Canadian Dollar edged lower in early US trading Friday following a mixed labor market report that offered little clarity on the BoC’s next move. The set of data suggests that slack is building, but not yet enough to trigger a policy response.

BoC left its benchmark rate unchanged at 2.75% last week for the third straight meeting, stating that a cut could be warranted if economic weakness deepens and inflationary pressures from global trade disruptions remain contained. Today’s report will add weight to those arguments, but with no surge in unemployment and wage pressures still evident, the central bank is expected to stay cautious.

Markets may start pricing in a higher probability of a rate cut in Q4, but an immediate policy shift remains unlikely. Loonie traders appear to be taking the data in stride, with USD/CAD holding within tight range, reflecting a wait-and-see stance.

Broader market moves were subdued heading into the weekend. Yen came under fresh pressure and is now the second worst performer on the week, trailing only Swiss Franc. Dollar is slightly firmer today but remains the third weakest major, still digesting recent dovish shifts in Fed expectations.

On the stronger side, Sterling continues to outperform, buoyed by the Bank of England’s hawkish rate cut this week. Aussie and Kiwi also remain firm. Euro and Loonie are trading in the middle of the pack, showing no strong directional bias.

Meanwhile, tensions between India and the US are escalating. In a rare public signal of protest, New Delhi has reportedly frozen plans to purchase US weapons and aircraft following US President Donald Trump’s decision to hike tariffs on Indian exports to 50%. A planned visit by Indian Defence Minister Rajnath Singh to Washington has also been scrapped according to media reports.

Canada’s jobs shrink -40.8k in July, wages growth pick up

Canada’s labor market surprised to the downside in July, shedding -40.8k jobs versus expectations of a 15.3k gain. The drop was led by a sharp decline in full-time employment (-51k), and offsetting some of June’s strong 83k rise. Overall job growth has stagnated, with employment up just 27k since January. However, the unemployment rate held steady at 6.9%, slightly better than the expected 7.0%.

Despite the headline job loss, average hourly wages rose 3.3% yoy in July, slightly up from June’s 3.2% yoy. Total hours worked dipped marginally by -0.2% mom, indicating flat momentum in overall labor output. The mixed signals—a steep fall in full-time jobs alongside rising wages—paint a complex picture for policymakers.

BoE’s Pill questions cut pace, says inflation risks may delay easing

BoE Chief Economist Huw Pill signaled that the central bank may need to reconsider its steady pace of easing if shifts in longer-term inflation dynamics persist. In a briefing to business leaders, Pill acknowledged that inflation pressures are likely to keep easing, but warned that price- and wage-setting behavior” may delay further policy easing.

“That might lead us to… question whether the pace at which we’re reducing Bank Rate… is sustainable,” he said, referencing the quarterly 25bps cut rhythm the BoE has maintained over the past year.

Pill’s comments help clarify the reasoning behind Thursday’s unexpectedly tight 5–4 policy vote, where he and three other members dissented against the 25bps cut to 4.00%. The majority, including Governor Andrew Bailey, favored continuing the easing path. But the split exposed growing concern within the Monetary Policy Committee over stickier inflation risks. Pill said the more hawkish voters are focused on upside risks driven by behavioral shifts rather than headline inflation itself.

Traders are now pushing back expectations for the next cut, with futures no longer fully pricing a 25bps move before February. Pill’s remarks reinforce the message that while policy is still on a downward path, the pace may slow if inflation proves more persistent beneath the surface.

BoJ Opinions: 2–3 months needed to Gauge Tariff impacts, year-end hike possible

BoJ’s July 30–31 Summary of Opinions revealed a broadly cautious stance on future policy moves, with members emphasizing the need for more data before shifting course.

Despite the recent US–Japan tariff agreement, board members reaffirmed that Japan’s baseline outlook has not improved. “Japan’s economic growth will moderate and the improvement in underlying CPI inflation will be sluggish temporarily,” one policymaker said. Accordingly, the consensus was to maintain current interest rates and financial accommodation, while monitoring trade risks and external demand.

“At least two to three more months are needed to assess the impact of US tariff policy,” one member stated, noting that the direction of US monetary policy and exchange rates could also shift materially depending on inflation and labor conditions.

Still, the door is now open for rate hikes later this year. The Summary suggests that if incoming data shows resilience in the US economy—and Japan avoids major trade fallout—the BoJ could resume policy normalization as soon as year-end.

“It may be possible for the Bank to exit from its current wait-and-see stance, perhaps as early as the end of this year,” one policymaker said. That prospect keeps the door open to further hikes in late 2025 if inflation and growth align.

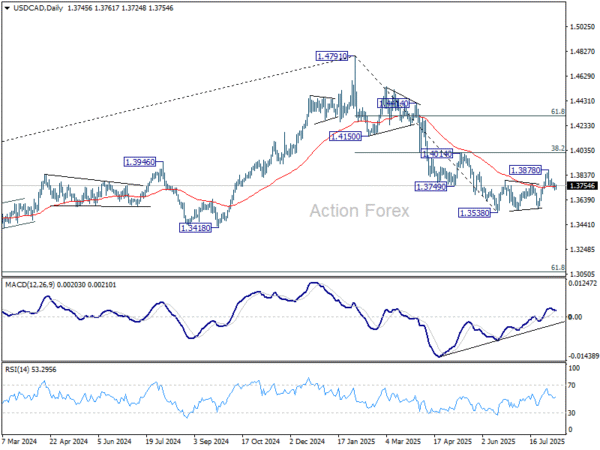

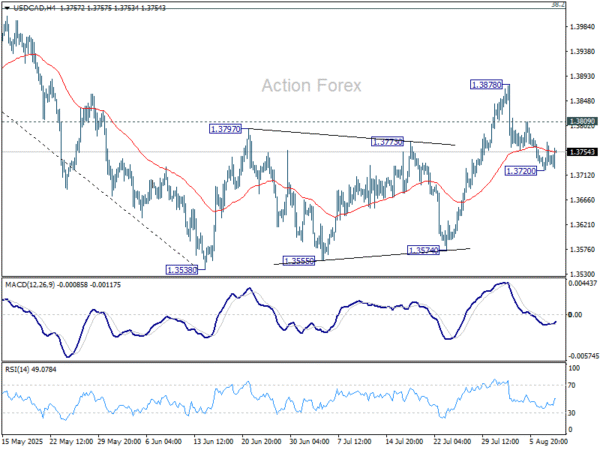

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3723; (P) 1.3748; (R1) 1.3775; More…

Intraday bias in USD/CAD is turned neutral first with 4H MACD crossed above signal line. On the downside, below 1.3720 will affirm the case that corrective rebound from 1.3538 has completed at 1.3878. Deeper fall should then be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view, and turn bias back to the upside for retesting 1.3878 instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.