Markets adopted a cautious tone again today, as attention swung back to U.S. economic data. Today’s ADP private payrolls and ISM services figures are seen as key precursors to tomorrow’s highly anticipated nonfarm payrolls. The numbers are expected to sharpen the Fed’s rate-cut calculus, with traders reluctant to take large positions before the release.

Fed officials have broadly indicated openness to a rate cut this month, reinforcing expectations of a 25-basis-point move. Fed fund futures now price the odds of such a cut above 97%, reflecting the market’s conviction that easing is imminent.

The debate, however, is less about September and more about what comes afterward. Even Fed Governor Christopher Waller, a known dove, refrained from endorsing consecutive cuts. While he expects multiple moves over the next three to six months, he stressed that there is no fixed schedule, leaving policymakers room to adapt to incoming data.

On the other end of the spectrum, Atlanta Fed President Raphael Bostic reiterated his preference for a single cut this year, arguing that inflation risks remain the dominant concern. The divide highlights how much weight upcoming data, including Friday’s NFP, will carry in shaping expectations for the policy path into year-end.

Trade risks are also back in focus. US President Donald Trump asked the Supreme Court to fast-track his appeal against lower court rulings that deemed most of his global tariffs illegal. The appeals court ruled last week that Trump overstepped his authority when imposing sweeping levies on nearly all U.S. trading partners.

Trump is pushing for arguments to be heard in November with a decision soon after, warning that a delay until June 2026 could see as much as USD 750 billion to USD 1 trillion in tariffs collected and then potentially unwound—an outcome he says would cause major disruption. Normally, the Supreme Court would not deliver a decision until next summer.

Separately, Japan’s top trade negotiator Ryosei Akazawa departed for Washington for ministerial-level talks, signaling progress in implementing the bilateral trade deal reached in July. “Both Japan and the U.S. have agreed to implement the agreement faithfully and swiftly,” Akazawa said before leaving Tokyo.

In currency markets, Dollar remains the week’s best performer. Aussie and Euro follow, while Yen is the weakest, trailed by Sterling and the kiwi. Franc and Loonie are trading mid-range.

In Asia, at the time of writing, Nikkei is up 1.47%. Hong Kong HSI is down -0.84%. China’s Shanghai SSE is down -1.1%. Singapore Strait Times is up 0.27%. Japan 10-year JGB yield is down -0.027 at 1.610. Overnight, DOW fell -0.05%. S& 500 rose 0.51%. NASDAQ rose 1.02%. 10-year yield fell -0.066 to 4.211.

Fed’s Beige Book shows little growth, tariff pressures building

Fed’s Beige Book indicated that U.S. economic activity was largely stagnant over the past period, with most Districts reporting “little or no change”. Across the board, consumer spending was described as “flat to declining” as wages failed to keep pace with rising prices. Uncertainty and tariffs were frequently cited as additional drags on sentiment.

Employment trends also remained subdued, with 11 of the 12 Districts reporting little or no change in job levels and one District citing a modest decline. On prices, most Districts characterized inflation as “moderate or modest”, though two noted strong input cost increases that outpaced selling prices. Nearly all pointed to tariffs as a key driver of higher costs. Looking ahead, firms widely expect prices to continue rising, with three Districts warning the pace of increases could accelerate further.

Fed’s Kashkari: Neutral rate at 3% leaves room to ease “gently”

Minneapolis Fed President Neel Kashkari said overnight that with the neutral policy rate near 3%, interest rates have “some room to come down gently” over the next couple of years.

Nevertheless, he noted what while headline inflation is being pushed higher by tariffs on goods, other areas like housing are experiencing disinflation, leaving overall price pressures essentially “going sideways.”

Kashkari described the current backdrop as a “tricky situation,” with inflation still too high but the labor market clearly cooling. He stressed that policymakers will need to watch developments carefully before drawing firm conclusions about the path of policy.

While acknowledging risks, Kashkari said he is not forecasting a recession. Instead, he expects the cooling in the labor market to continue in a “somewhat gentle” fashion, suggesting the Fed can gradually reduce rates without tipping the economy into contraction.

RBA’s Bullock hints fewer cuts ahead as spending surges, GBP/AUD extends lower

Australian Dollar is holding its ground as one of the strongest performers in FX markets this week, buoyed by upbeat economic data and comments from RBA Governor Michele Bullock.

Australian consumer spending rose 5.1% yoy in July, according to the ABS released today, led by demand for health services, hotels, travel, and restaurants. The data point to resilient household demand despite tighter financial conditions and underline a growing willingness among households to spend after a prolonged stretch of caution.

That strength follows Wednesday’s GDP report, which showed growth of 0.6% in Q2. Discretionary spending surged 1.4% in the quarter, the fastest pace in three years, highlighting that consumption is now a meaningful driver of Australia’s recovery.

Responding to the GDP data, Governor Bullock cautioned overnight that sustained strength in consumption could limit scope for further easing. “If it keeps going, then there may not be many interest rate declines yet to come. But it all depends,” she said.

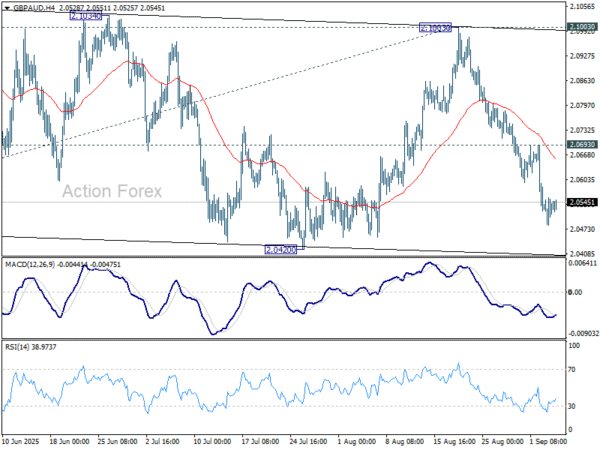

Aussie’s strength stands in contrast to Sterling, which has been weighed down by fiscal concerns. Technically, GBP/AUD extended its decline from 2.1003 this week. Momentum is easing slightly near 2.0420 support level as seen in 4H MACD. But risks remain tilted lower as long as 2.0693 resistance holds. Current fall should be in progress through 2.0420 to 61.8% projection of 2.1643 to 2.0478 from 2.1003 at 2.0283.

The 2.0283 area aligns closely with 55 W EMA now at 2.0265. Decisive move through that zone would suggest that the decline from 2.1643 is evolving into a medium-term downtrend, even if it’s just a correction to the rise from 1.5925 (2022 low).

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3777; (P) 1.3793; (R1) 1.3808; More…

Intraday bias in USD/CAD remains neutral for the moment. On the upside, firm break of 1.3813 resistance will retain near term bullishness that rebound from 1.3538 is still in progress. Intraday bias will be back on the upside for retesting 1.3923 next. On the downside, decisive break of 1.3720 will argue that the corrective pattern from 1.3538 has already completed at 1.3923. Intraday bias will be back on the downside for 1.3574 support first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.