Yen rebounded broadly today, climbing to the top of the performance leaderboard as traders latched onto speculation that the BoJ may still raise rates as soon as October. A Bloomberg report citing unnamed officials suggested some policymakers favor an earlier move, with reduced concern about growth risks following the U.S.–Japan trade deal. The report noted that the key variable for policymakers is whether the drag from U.S. tariffs on Japan’s economy remains within expectations. If so, the bank could argue there is room to resume normalizing rates despite political turbulence in Tokyo.

However, the report relied on anonymous sources and came alongside conflicting headlines. Many analysts argue the resignation of Prime Minister Shigeru Ishiba and the ensuing LDP leadership contest are reasons for caution. The BoJ, they contend, is unlikely to risk tightening policy amid such political uncertainty. The central bank also has time on its side. Policymakers can afford to wait until early next year for the next hike, ensuring stability while avoiding the impression of acting in haste. For markets, this means rate expectations are likely to remain volatile as headlines shift.

Elsewhere, Euro weakened broadly, with investors still digesting the ouster of French Prime Minister François Bayrou on Monday. His government’s collapse has heightened perceptions of instability in Paris, though the turmoil alone is unlikely to drive sustained Euro weakness without broader contagion. Still, the picture of France cycling through four prime ministers in two years have weighed on confidence. With President Emmanuel Macron scrambling to find another candidate capable of surviving parliament, Euro has remained defensive.

In the wider FX market, Yen is the day’s strongest performer so far, followed by Aussie and Kiwi. Euro is the weakest, trailed by the Swiss Franc and Loonie. Dollar and Sterling sit mid-pack.

In Europe, at the time of writing, FTSE is up 0.26%. DAX is down -0.48%. CAC is up 0.31%. UK 10-year yield is up 0.012 at 4.62. Germany 10-year yield is up 0.029 at 2.674. Earlier in Asia, Nikkei fell -0.42%. Hong Kong HSI rose 1.19%. China Shanghai SSE fell -0.51%. Singapore Strait Times fell -0.25%. Japan 10-year JGB yield fell -0.03 to 1.565.

Westpac: Australia consumer optimism elusive, RBA to pause in September

Australia’s Westpac Consumer Sentiment Index dropped -3.1% mom to 95.4 in September, reversing part of last month’s boost from the RBA’s third rate cut. While sentiment remains modestly above July levels and well above the April tariff-driven low, the index has slipped back into “cautiously pessimistic” territory. Westpac said outright optimism remains “elusive”, with households still uneasy about the path ahead despite relief from the cost-of-living crisis.

The RBA is expected to keep its cash rate steady at 3.6% when it meets later this month. Westpac noted recent data on inflation and demand came in “somewhat firmer than expected”, reinforcing the case for caution. Policymakers are seen waiting for further confirmation that underlying trends remain benign before resuming cuts.

For now, consumer recovery looks sluggish, and Westpac expects “further easing will likely be needed” to sustain momentum. It forecasts another 25bp cut in November and two additional moves in 2026, underscoring the gradual path ahead for both sentiment and policy.

Australia NAB business survey: Confidence falls, costs ease, capacity still tight

Australia’s NAB Business Confidence index slipped from 8 to 4 in August, but conditions showed improvement, rising from 5 to 7. Trading remained steady at 12, while profitability rose from 2 to 4 and employment from 2 to 5. NAB Chief Economist Sally Auld said the results support the view that “the outlook for businesses continues to improve,” with both confidence and conditions now near long-run averages.

Capacity utilisation rose to 83.1% from 82.5%, staying two percentage points above its long-run norm. Capital expenditure intentions also improved, climbing from 8 to 10. Together, these suggest firms are still operating at high levels of resource use despite broader uncertainties.

At the same time, cost pressures eased further. Purchase cost growth slowed from 1.3% to 1.1%, its lowest since 2021, while labour costs moderated to from 1.9% 1.5% and product price growth dipped to from 0.8% 0.6%. The survey points to an environment of resilient business activity and capacity tightness, but with inflation pressures continuing to recede.

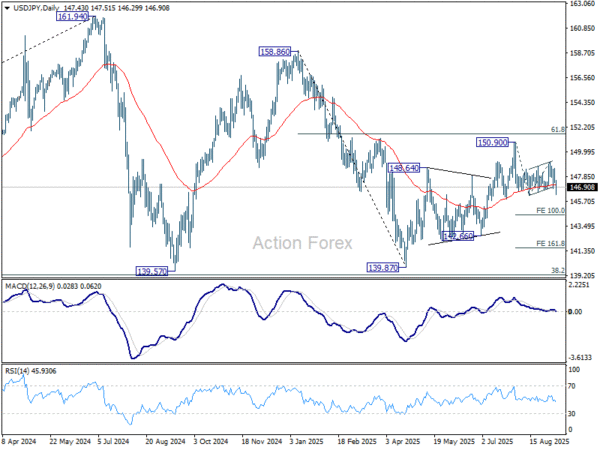

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.05; (P) 147.82; (R1) 148.29; More…

EUR/JPY’s break of 146.65 support suggest that fall from 150.90 is resuming. Intraday bias is back on the downside, and break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. On the upside, however, break of 147.51 minor resistance will mix up the outlook again and turn intraday bias neutral.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.