A political shock in Tokyo is dominating global markets today, with Prime Minister Shigeru Ishiba announcing to step down over the weekend. The surprise resignation boosted risk appetite, propelling Nikkei. Yen, meanwhile, looks increasingly vulnerable. Last week’s dip in U.S. Treasury yields provided only temporary relief, and the currency has quickly reversed lower today. If optimism surrounding Japan’s leadership transition holds and the Nikkei breaks into record territory, Yen’s selloff could extend further in the days ahead.

For Dollar, the picture is mixed after last week’s sharp post-NFP selloff. Markets are now shifting attention to upcoming U.S. CPI and PPI reports, which will be critical in gauging the impact of August’s tariff escalation. After another weak jobs print, the inflation data will be crucial in determining whether the Fed has the flexibility to accelerate easing to support employment.

Euro trading has turned cautious as investors look toward Thursday’s ECB meeting, where policymakers are widely expected to leave the deposit rate unchanged at 2.00%. With inflation near target and unemployment still low, the ECB is seen maintaining its wait-and-see stance after delivering 200bps of cuts over the past year.

Across broader FX markets, the commodity bloc is outperforming, with Kiwi leading gains, followed by Aussie and Loonie. At the other end of the spectrum, Yen is the weakest, trailed by Sterling and Euro. Dollar and Swiss Franc are sitting in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 1.42%. Hong Kong HSI is up 0.53%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is down -0.006 at 1.570.

Japanese stocks soar towards record as Ishiba exit sparks optimism, NZD/JPY breaks higher

Japanese equities surged at the start of the week, with the Nikkei jumping more than 800 points in early trade and holding firm through the morning session. The index now sits within striking distance of a fresh record high. Risk-on appetite spilled over into currency markets, sending Yen sharply lower and leaving it vulnerable to further pressure if sentiment holds.

The trigger was the surprise resignation of Prime Minister Shigeru Ishiba over the weekend. Ishiba said the timing was deliberate, coming days after he secured the formal reduction of U.S. auto tariffs from 27.5% to 15%. “Now that negotiations on U.S. tariff measures have reached a conclusion, I believe this is the appropriate moment to resign,” he told reporters. His departure marks a sudden end to a premiership that began less than a year ago but was hampered by his coalition losing control of the lower house.

Nevertheless, Ishiba’s exit opens the door to fresh leadership amid hopes that new faces could re-energize both the party and the electorate. Koizumi Shinjiro, agricultural minister and son of former prime minister Junichiro Koizumi, is widely viewed as a frontrunner, with his youth and broad appeal resonating with markets. Takaichi Sanae, closely aligned with the late Abe Shinzo, is also expected to be a serious contender. The leadership race is expected to fuel speculation of policy continuity combined with a push for fresh fiscal initiatives.

Investors are betting that the incoming administration will prioritize expansionary fiscal measures to secure opposition cooperation, given the LDP-led coalition still commands only a minority. Such expectations have buoyed equities further and reinforced the risk-on backdrop weighing on Yen.

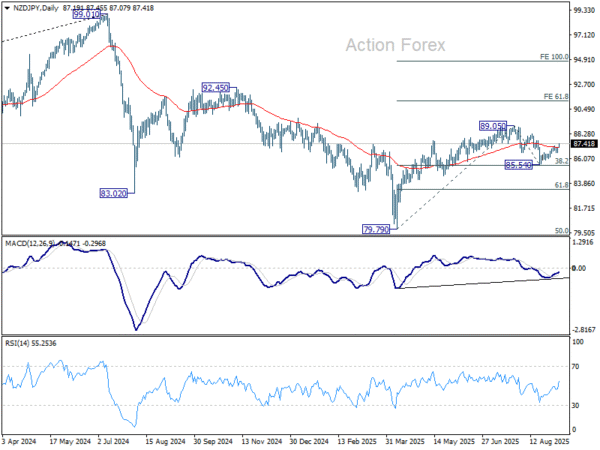

Technically, NZD/JPY’s rally from 85.54 resumed today. The break of 55 D EMA (now at 87.10) suggests that correction from 89.05 has completed after defending 38.2% retracement of 38.2% retracement of 79.79 to 89.05 at 85.51. Further rise is expected as long as 86.61 support holds. Break of 88.33 resistance will indicate that whole up trend from 79.79 is ready to resume through 89.05 short term top.

China exports growth slows in August, US flows collapse -33% yoy

China’s trade report for August showed growing pressure from U.S. tariffs. Exports rose 4.4% yoy, below expectations of 5.0% yoy and the slowest pace in six months. Shipments to the U.S. plunged -33.1% yoy, while flows to Southeast Asia jumped 22.5% yoy, suggesting exporters may be rerouting goods through regional partners to cushion losses.

Imports also disappointed, rising just 1.3% yoy versus forecasts of 4.1% yoy. Imports from the U.S. dropped -16% yoy, reflecting both weaker domestic demand and the bite of tariffs. Still, the overall trade surplus widened from USD 98.2B to USD 102.3 B, beating expectations of USD 99.4B.

While the surplus provides headline support, the underlying dynamics are fragile. U.S. President Donald Trump has already threatened a 40% penalty tariff on goods deemed to be transshipped from China, raising questions about how long exporters can sustain the ASEAN workaround. Besides, economists warn that once U.S. tariffs rise above 35%, they become prohibitively high for many Chinese manufacturers.

Washington and Beijing extended their tariff truce by 90 days on August 11, locking in 30% U.S. duties on Chinese goods and 10% Chinese tariffs on U.S. exports. But with no path yet beyond the pause, uncertainty lingers over whether China can maintain export growth as tariff pressure intensifies.

SNB Schlegel: Hurdle to reintroducing negative rates remains high

SNB President Martin Schlegel said the bar for reintroducing negative rates remains “high,” acknowledging the policy’s “undesirable side effects” for savers and pension funds. His comments reinforced market expectations that the SNB will hold its policy rate steady well into 2026, with inflation staying positive for a third month in August.

Switzerland faces new headwinds from U.S. tariffs of 39%, which threaten its export-heavy economy and raise risks of further disinflation. Schlegel cautioned that while some firms will be hit hard, the overall economic impact is not yet clear. “Many companies are investing less, which is having a negative impact on the economy,” he told Migros-Magazin.

ECB to Lean Back; Fed Awaits US CPI

The ECB is widely expected to keep its deposit rate unchanged at 2.00% this week, marking its second consecutive hold. After cutting by 200bps between June 2024 and June 2025, markets are increasingly convinced the easing cycle is over. With inflation at target and unemployment still at record lows, policymakers see little urgency to move further.

This backdrop has been described as a soft landing: inflation near 2% and a labor market that remains resilient. In such an environment, the ECB can afford to step back, assess the impact of past cuts, and wait for clearer signs before shifting again. The balance of risks no longer tilts toward urgent easing, and consensus is building that rates could stay at current levels well into 2026.

Survey data backs up this outlook. A Reuters poll showed nearly 60% of economists expect the ECB to hold through 2025, while a narrow majority predict the deposit rate will still be at or above 2% by end-2026. For now, expectations of a long pause are keeping the euro broadly supported.

In contrast, the Fed faces mounting pressure to resume easing after two consecutive weak non-farm payrolls. Markets still lean toward a 25bps cut in September, but the risk of a 50bps move is rising as the Trump administration intensifies political pressure on the FOMC. Even if the Fed opts for caution this month, markets see a strong chance of back-to-back easing with another cut in October.

The week’s major focus in the U.S. will be on August CPI and PPI releases, which should reflect the early impact of tariff escalation. Consensus sees headline CPI rising from 2.7% to 2.9% yoy, while core CPI is expected to hold at 3.1% yoy. Any upside surprise would deepen the Fed’s dilemma: inflation edging higher while growth signals weaken.

For Fed hawks, a downside surprise in core CPI would provide the opening to pivot toward deeper or faster cuts. But expectations remain fluid, and market reaction is set to remain volatile. Dollar moves will likely mirror each CPI headline as traders recalibrate the odds of 25bps versus 50bps in September.

Beyond the Fed and ECB, investors will watch UK GDP for clues on fiscal drag, Eurozone investor confidence for signals on growth resilience, and sentiment data out of Australia, where the RBA has recently leaned less dovish. Together, these releases could set the tone for risk sentiment and FX positioning into mid-September.

Here are some highlights for the week:

- Monday: Japan GDP final; China trade balance; Germany industrial production, trade balance; Eurozone Sentix investor confidence.

- Tuesday: New Zealand manufacturing sales; Australia Westpac consumer sentiment, NAB business confidence; France industrial production.

- Wednesday: China CPI, PPI; US PPI.

- Thursday: Japan BIS manufacturing, PPI; ECB rate decision; US CPI, jobless claims.

- Friday: New Zealand BNZ manufacturing; Germany CPI final; UK GDP, trade balance; US UoM consumer sentiment and inflation expectations.

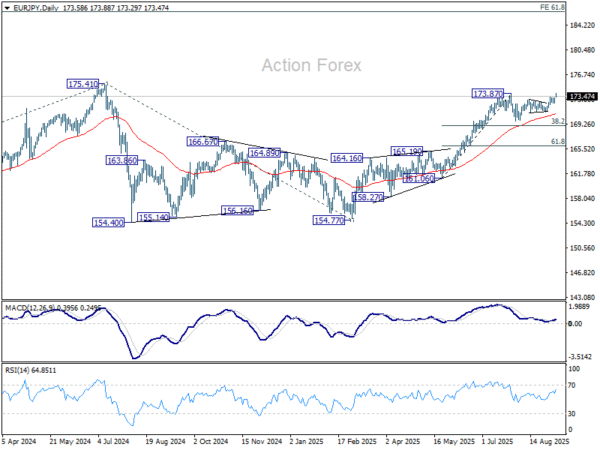

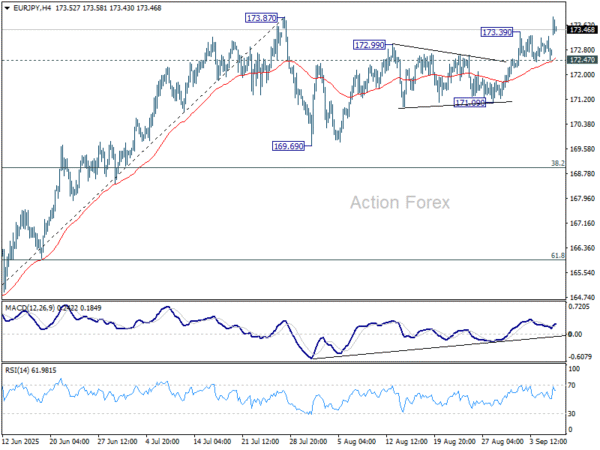

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.39; (P) 172.83; (R1) 173.17; More…

EUR/JPY’s rally resumed after brief consolidations and intraday bias is back on the upside. Firm break of 173.87 will resume larger rise to retest 175.41 key resistance. On the downside, though, break of 172.47 support will extend the corrective pattern from 173.87 with another falling leg, before rally resumption.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 38.2% retracement of 161.06 to 173.87 at 168.97 will delay this bullish case, and probably extend the correction from 175.41 with another fall.