Global markets steadied on today as benchmark treasury yields dipped modestly after this week’s sharp jump. The pullback in yields helped ease pressure on risk sentiment, with European stocks trading slightly higher while U.S. futures hovered near flat.

Sterling also managed a tentative rebound following its steep selloff yesterday. Although investor concerns over the U.K.’s fiscal trajectory remain acute, the announcement of the Autumn Budget date has shifted attention to November for a clearer view on the government’s plans.

Chancellor Rachel Reeves confirmed she will deliver the Autumn Budget on November 26, reiterating that the government “must bring inflation and borrowing costs down by keeping a tight grip on day-to-day spending through our non-negotiable fiscal rule.” Reeves’ stance was seen as a bid to reassure markets about her commitment to discipline.

Still, Reeves will likely need to raise taxes to meet her targets and preserve a fiscal buffer of around GBP 10 billion. That margin has already been squeezed by U-turns on welfare cuts and the rising cost of borrowing, leaving limited room for maneuver as the government tries to restore confidence.

For now, markets appear willing to wait for Reeves’ budget for more concrete answers, though caution prevails. Any signs that Reeves could be sidelined would likely trigger renewed panic, as investors continue to view her credibility as critical for fiscal stability.

In the currency markets, Yen remains the weakest performer for the week, followed by Sterling and Kiwi. Dollar leads the pack, while Aussie and Euro are also firmer. Loonie and Swiss Franc are trading mid-range.

In Europe, at the time of writing, FTSE is up 0.39%. DAX is up 0.73%. CAC is up 0.91%. UK 10-year yield is down 0.027 at 4.782. Germany 10-year yield is down -0.022 at 2.769. Earlier in Asia, Nikkei fell -0.88%. Hong Kong HSI fell -0.60%. China Shanghai SSE fell -1.16%. Singapore Strait Times fell -0.21%. Japan 10-year JGB yield rose 0.031 to 1.637.

Eurozone PPI beats expectations at 0.4% mom on energy surge

Eurozone producer prices rose more than expected in July, with PPI up 0.4% mom and 0.2% yoy, compared with consensus of 0.2% mom and 0.1% yoy. The data suggest some renewed pipeline pressures, largely driven by energy. Across the wider EU, PPI increased 0.6% mom and 0.1% yoy. Overall, the figures indicate modest upward pressure in the production pipeline.

Within the Eurozone, energy costs jumped 1.5% from June, offsetting a -0.2% decline in intermediate goods. Prices for capital goods rose 0.1%, durable consumer goods gained 0.2%, while non-durable consumer goods were flat. The mix highlights that energy remains the key source of volatility in producer prices, even as other categories remain stable or subdued.

Price dynamics varied sharply across member states. The largest monthly increases were recorded in Romania (+6.7%), Bulgaria (+5.7%), and Slovakia (+2.8%), while Estonia (-1.0%), Latvia (-0.7%), and Luxembourg (-0.4%) posted declines.

Australia’s GDP rebounds 0.6% qoq in Q2, as spending and exports drive recovery

Australia’s economy grew 0.6% qoq in Q2, beating expectations of 0.5% qoq and expanding 1.8% yoy from a year earlier. The Australian Bureau of Statistics noted that growth rebounded after weather disruptions depressed activity in Q1. GDP per capita also rose 0.2% qoq, reversing the decline recorded in the March quarter.

Domestic final demand was the key driver, supported by a 0.9% qoq rise in household spending and a 1.0% qoq increase in government consumption. Public investment detracted from growth, but private demand proved resilient.

Net trade added 0.1 percentage points to GDP, driven by a rebound in exports of iron ore and LNG as production normalized after severe weather disruptions earlier in the year.

BoJ’s Ueda meets PM Ishiba, stresses stable FX and policy vigilance

BoJ Governor Kazuo Ueda said he discussed economic and market conditions, including foreign exchange moves, in a meeting with Prime Minister Shigeru Ishiba today. Ueda told reporters afterward that “it’s desirable for currency rates to move stably, reflecting fundamentals,” but declined to elaborate further on the details of the exchange.

On policy, Ueda reaffirmed that the BOJ remains prepared to raise interest rates further if the economy and prices evolve in line with projections. He emphasized that the central bank will “scrutinize without any pre-conception” whether those projections materialize.

China RatingDog services PMI rises to 53.0, optimism improves

China’s services sector gained fresh momentum in August, with the RatingDog PMI rising to 53.0 from 52.6, topping expectations of 52.5 and marking the highest level since May 2024. The composite index also improved, climbing to 51.9 from 50.8.

RatingDog founder Yao Yu highlighted that new business inflows surged to the highest since May of last year, while new export orders expanded at the fastest pace since February. More stable domestic demand and a recovery in foreign demand were key drivers, with service providers also reporting stronger optimism—the highest since March.

Price trends, however, remained challenging. Input costs rose modestly but firms were unable to fully pass them on, with output prices slipping back into contraction. That indicates profit margins have been under sustained pressure since late 2023.

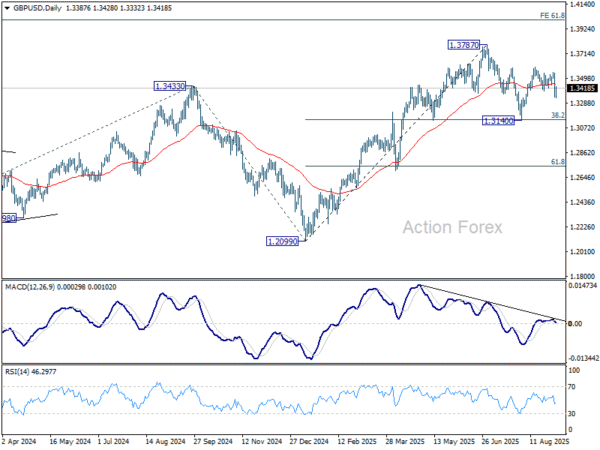

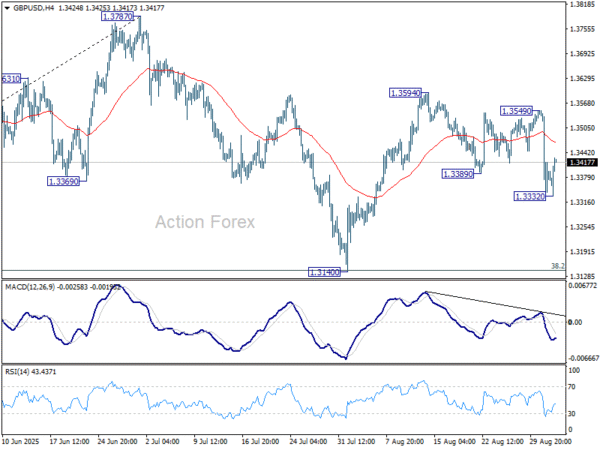

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3306; (P) 1.3428; (R1) 1.3515; More…

GBP/USD recovered after dipping to 1.3332 and intraday bias is turned neutral first. Overall outlook is unchanged that corrective pattern from 1.3787 is extending. Below 1.3332 will bring deeper pullback. But downside should be contained by 38.2% retracement of 1.2099 to 1.3787 at 1.3142. On the upside, break of 1.3549 resistance should resume the rebound from 1.3140 towards 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3104) holds, even in case of deep pullback.