Dollar is charging broadly higher as traders turn their focus to Fed Chair Jerome Powell’s upcoming remarks at the Jackson Hole Symposium later today. Scheduled for 1400GMT, the speech is seen as the key event of the week, particularly after recent data and Fed commentary trimmed expectations for near-term easing.

Markets have scaled back bets on a September rate cut, with odds dropping from over 90% last week to about 73% currently. Comments from Fed officials have struck a distinctly cautious tone, with most sounding dismissive of the need for an imminent cut. Notably, Boston Fed President Susan Collins has expressed openness to action but stopped short of pushing for it, leaving the dovish camp conspicuously thin.

This contrasts with prior market optimism that a dovish pivot was imminent. Instead, the lack of strong voices pushing for a September move highlights how the Fed remains unconvinced that conditions justify immediate action. Recent speeches suggest some policymakers are far more focused on inflation risks than on rushing to loosen policy.

The latest US PMI flash readings reinforced that stance. Manufacturing activity staged a sharp rebound in August while services growth held firm, putting the composite PMI at its highest in eight months. S&P Global estimates that the data aligns with a 2.5% annualized GDP growth rate, almost double the average pace from the first half of the year.

Importantly, the surveys showed inflationary pressures building again. Companies reported greater ability to pass tariff-related cost increases through to customers, with the price index reaching a three-year high. S&P Global argued that such conditions historically align more with a case for tightening, not easing.

Powell is unlikely to use today’s platform to signal any sudden shift. Known more for his moderate, consensus-driven tone than for taking a strong lead, he may simply emphasize Fed’s dual mandate while acknowledging both the risks of sticky inflation and signs of cooling in the labor market. Still, even subtle hints about which side of the mandate is taking precedence could meaningfully sway rate pricing.

In currency markets, Dollar leads the way as at this point of the week, followed by Swiss Franc and Loonie. At the other end, Kiwi remains pinned at the bottom, trailed by Aussie and Sterling. Euro and Yen are holding a middle ground.

In Asia, at the time of writing, Nikkei is down -0.13%. Hong Kong HSI is up 0.39%. China Shanghai SSE is up 0.84%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is up 0.005 at 1.616. Overnight DOW fell -0.34%. S&P 500 fell -0.40%. NASDAQ fell -0.34%. 10-year yield rose 0.034 to 4.330.

Fed’s Hammack: No case for rate cuts as inflation trends wrong way

Cleveland Fed President Beth Hammack signaled little appetite for near-term easing, telling Yahoo Finance that if the FOMC were meeting tomorrow she “would not see a case for reducing interest rates.” She stressed that inflation has been “too high for the past four years” and it’s been “trending in the wrong direction” currently, justifying a stance that remains “modestly restrictive.”

Hammack noted that the economy has so far shown resilience, with no significant signs of downturn that would warrant easier policy. Instead, she emphasized the Fed’s responsibility to ensure inflation expectations remain anchored, cautioning that premature cuts risk undermining that effort.

On tariffs, Hammack flagged that their effects are only beginning to filter through. Typically, it takes “three to four months” for the first signs to emerge, meaning the bulk of the impact will not be seen until 2026. She expects further pass-through of higher costs next year, adding another reason to proceed cautiously on easing.

Fed’s Goolsbee cautious on cuts, Collins open to September easing

Chicago Fed President Austan Goolsbee struck a cautious tone, telling Bloomberg TV that while next month’s FOMC meeting is “live,” the recent pickup in services inflation has made him hesitant about supporting a rate cut.

He pointed to the latest CPI report, where services costs accelerated in a way “probably not driven by tariffs,” calling it a “dangerous data point” for Fed’s inflation fight.

In contrast, Boston Fed President Susan Collins signaled a greater willingness to cut rates soon, telling the Wall Street Journal she could back easing as early as September. Collins emphasized that higher tariffs could weigh on consumer purchasing power and ultimately weaken spending, while also warning that labor market risks are becoming more visible.

Collins acknowledged that she expects inflation to keep rising through the end of 2025 before easing again in 2026, but still viewed the risks to growth and employment as important factors that justify keeping the option of cuts on the table.

Japan core CPI slows to 3.1% as rice inflation cools, but underying pressures persist

Japan’s inflation slowed again in July, with core CPI (ex-fresh food) easing to 3.1% yoy from 3.3% yoy, slightly above expectations of 3.0% yoy. Headline CPI also dipped to 3.1% yoy. The moderation was driven in part by cooling rice prices, which rose 90.7% yoy after surging 100.2% yoy in June, alongside the reintroduction of energy subsidies. Together, these helped bring core inflation down from May’s 3.7% peak.

However, price pressures remain entrenched. Food inflation excluding fresh items actually quickened to 8.3% yoy from 8.2% yoy. Core-core CPI (ex-food and energy) stayed unchanged, elevated at 3.4%. Energy prices provided some relief with a -0.3% yoy annual decline, the first drop since March 2024, but this was not enough to counter stubborn underlying strength.

For policymakers at BoJ, the data paints a mixed picture: rice and energy are finally easing their grip on consumer prices, but persistently high core inflation highlights why interest rate hikes remain on the table. While inflation is clearly off its May peak, the road back toward the 2% target looks slow and uneven.

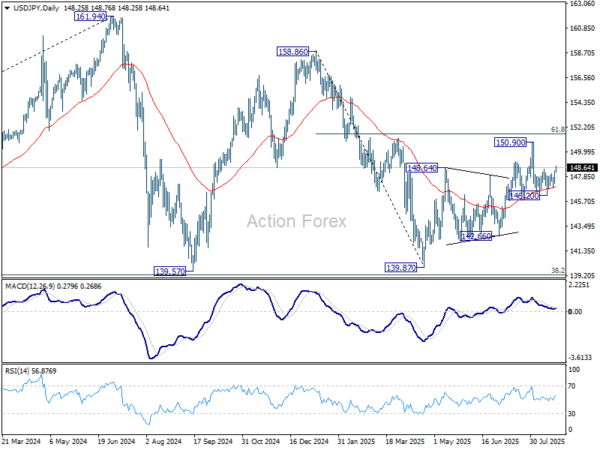

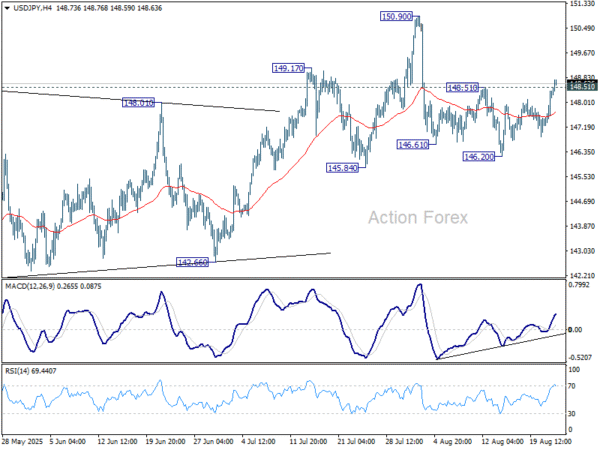

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.62; (P) 148.01; (R1) 148.78; More…

USD/JPY’s break of 148.51 resistance suggests that correction from 150.90 has already completed at 146.20. Larger rebound from 139.87 should still be in progress. Intraday bias is back on the upside for 150.90 first. Firm break there will target 151.22 fibonacci level next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.