Forex markets are trading with a relatively subdued tone as the US session gets underway, with limited broad-based momentum among major currencies. The most notable move is a selloff in the Swiss Franc, which appears largely technical, led by a bullish bounce in EUR/CHF.

Meanwhile, Yen is seeing a modest recovery, likely driven by profit-taking after its extended weakness since the start of July. Traders appear reluctant to press shorts further ahead of this weekend’s upper house elections in Japan, which could trigger new fiscal policy shifts and JGB volatility in the days ahead.

Dollar is slightly firmer despite today’s softer-than-expected PPI release. Markets are not placing too much emphasis on the inflation miss, as the dominant driver remains the looming August 1 tariff deadline. Until there is clarity on whether new trade deals are reached or further levies imposed, Dollar positioning is likely to stay cautious.

Sterling is holding its ground near the top of the G10 board after today’s upside surprise in UK inflation. Though the reaction has been modest. Attention now turns to the UK labor market report tomorrow, which could help determine whether August’s rate cut odds remain intact.

For the week so far, Dollar leads the major currencies, followed by Loonie and Sterling. At the bottom are Kiwi and Aussie, with Swiss Franc also under pressure. Euro and Yen are treading in the middle.

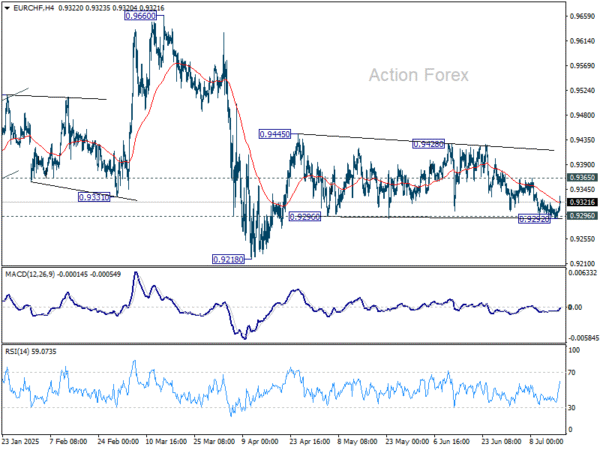

Technically, EUR/CHF’s break of 55 4H EMA offers tentative sign of bottoming at 0.9292, after breaching 0.9296 support briefly. Focus is back on 0.9365 resistance. Break there will argue that corrective pattern from 0.9445 has completed, and the rebound from 0.9218 low is ready to resume.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is up 0.52%. CAC is up 0.02%. UK 10-year yield is down -0.002 at 4.628. Germany 10-year yield is down -0.012 at 2.698. Earlier in Asia, Nikkei fell -0.04%. Hong Kong HSI fell -0.29%. China Shanghai SSE fell -0.03%. Singapore Strait Times rose 0.30%.

US PPI flat in June, misses forecasts

US producer prices were flat in June, falling short of expectations for a 0.3% mom rise. While a 0.3% mom increase in goods prices provided some support, a -0.1% mom dip in services prices offset the gain. PPI excluding food, energy, and trade services was unchanged on the month too.

On an annual basis, headline PPI slowed to 2.3% yoy from 2.6% yoy, also below forecasts 2.5% yoy. The more stable core measure still rose 2.5% year-on-year.

Eurozone exports rise 0.9% yoy in May while imports fall -0.6% yoy

Eurozone goods exports rose 0.9% yoy in May to EUR 242.6B, outpacing a -0.6% yoy drop in imports to EUR 226.5B, leading to a trade surplus of EUR 16.2B. Intra-Eurozone trade also grew 1.4% yoy to EUR 219.1B, indicating resilient domestic supply chains within the bloc.

For the broader European Union, exports rose just 0.1% yoy while imports fell -2.0% yoy, producing a EUR 13.1B surplus. Bilateral data shows continued divergence: EU exports to the US rose 4.4% yoy while imports from the U.S. fell -7.4%. Exports to China dropped -11.2% yoy, while imports from China rose 3.4%. EU-UK trade data showed a 2.5% yoy increase in exports and a -7.1% drop in imports.

UK CPI rises to 3.6%, goods prices jump, services sticky

UK inflation came in hotter than expected in June. Headline CPI accelerated from 3.4% yoy to 3.6% yoy, above consensus of 3.4%. Core CPI (excluding energy, food, alcohol, and tobacco)also surprised to the upside, rising from 3.5% to 3.7%, versus expectation of 3.5% yoy.

Goods inflation picked up from 2.0% yoy to 2.4%, its highest since October 2023. Services inflation remained stubbornly high, unchanged at 4.7% yoy.

On a monthly basis, CPI rose 0.3%, adding to signs that disinflationary progress may be stalling.

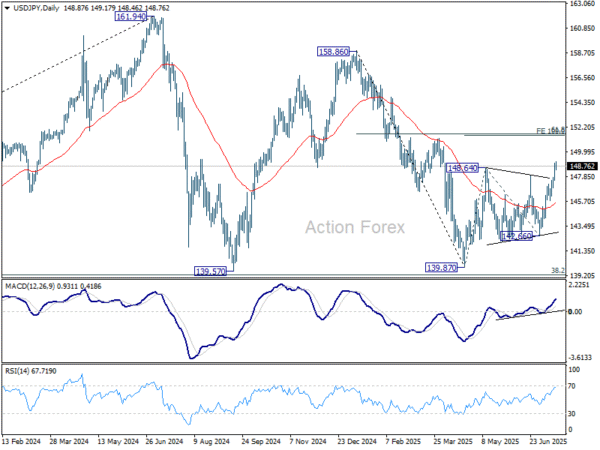

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.93; (P) 148.47; (R1) 149.40; More…

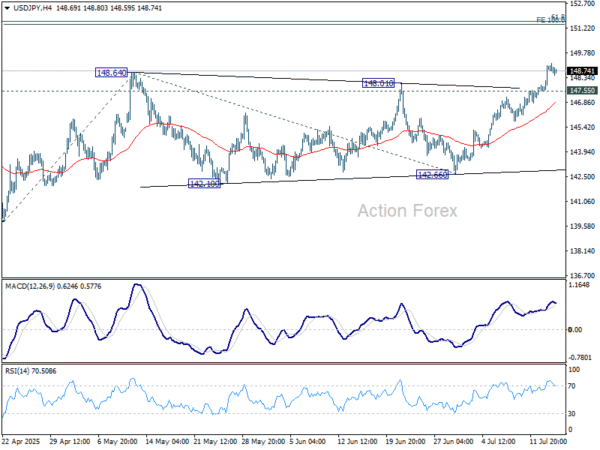

USD/JPY retreats mildly but stays above 147.55 minor support. Intraday bias remains mildly on the upside. Rise from 139.87 is resuming and should target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. On the downside, below 147.55 minor support turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.