Asian equity markets are broadly stable today, shrugging off the negative lead from Wall Street overnight. The broader resilience comes despite a sharp selloff in chip stocks across Japan, South Korea, and Taiwan after US President Donald Trump confirmed that new tariffs on semiconductors and chips will be unveiled “within the next week or so.”

The planned sector-specific tariffs mark a new phase in the trade war. While reciprocal country-level tariffs appear largely set following last week’s sweeping executive orders, the White House is now pivoting toward targeted sectoral action. Alongside semiconductors, Trump flagged the pharmaceutical industry as another category under review — with some levies potentially rising as high as 250%, the steepest threat to date.

So far, broader Asian indices are holding up, with investors cautiously awaiting further clarity. However, sentiment remains fragile as the risk of further escalation persists. With markets still digesting the implications of a prolonged tariff campaign, sector-specific vulnerabilities are starting to come into sharper focus, especially in export-driven economies.

In the currency markets, price action remains subdued. All major currency pairs and crosses are still trading within last week’s ranges, reflecting underlying indecision. Dollar is on the softer side today, but there was no following through selling after yesterday’s disappointing ISM Services print. Loonie and Swiss Franc are also underperforming in today’s session.

Kiwi is showing a modest rebound after Q2 employment data showed a smaller-than-expected rise in unemployment. Still, the report does little to shift expectations for another RBNZ rate cut later this month. Aussie is also slightly firmer, helped by a record high in the ASX equity index. Meanwhile, Euro, Sterling, and Yen are all trading mixed in the middle.

In Asia, at the time of writing, Nikkei is up 0.55%. Hong Kong HSI is down -0.01%. China’s Shanghai SSE is up 0.18%. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield is up 0.017 at 1.493. Overnight, DOW fell -0.13%. S&P 500 fell -0.49%. NASDAQ fell -0.65%. 10-year yield fell -0.004 to 4.196.

Japan real wages remain negative despite stronger 2.5% nominal growth

Japan’s real wages continued to contract in June, falling -1.3% yoy — the sixth straight month of decline. While that marked an improvement from May’s revised -2.6% yoy drop, persistent inflation, particularly in food prices, continues to erode household purchasing power. Consumer prices used for wage calculations rose 3.8% yoy in June, far outpacing nominal wage gains.

Nominal wages climbed 2.5% yoy, up from 1.4% yoy in May and rising for the 42nd consecutive month. However, the reading missed expectations of 3.2% yoy, tempering the positive headline. Base pay rose 2.1% yoy, and special earnings — mainly bonuses — grew 3.0% yoy, supporting a modest rise in overall pay levels during the reporting month.

NZ unemployment rate rises to 5.2%, RBNZ August cut in play

New Zealand’s Q2 labour market report confirmed continued softening, with employment falling -0.1% qoq and unemployment edging up to 5.2%. That marks the highest jobless rate since 2020, though still slightly below consensus of 5.3%. Participation rate also dropped -0.2 points to 70.5%, its lowest since early 2021, suggesting a cooling in demand.

Wage growth offered a mixed signal to the RBNZ. The private sector wage index rose 0.6% qoq, higher than expected 0.5% qoq and up from Q1’s 0.4%. But annual wage inflation slowed from 2.5% to 2.2% — the lowest in over three years — hinting that longer-term wage pressures are easing.

The overall report doesn’t deviate much from RBNZ’s May projections and is unlikely to alter its near-term stance. With inflation running at 2.7% yoy in Q2, markets still expect one more 25bps rate cut from the current 3.25% this month. But the central bank is likely to stay cautious on signaling further easing until price and wage dynamics show more decisive downside momentum.

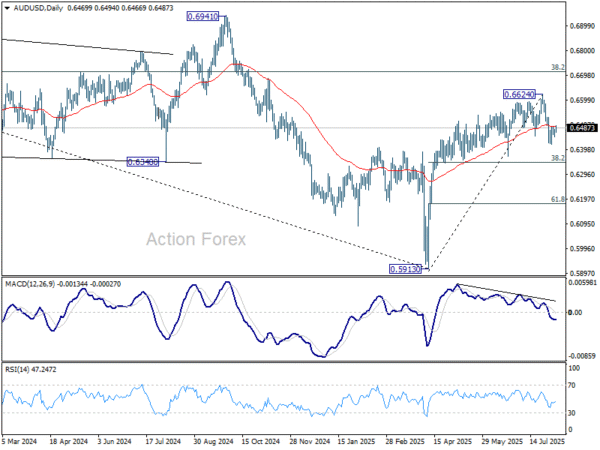

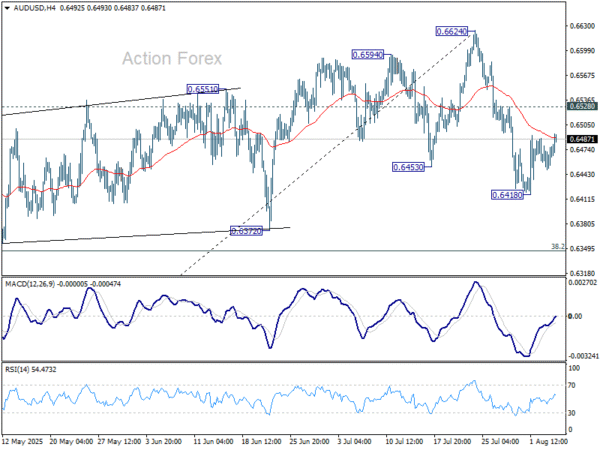

AUD/USD Daily Report

Daily Pivots: (S1) 0.6455; (P) 0.6467; (R1) 0.6485; More…

AUD/USD’s recovery from 0.6418 extends higher today but stays below 0.6528 resistance. Intraday bias remains neutral and further decline is in favor. Fall from 0.6624 short term top is seen as at least correcting the rally from 0.5913. Below 0.6418 will target 38.2% retracement of 0.5913 to 0.6624 at 0.6352. Nevertheless, break of 0.6528 will dampen this bearish case, and bring retest of 0.6624 high instead.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).