Closing at $45,711, up +0.43%, the Dow Jones 30 has renewed recent highs in today’s session, breaking above previously held consolidation at around $45,642.

Dow Jones 30 (DJIA): Key takeaways from today’s session

- Up around 7.00% year-to-date, recent developments suggesting the Fed will cut in their upcoming decision are benefiting US equity pricing

- While interest rate cuts stand to benefit Dow Jones pricing, weak jobs data and a potential for infamous ‘stagflation’ could limit upside in the medium term

Dow Jones 30 (DJIA): Interest rate cut predictions boost Dow Jones pricing

Although playing second fiddle to the tech-dominant Nasdaq-100 for much of 2025, the Dow Jones remains around ~7.83% year-to-date, even with zero interest rate cuts, which, on paper, would be negative for index pricing.

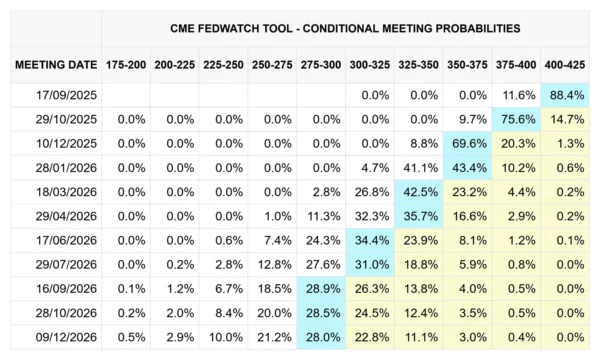

As we all know by now, this could be about to change; most predict that the Fed will cut rates by 25 bps in their upcoming decision, while others are even expecting a cut of 50 bps in response to poor US labour data.

CME FedWatch, 08/09/2025

While the latter remains unlikely compared to a more tame approach, what is more certain is that a Fed rate cut is undeniably positive for the Dow Jones, with the benefit of holding dollars instead of investing set to be lowered for the first time in 2025.

It should be noted that despite the Fed’s choice of tight monetary policy, the Dow Jones has performed fairly well this year, all things considered. While we can expect some short-term upside from expectations of rate cuts, the proof in the metaphorical pudding will be how data reacts to a change in interest rates, especially regarding inflation and labour data

Dow Jones 30 (DJIA): Stagflation fears and poor labour data cast doubt over upside

With poor labour data having virtually cemented the chances of an interest rate cut next week, markets are keenly watching upcoming US inflation data releases to understand whether fears of ‘stagflation’ are justified:

- Core Producer Price Index (MoM) (Aug), Wednesday, September 10th, 08:30 ET

- Core Producer Price Index (YoY) (Aug), Wednesday, September 10th, 08:30 ET

- Producer Price Index (MoM) (Aug), Wednesday, September 10th, 08:30 ET

- Producer Price Index (YoY) (Aug), Wednesday, September 10th, 08:30 ET

- Core Consumer Price Index (MoM) (Aug), Thursday, September 11th, 08:30 ET

- Core Consumer Price Index (YoY) (Aug), Thursday, September 11th, 08:30 ET

- Consumer Price Index (MoM) (Aug), Thursday, September 11th, 08:30 ET

- Consumer Price Index (YoY) (Aug), Thursday, September 11th, 08:30 ET

It’s important to remember that, even if interest rates are to be cut, sentiment and general confidence in the US economy will be the most significant determining factor in equity performance in the near future.

As such, labour and inflation data remain as crucial as ever. When considering the Fed’s dual mandate, here are a couple possible outcomes in the next few months:

- Lower rates boost jobs growth while inflation starts to fall

If a decision to cut rates is made, and the labour market responds well, while inflation starts to fall, we can consider this the best possible outcome. Naturally, this would substantially boost belief in the US economy, which would be US equity positive

2. Lower rates fail to promote jobs growth, while inflation remains stubborn

If the Federal Reserve decides to cut rates and the labour market responds poorly while inflation proves stubborn, this would be a very difficult position to maintain. While further rate cuts would potentially help the labour market, maintaining or even hiking rates would better control inflation, making monetary policy decisions difficult. In this scenario, we can expect higher levels of market uncertainty, which would be generally US equity negative

Dow Jones 30 (US30USD), OANDA, TradingView, 09/09/2025