Aussie and Kiwi are the top performers in FX trading on today so far, supported by the continued surge in Chinese equities. With the local market on course for its biggest monthly rise in nearly a year, risk sentiment spilled into regional currencies, giving both Australian and New Zealand Dollars some fresh momentum.

However, skepticism remains about the durability of the equity boom. The bulk of Chinese household wealth is tied up in property, which remains weak, suggesting that rising stock prices may not deliver much of a consumption boost. Still, for now, markets are embracing the positive sentiment, with the Aussie and Kiwi riding the tide.

Dollar has been more subdued, trading without a clear direction. Investors are holding back ahead of the July PCE release, the Fed’s preferred inflation gauge. Core PCE is expected to edge up to 2.9% yoy, while personal spending is forecast to grow 0.5% mom.

Spending may prove the bigger market mover. Any downside surprise in spending could point to early signs of consumer fatigue, even before August’s tariff escalations hit household budgets. That would bolster the case for the Fed to begin cutting rates in September, a path already widely anticipated.

Fed Governor Christopher Waller, one of the more dovish voices on the Board, urged that rates should eventually move back toward a neutral 3%. Still, he emphasized that the pace of cuts will depend on how data evolve.

In terms of weekly performance, Aussie tops the leaderboard this week, followed by Loonie and Kiwi. Euro is the weakest, trailed by Sterling and Swiss Franc, while Dollar and Yen sit in the middle of the field. That leaves the FX market neatly divided: commodity currencies strong, European currencies weak, and Dollar and Yen mixed.

In Asia, Nikkei fell -0.19%. Hong Kong HSI is up 0.94%. China Shanghai SSE is up 0.43%. Singapore Strait Times is up 0.39%. Japan 10-year JGB yield fell -0.007 to 1.612. Overnight, DOW rose 0.16%. S&P 500 rose 0.32%. NASDAQ rose 0.53% 10-year yield fell -0.031 to 4.207.

Fed’s Waller: Time to start cutting in September, target neutral around 3%

Fed Governor Christopher Waller said he would support a 25bps cut at the September 16–17 FOMC meeting, warning that waiting for further labor market deterioration would risk the Fed “falling behind the curve.” He said conditions warrant a move now to put policy on a path toward neutral.

He placed the neutral rate near 3%, around 125–150bps below current levels. While not convinced the Fed is behind the curve yet, he emphasized that signaling a path toward neutral is a way to reassure markets that the Fed won’t let policy remain too tight for too long.

Waller said he expects more easing over the next three to six months, “and the pace of rate cuts will be driven by the incoming data”. He left open whether that would mean “a sequence of cuts” or a more gradual adjustment with pauses. Either way, he made clear that policy should head steadily toward neutral. “It’s just a question how fast we get there,” he added.

The stance reflects his dissent at the July 30 meeting alongside Governor Michelle Bowman. Both argued then that signs of a softening labor market were enough reason to begin easing earlier.

Tokyo CPI core eases on to 2.5% yoy, but food inflation remains stubborn

Japan’s Tokyo CPI slowed in August as government fuel subsidies pushed down utility bills, but stubborn food inflation kept underlying price pressures elevated. Core CPI excluding fresh food eased to 2.5% yoy from 2.9% yoy, below expectations of 2.6% yoy. Headline CPI also cooled to 2.6% yoy, while the narrower core measure excluding both food and energy edged down to 3.0% yoy from 3.1% yoy.

Food inflation, however, remained sticky. Prices of rice, coffee beans and other groceries kept food CPI ex-fresh food at 7.4% yoy, unchanged from the previous month, highlighting persistent pressure on household budgets.

On the activity side, July industrial production dropped -1.6% mom, worse than forecasts of -1.0% mom, dragged down by a -6.7% mom slump in auto output. Manufacturers expect a rebound of 2.8% mom in August before a modest -0.3% mom dip in September.

Retail sales disappointed, rising only 0.3% yoy against expectations of 1.8% yoy. The labor market was a bright spot, with unemployment falling to from 2.5% to 2.3%, the lowest since December 2019.

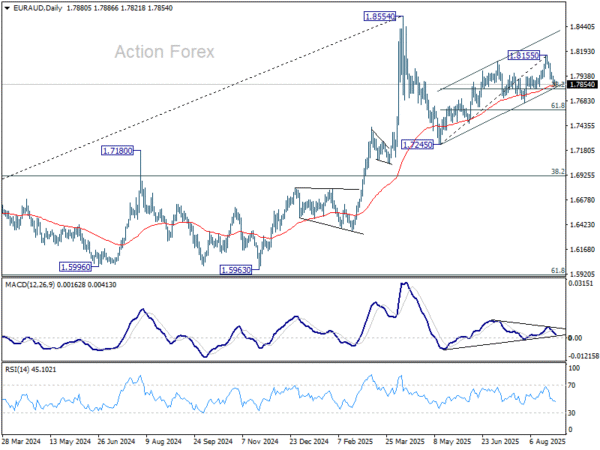

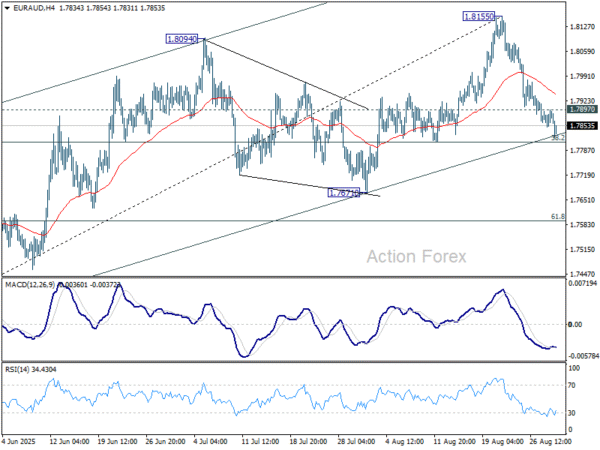

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7859; (P) 1.7879; (R1) 1.7906; More…

EUR/AUD’s decline from 1.8155 short term top continues today and intraday bias stays on the downside. Decisive break of 38.2% retracement of 1.7245 to 1.8155 at 1.7807 should confirm that whole rise from 1.7245 has completed. Corrective pattern from 1.8554 should then be in its third leg. Further decline should be seen to 61.8% retracement at 1.7593. On the upside, above 1.7897 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.