Dollar is holding broadly firm as markets head into the US session, though intraday momentum has slowed. Traders are reluctant to commit to new positions ahead of Fed Chair Jerome Powell’s highly anticipated Jackson Hole speech.

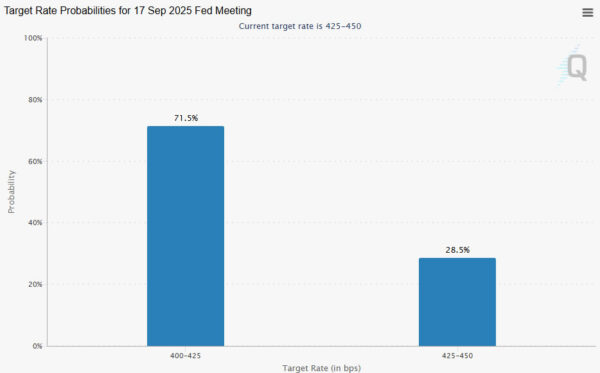

Expectations for a September rate cut have already been pared back sharply, with Fed fund futures now pricing around a 71% chance, down from over 90% just a week ago. Powell’s remarks will be closely scrutinized for any hint on whether he sees scope for a near-term move, or whether inflation risks still outweigh concerns about labor market cooling.

Market participants are also mindful that Powell’s tone will not be the only driver today. Comments from other Fed officials are expected to hit the wires, helping investors gauge the balance of views across the committee. By the end of the day, markets should have a clearer sense of the prevailing hawkish or dovish leanings inside the Fed.

Still, it must be stressed that today’s speeches are not the final word. Both the August nonfarm payrolls and CPI reports will be released before the next FOMC meeting, and those could easily shift expectations again. Market pricing will therefore remain highly data-dependent over the coming weeks.

For now, the Dollar sits as the strongest performer of the week, trailed by Swiss Franc and Loonie. Kiwi remains the weakest, followed by Aussie and Sterling, while Euro and Yen are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is down -0.03%. CAC is up 0.11%. UK 10-year yield is up 0.007 at 4.74. Germany 10-year yield is down -0.013 at 2.746. Earlier in Asia, Nikkei rose 0.05%. Hong Kong HSI rose 0.93%. China Shanghai SSE rose 1.45%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield rose 0.008 to 1.619.

Canadian retail sales jump in 1.5% mom June, but July seen weakening

Canada’s retail sales climbed 1.5% mom to CAD 70.2B in June, though the gain fell just short of expectations of 1.6% mom. The increase was broad-based, with all nine subsectors contributing, led by food and beverage retailers.

Excluding autos, sales rose an even stronger 1.9% mom, more than doubling forecasts of 0.9% mom, suggesting underlying consumer spending remains resilient.

In volume terms, retail sales advanced 1.5% mom in June, reinforcing that the pick-up was not purely price-driven. On a quarterly basis, sales grew 0.4% qoq, with volumes up 0.7% qoq, pointing to a modest but positive contribution from consumption to Q2 GDP.

However, early signals from Statistics Canada suggest the momentum could be fading. The agency’s advance estimate shows sales likely slipped -0.8% in July mom, raising the risk that strong second-quarter consumption may not carry through into the third.

Eurozone wages growth jump to 3.95%, supports ECB pause

Eurozone negotiated wages accelerated to 3.95% in Q2, up sharply from 2.46% in Q1, the ECB reported on Friday. Though well below the 2024 peak of 5.4%, the acceleration suggests cost pressures remain sticky.

Some analysts noted that much of the gain reflected one-off payments, raising the possibility that the rise is short-lived. Still, with services inflation remaining elevated, policymakers have little scope to accelerate easing after already cutting the deposit rate to 2.00%.

Whether wage growth cools in the coming quarters will be central to determining if the ECB can continue on its path toward looser policy.

Japan core CPI slows to 3.1% as rice inflation cools, but underlying pressures persist

Japan’s inflation slowed again in July, with core CPI (ex-fresh food) easing to 3.1% yoy from 3.3% yoy, slightly above expectations of 3.0% yoy. Headline CPI also dipped to 3.1% yoy. The moderation was driven in part by cooling rice prices, which rose 90.7% yoy after surging 100.2% yoy in June, alongside the reintroduction of energy subsidies. Together, these helped bring core inflation down from May’s 3.7% peak.

However, price pressures remain entrenched. Food inflation excluding fresh items actually quickened to 8.3% yoy from 8.2% yoy. Core-core CPI (ex-food and energy) stayed unchanged, elevated at 3.4%. Energy prices provided some relief with a -0.3% yoy annual decline, the first drop since March 2024, but this was not enough to counter stubborn underlying strength.

For policymakers at BoJ, the data paints a mixed picture: rice and energy are finally easing their grip on consumer prices, but persistently high core inflation highlights why interest rate hikes remain on the table. While inflation is clearly off its May peak, the road back toward the 2% target looks slow and uneven.

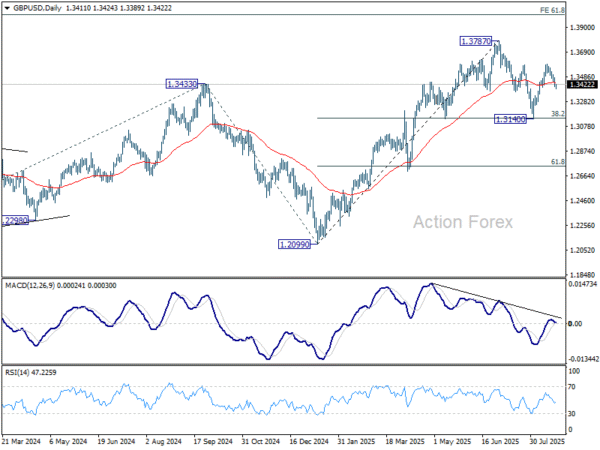

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3384; (P) 1.3434; (R1) 1.3462; More…

Intraday bias in GBP/USD remains mildly on the downside for the moment. Fall from 1.3594 is in progress for 61.8% retracement of 1.3140 to 1.3594 at 1.3313. Firm break there will bring retest of 1.3140 low. On the upside, above 1.3481 minor resistance will bring retest of 1.3594 first. Overall, corrective pattern from 1.3787 is extending.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3090) holds, even in case of deep pullback.