 1.1589 support holds. Above 1.1729 will target a retest on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, however, break of 1.1589 support will delay the bullish case and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.