Market activity cooled notably in Asian session today, with major currency pairs and crosses confined to tight ranges. The cautious mood reflects investor focus on the Jackson Hole Symposium, which begins today. The gathering of global central bankers is always a closely watched event, but this year’s comes at a particularly sensitive moment for markets.

The spotlight, of course, is on Fed Chair Jerome Powell’s remarks tomorrow. But in the meantime, headlines will still be populated by interventions from other central bankers, making it a cautious and headline-driven session. This year’s symposium carries extra weight given the backdrop of shifting Fed expectations and recent volatility across asset classes.

The event comes just after the release of the July FOMC minutes overnight, which revealed that most Fed officials maintained caution around tariff risks. That document, however, already looks dated. Since then, the US has reported a much weaker July payrolls report with sharp downward revisions, while early August brought another round of tariff escalations. These developments have significantly shifted the debate inside and outside the Fed.

Still, Fed’s latest dot plot projected two cuts in the second half of the year, suggesting September is the logical window for the first move. Fed funds futures currently price in an 82% chance of a September cut, slightly down from 92% a week ago. The real uncertainty lies in how forcefully the Fed will move after September, with opinions ranging from front-loading cuts to spreading them more cautiously.

This nuance will be critical for market sentiment, particularly with Wall Street already showing cracks. Technology stocks have been under heavy selling pressure this week, with NASDAQ struggling to recover after sharp declines. While the index managed to pare back some losses overnight, it remains vulnerable. Any hawkish surprise at Jackson Hole could amplify risk aversion and extend safe-haven flows into the Yen.

Beyond central bank rhetoric, attention today also turns to flash PMI data. The UK release is especially important after yesterday’s hotter-than-expected CPI print, which raised doubts about another BoE cut in November. For now, markets have pushed back expectations, with a quarter-point cut not fully priced until March 2026, compared with consensus earlier this month for a move by year-end.

A strong PMI reading would add further support to Sterling, though as recent sessions have shown, domestic strength may still be overshadowed by global risk-off sentiment. Sterling’s rebound after CPI data was already capped by souring risk appetite.

On the weekly performance scoreboard, Swiss Franc is currently the strongest currency, followed by Dollar and Yen. At the other end, Kiwi has underperformed badly, followed by Aussie and Sterling, while Euro and Loonie hold middle ground.

In Asia, at the time of writing, Nikkei is down -0.54%. Hong Kong HSI is down -0.25%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is up 0.005 at 1.613. Overnight, DOW rose 0.04% S&P 500 fell -0.24%. NASDAQ fell -0.67%. 10-year yield fell -0.006 to 4.296.

FOMC minutes show Waller, Bowman the dove outliers amid tariff uncertainty

FOMC minutes from July 29–30 meeting showed that while two members, Governor Christopher Waller and Michelle Bowman, dissented in favor of a rate cut, they remained isolated within the Committee. “Almost all participants” judged it appropriate to keep the federal funds rate at 4.25%–4.50%, highlighting the broad consensus to hold steady amid uncertainty.

The discussion revealed a split in emphasis: most officials still see upside inflation risks as “the greater of these two risks”, particularly given tariffs and the risk of unanchored expectations. But a couple of members warned that weakening employment should not be underestimated, reflecting the growing tension between Fed’s dual mandate.

The minutes flagged “considerable uncertainty” over the timing and scale of tariff effects, leaving policymakers braced for potential tradeoffs if inflation proves sticky while labor market softens. Rate decisions, thus, would depend on “each variable’s distance from the Committee’s goal and the potentially different time horizons over which those respective gaps would be anticipated to close.”

Japan’s PMI manufacturing nears expansion at 49.9, but external demand raises sustainability concerns

Japan’s flash PMI data for August showed momentum improving, with the composite index rising slightly from 51.6 to 51.9. Manufacturing posted a surprise recovery, with output climbing back into expansion at 50.5 from 47.6, while the broader PMI Manufacturing rose to 49.9 from 48.9. However, services growth slowed, with the index easing to 52.7 from 53.6.

S&P Global’s Annabel Fiddes noted that the upturn was broad-based, led by a fresh rise in factory production alongside continued service-sector strength. Still, new orders in manufacturing remained weak, raising questions about how sustainable the rebound in factory output will be without stronger demand.

Foreign demand was a drag across both goods and services, leaving the recovery heavily reliant on domestic activity. At the same time, rising input costs squeezed firms’ margins as competitive pressures limited their ability to pass costs on to clients. Selling price inflation slowed to its weakest pace since October, underlining the profitability challenge for Japanese businesses.

Australia PMI composite rises to 54.9, growth broadening, inflation cooling

Australia’s private sector gained momentum in August, with both manufacturing and services showing stronger growth. Manufacturing PMI climbed to 52.9 from 51.3, while Services PMI improved to 55.1 from 54.1. As a result, Composite PMI rose to 54.9 from 53.8, its highest since April 2022, signaling a broadening recovery.

S&P Global’s Jingyi Pan noted that easier interest rates have supported domestic activity, while external demand is also beginning to revive. Export orders picked up, adding to optimism among Australian businesses, and sentiment strengthened notably through the month.

Price pressures, meanwhile, showed signs of easing. Output price inflation pulled back from July’s recent high, a shift that could help sustain demand in the months ahead. That combination of stronger demand and softer price growth points to a healthier balance in the economy and gives RBA space to assess policy moves more carefully in the coming months.

NZ trade swings back into deficit despite broad export gains

New Zealand’s trade balance flipped back into deficit in July, with imports outpacing exports despite solid overseas demand. Goods exports climbed 10% yoy to NZD 6.7 billion, but imports rose 2.6% yoy to NZD 7.3 billion, leaving a monthly deficit of NZD -578 million compared with expectation of NZD 70 million surplus.

Export performance was broadly positive across major partners. Shipments to the EU jumped 28% yoy, while sales to Japan rose 23%. Exports to the U.S. and China also advanced by 7.7% and 7.1% respectively. Australia remained steady with a 4.7% increase.

On the import side, gains were concentrated in the EU and U.S., up 22% yoy and 24% respectively. Purchases from China increased 6.9%, while imports from Australia ticked up by 2.7%. However, imports from South Korea slumped by a sharp -33%.

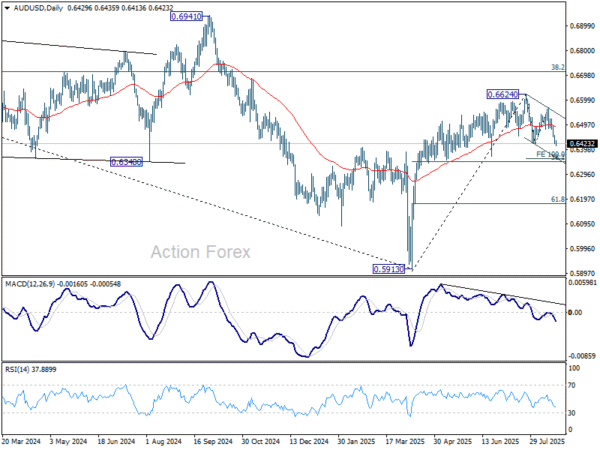

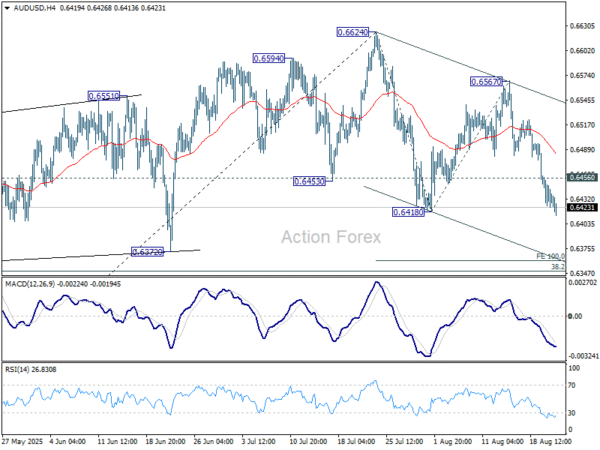

AUD/USD Daily Report

Daily Pivots: (S1) 0.6416; (P) 0.6442; (R1) 0.6461; More…

Intraday bias in AUD/USD stays on the downside for the moment. Firm break of 0.6418 support will resume the whole corrective fall form 0.6624. Next target is 38.2% retracement of 0.5913 to 0.6624 at 0.6352. On the upside, above 0.6456 minor resistance will turn intraday bias neutral again first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).