Forex markets opened the week on a quiet note, with major pairs and crosses holding tightly within Friday’s ranges during Asian session. Even with last week’s risk-off tone and Wall Street’s steep decline, Asian investors appear to be taking the broader US developments in stride. One outlier is Japan’s Nikkei, which extended its selloff from Friday. Still, the index remains comfortably above the key 40k psychological level, a sign that confidence hasn’t fully eroded. After all, there’s cautious optimism in the region that accelerating Fed rate cuts could eventually support global sentiment.

That said, political tensions in the US are still drawing much attention. US President Donald Trump’s abrupt dismissal of Bureau of Labor Statistics Commissioner Erika McEntarfer, after accusing her of falsifying job numbers, raised fresh concerns over institutional stability. Trump claimed he would name a new BLS head within days, while White House officials attempted to back up his accusation without concrete evidence. Kevin Hassett, head of the National Economic Council, echoed the president’s stance, pointing to “revisions” as proof of wrongdoing.

However, Bill Beach, a former BLS Commissioner and Trump appointee, emphasized that employment figures are compiled by professionals who have served under both parties. He strongly defended the integrity of the agency’s methods. The controversy adds to broader unease after the downward revisions to job growth figures last week further fueled expectations of a Fed policy shift.

On the trade front, Jamieson Greer, the US Trade Representative, said most of last week’s new tariff rates are already locked in. That should ease some market fears about ongoing surprises, though not all negotiations are settle, and several key fronts are unresolved. Most notably, talks with China continue ahead of the August 12 tariff truce deadline, and no agreement has been reached on an extension.

India is also under scrutiny, having just been hit with a 25% US tariff. Stephen Miller warned over the weekend that countries financing Russia’s war “will face consequences,” with Trump hinting at even higher duties if peace talks fail. Canada is pushing back against a 35% US tariff on goods not covered under the USMCA, though Canadian officials expressed optimism over potential progress in talks. These crosscurrents will keep markets alert for further trade developments.

Looking ahead, attention will shift to monetary policy and data. BoE is expected to cut rates by 25bps this week, though internal divisions remain huge. Traders will also parse the BoJ’s latest meeting notes and monitor upcoming ISM Services data, plus Canadian and New Zealand labor reports.

In Asia, at the time of writing, Nikkei is down -1.49%. Hong Kong HSI is up 0.50%. China Shanghai SSE is up 0.21%. Singapore Strait Times is up 0.83%. Japan 10-year JGB yield is down -0.048 at 1.505.

WTI dips on OPEC+ hike, 65 to contain downside in range trade

Crude oil prices slipped on Monday after OPEC+ announced another production boost, this time for September. The group confirmed a planned hike of 547k barrels per day, continuing its aggressive push to regain global market share after years of output cuts meant to prop up prices.

The shift began in April with a small supply increase, but since then OPEC+ has stepped on the gas. May through July each saw 411k bpd added, with larger hikes of 548k in August and now 547k bpd set for September.

Despite briefly surging to nearly 79 in June amid Middle East tensions, WTI crude reversed sharply after the Israel–Iran ceasefire and dropped back to as low as 65.21. The bounce to 71.34 last week failed to sustain, and prices have turned lower again, signaling ongoing sideways consolidation rather than a breakout.

Technically, oil remains trapped in a range. Downside should be anchored near 65, upside appears capped below $73.65. However, even in event of a bounce through 71.34, momentum is expected to fade as oversupply concerns and tepid demand limit further gains below 61.8% retracement of 78.87 to 65.21 at 73.65.

Bitcoin supported by 112k confluence, uptrend still in play

Crypto markets came under pressure last week as risk sentiment soured globally, dragging Bitcoin off recent highs. While the correction was sharp, BTC has found technical footing around a major cluster of support, offering bulls a chance to regroup.

Three key levels are now converging: the prior May high of 112,013, 55 D EMA at 112,331, and trendline support near 111,400. These levels could provide a solid floor for another upside attempt toward the record high at 123,231, assuming broader sentiment doesn’t deteriorate further.

But follow-through may be limited from there as momentum signals suggest caution. Bearish divergence in the daily MACD hints at fading strength, and strong resistance is expected around 100% projection of 49,008 to 109,571 from 74,373 at 134,936 to cap upside.

For now, the uptrend is alive, but ceiling would form below 135k.

BoE eyes another rate cut amid persistent MPC split

BoE is widely expected to deliver another 25bps rate cut this week, continuing its steady pace of one reduction per quarter. That would bring the Bank Rate down to 4.00%. According to a recent Reuters poll, 62 of 75 economists anticipate two more cuts this year — in August and November — keeping the Bank Rate on track to hit 3.75% by year-end.

However, the decision may be far from unanimous. The Monetary Policy Committee remains split, with hawks pointing to persistent inflation risks while doves stress the need to cushion a softening labor market. The middle ground — which has dominated past decisions — still favors a cautious, gradual approach. This internal division is likely to be reflected again in the vote breakdown again, just like the three-way split back in May.

Headline CPI in the UK unexpectedly ticked up to 3.6% in June, reigniting inflation concerns. Survey data also show the public expects stronger price growth ahead. June meeting minutes flagged the risk of rising food prices feeding into broader inflation, and that pressure may force the BoE to revise its 2025 inflation forecast closer to 4%. That’s well above the 2% target and would make it harder for doves to push for a faster pace of easing. Markets will closely watch updated projections for any hawkish tilt that could limit scope for further 2025 easing.

In Japan, the BoJ’s summary of opinions from its July meeting will be scrutinized for signs of how policymakers are responding to the US-Japan trade deal. Optimism about reduced tariff risks could temper some downside concerns. But ongoing trade tensions between the US and other countries, especially China, could have ripple effects across the region.

Another lingering issue is domestic inflation, especially in food. While the BoJ maintains that cost pressures will fade over time, the current pace of increases may challenge that narrative. The tone of the BoJ’s discussions will shape expectations on whether it acts again this year or waits until 2026.

In the US, attention shifts to ISM Services PMI after the sharp downside surprise in last week’s nonfarm payrolls. Markets are growing more confident that the Fed will cut in September, with fed fund futures pricing in nearly 80% probability. A weak ISM read would further validate that view and may raise the likelihood of multiple cuts before year-end. Other data to watch include labor market reports from Canada and New Zealand, and China’s Caixin Services PMI.

Here are some highlights for the week:

- Monday: Swiss CPI, PMI manufacturing; Eurozone Sentix investor confidence; US factory orders.

- Tuesday: BoJ minutes; China Caixin PMI services; Eurozone PMI services final; UK PMI services final; Canada trade balance; US trade balance, ISM services.

- Wednesday: New Zealand employment; Japan average cash earnings; Eurozone retail sales.

- Thursday: Australia trade balance; China trade balance; Swiss foreign currency reserves, unemployment rate; BoE rate decision; US jobless claims; Canada Ivey PMI.

- Friday: Japan house hold spending, BoJ summary of opinions; Swiss SECO consumer climate; Canada employment.

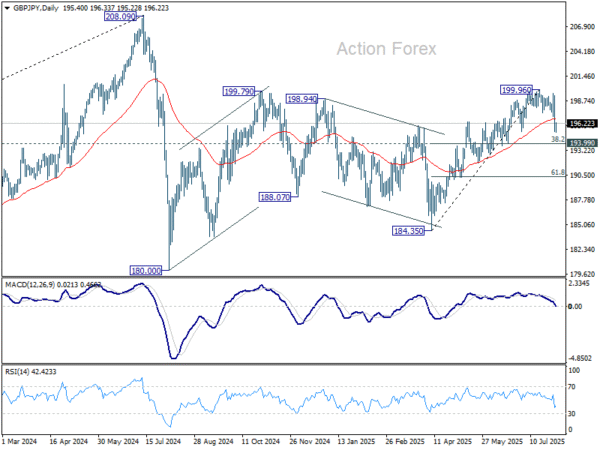

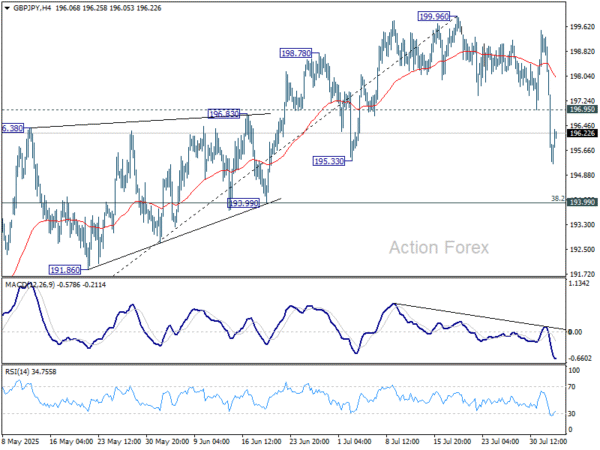

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.28; (P) 196.82; (R1) 198.29; More…

Intraday bias in GBP/JPY stays mildly on the downside for the moment. Fall from 199.96 would extend towards 193.99 cluster support (38.2% retracement of 184.35 to 199.96 at 193.99). Strong support should be seen there to bring rebound, at least on first attempt. On the upside, above 196.95 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.