Canadian Dollar came under pressure in early U.S. session after GDP data revealed a deeper slowdown than markets had anticipated. Canada’s economy contracted -0.4% qoq in Q2, marking its first quarterly decline in seven quarters. More concerning was June’s monthly contraction, which signaled that the weakness might carry on into Q3.

The drag came primarily from exports, which tumbled under the weight of U.S. tariffs. With auto exports collapsing and machinery shipments down sharply, external headwinds are likely to remain a persistent strain on Canada’s economy in the months ahead.

The disappointing GDP print has shifted attention back to the BoC, where markets now see increased odds of a September rate cut. After holding for three straight meetings, the weak growth outlook could prompt policymakers to restart easing in an effort to cushion the economy.

In contrast, U.S. data releases offered few surprises. Core PCE inflation rose in line with forecasts while personal spending remained solid. The resilience in household demand suggests the U.S. economy retains some momentum, and it did little to alter expectations for Fed easing.

Markets still anticipate September as the starting point of the Fed’s new easing cycle, with two cuts expected in total this year. However, the next two weeks—featuring the August nonfarm payrolls and CPI reports—will be pivotal in determining how aggressive the Fed can be.

In weekly currency performance, Aussie remains the strongest, followed by Loonie and Kiwi. On the weaker side, Euro leads losses, trailed by Sterling and Yen, while Swiss Franc and Dollar sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.16%. DAX is down -0.14%. CAC is down -0.34%. UK 10-year yield is up 0.019 at 4.721. Germany 10-year yield is up 0.016 at 2.714. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI rose 0.32%. China Shanghai SSE rose 0.37%. Singapore Strait Times rose 0.37%. Japan 10-year JGB yield fell -0.013 to 1.605.

US Core PCE ticks higher to 2.9%, spending stays firm in July

U.S. headline inflation held steady in July, with the PCE price index unchanged at 2.6% yoy. Core measure ticked up to 2.9% from 2.8%, in line with forecasts. On a monthly basis, PCE rose 0.2% mom, and core prices increased 0.3% mom, pointing to modest but persistent price pressures.

Personal income rose 0.4% mom and spending climbed 0.5% mom, both as expected. The data suggest households remain resilient despite elevated borrowing costs, giving the Fed little urgency to accelerate easing.

Canada GDP contracts -04% qoq in Q2, tariffs hit exports hard

Canada’s economy shrank -0.4% qoq in Q2, as exports and business investment fell sharply. The downturn was led by a steep -7.5% drop qoq in exports, with machinery, travel services, and particularly autos hit hard by U.S.-imposed tariffs. Passenger car and light truck exports plunged -24.7% qoq.

Meanwhile, imports fell -1.3% in the quarter, reflecting Ottawa’s counter-tariff measures against the U.S. That helped cushion the trade balance slightly, though it also underscored the disruption in cross-border commerce.

Monthly GDP data painted an equally weak picture, with output slipping -0.1% mom in June versus expectations for modest growth of 0.1% mom.

ECB consumer survey shows long-term inflation anchored, growth views weaken

The ECB’s July Consumer Expectations Survey showed households continue to see inflation remaining above target in the near term, with 12-month expectations steady at 2.6% and three-year expectations edging higher to 2.5% from 2.4%. Five-year inflation expectations were unchanged at 2.1% for an eighth consecutive month, underscoring anchored long-term views.

Notably, uncertainty around one-year inflation stayed at its lowest since January 2022, with the median at 1.6%. This suggests households feel more confident about the inflation outlook, even as near-term expectations remain somewhat elevated.

Growth and labor market expectations turned more downbeat. Economic growth was expected to contract by -1.2% over the next 12 months, compared with -1.0% in June. Unemployment expectations rose to 10.6% from 10.3%. The results highlight continued pessimism about the Eurozone’s economic prospects despite inflation stability.

Tokyo CPI core eases on to 2.5% yoy, but food inflation remains stubborn

Japan’s Tokyo CPI slowed in August as government fuel subsidies pushed down utility bills, but stubborn food inflation kept underlying price pressures elevated. Core CPI excluding fresh food eased to 2.5% yoy from 2.9% yoy, below expectations of 2.6% yoy. Headline CPI also cooled to 2.6% yoy, while the narrower core measure excluding both food and energy edged down to 3.0% yoy from 3.1% yoy.

Food inflation, however, remained sticky. Prices of rice, coffee beans and other groceries kept food CPI ex-fresh food at 7.4% yoy, unchanged from the previous month, highlighting persistent pressure on household budgets.

On the activity side, July industrial production dropped -1.6% mom, worse than forecasts of -1.0% mom, dragged down by a -6.7% mom slump in auto output. Manufacturers expect a rebound of 2.8% mom in August before a modest -0.3% mom dip in September.

Retail sales disappointed, rising only 0.3% yoy against expectations of 1.8% yoy. The labor market was a bright spot, with unemployment falling to from 2.5% to 2.3%, the lowest since December 2019.

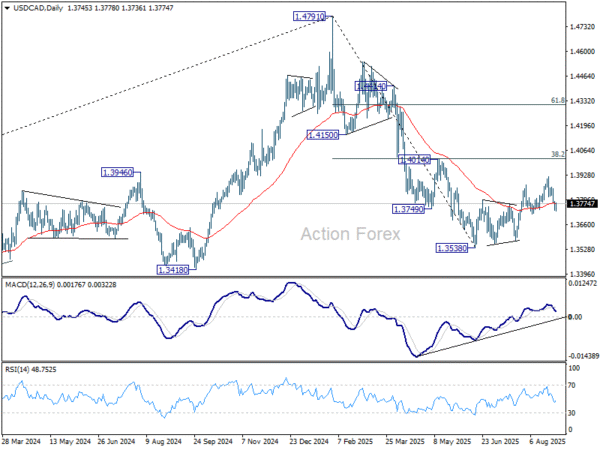

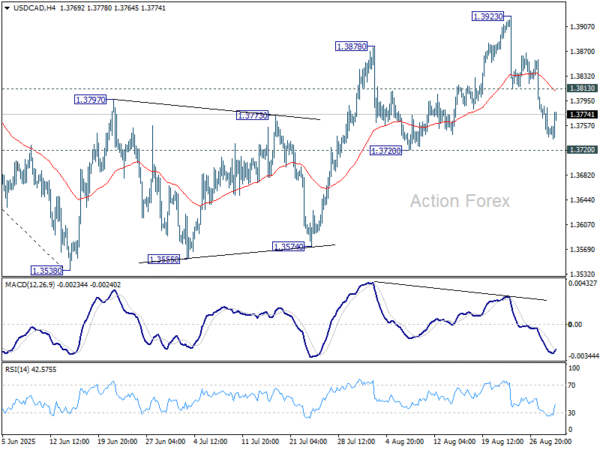

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3761; (R1) 1.3782; More…

Intraday bias in USD/CAD stays neutral first despite current recovery. On the upside, firm break of 1.3813 will indicate that the pullback from 1.3923 has completed, and corrective rise from 1.3538 is still in progress. Retest of 1.3923 should be seen next. But upside should be limited by 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Meanwhile, firm break of 1.3720 will argue that the corrective bounce has already completed, and bring retest of 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.