Summary

- The FOMC left the federal funds rate unchanged for the fifth consecutive meeting. The post-meeting policy statement had minimal changes and continued to characterize inflation as “somewhat elevated,” the unemployment rate as “low” and labor market conditions as “solid.” The pace of balance sheet runoff, also known as quantitative tightening, was left unchanged.

- Governors Waller and Bowman dissented against the decision to hold rates steady, preferring instead to cut the fed funds rate by 25 bps. This marked the first time multiple governors formally dissented since December 1993.

- To some extent these dissents reflect political jockeying, as Jerome Powell’s term as Chair comes to an end next spring. But, we suspect the dissents reflect at least some genuine disagreement among Committee participants as they grapple with the appropriate stance of monetary policy amid the stagflationary impulse from higher tariffs.

- In the post-meeting press conference, Chair Powell was very careful to play his cards close to the chest regarding the outlook for a rate cut at the September meeting. Chair Powell cited easing financial conditions, a low unemployment rate and still-above target inflation as reasons to keep rates on hold. But, he highlighted potential downside risks to the labor market as a key reason to remain nimble when thinking about the path forward for the fed funds rate.

- Economic and policy developments between now and the next FOMC meeting on September 16-17 will be critical to determining the path forward for monetary policy. The FOMC will receive two more employment reports (including Friday’s jobs data) and two more months of inflation data between now and then. Furthermore, although we doubt full clarity on tariffs is coming anytime soon, we should know more about the administration’s tariff intentions and the economy-wide average effective tariff rate come mid-September.

- As we go to print, markets are pricing roughly a 49% chance of a 25 bps rate cut at the September FOMC meeting. Our current forecast looks for the FOMC to cut the fed funds rate by 25 bps at its September, October and December meetings, with risks skewed toward pushing back the timing of those cuts. We intend to adjust our fed funds forecast, if necessary, after the dust has settled following Friday’s employment report.

The Center Holds

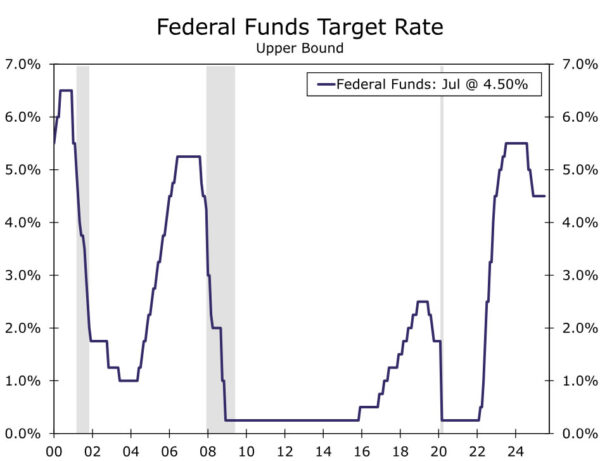

As was widely expected, the FOMC left the fed funds target range unchanged at the conclusion of its meeting today (Figure 1). The Committee has held the policy rate steady at 4.25%-4.50% this year as the economy’s resilience has afforded the FOMC time to see how inflation and the labor market fare in the face of higher tariffs. However, Committee members are no longer all on board with this wait-and-see approach. Governors Waller and Bowman dissented in favor of reducing the fed funds rate by 25 bps at today’s meeting.

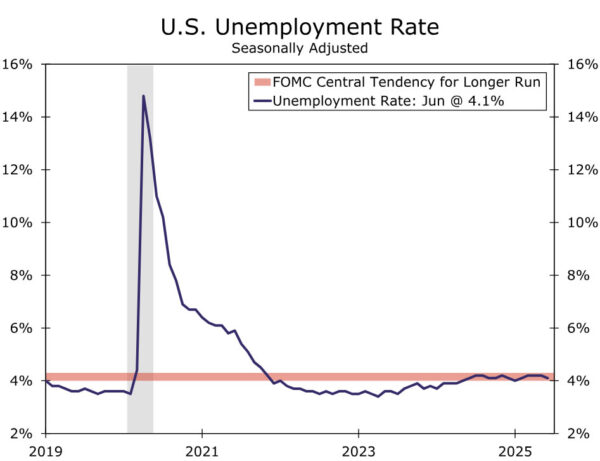

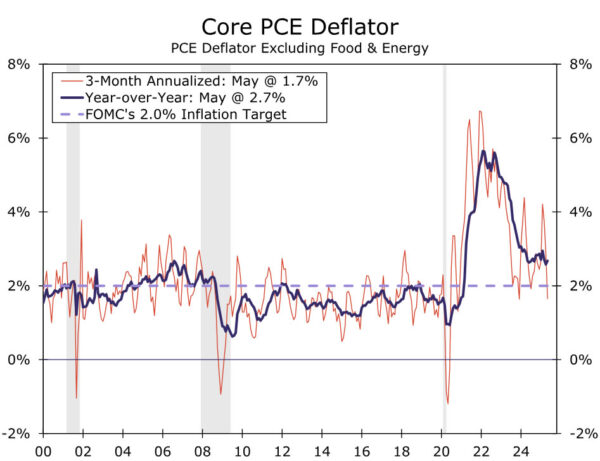

Yet, there were no hints in the statement that other Committee members may soon be ready to follow their lead. The majority of voters still see policy as appropriately positioned to support the Committee’s inflation and employment objectives. The statement continued to characterize inflation as “somewhat elevated,” as the core PCE deflator has been running above the FOMC’s 2% target for four years and counting (Figure 2). At the same time, labor market conditions remain “solid.” The Committee did note some loss of momentum in economic growth recently, which was evident in the details of second quarter GDP. That said, the statement does not seem overly worried about current activity, noting it has moderated, rather than expanded at a “solid” pace recently. The only other change to the statement was the removal of uncertainty as “having diminished;” it now simply states that uncertainty remains elevated.

The dissents of Governors Waller and Bowman were telegraphed ahead of today’s meeting and thus do not come as a surprising development. As the only two governors appointed by President Trump, the breaking of ranks could be viewed as jockeying for position in the race for the next Fed chair given that the administration has made no secret in its preference for lower rates. After all, a double dissent by governors has become extraordinarily rare, with the last one occurring in 1993.

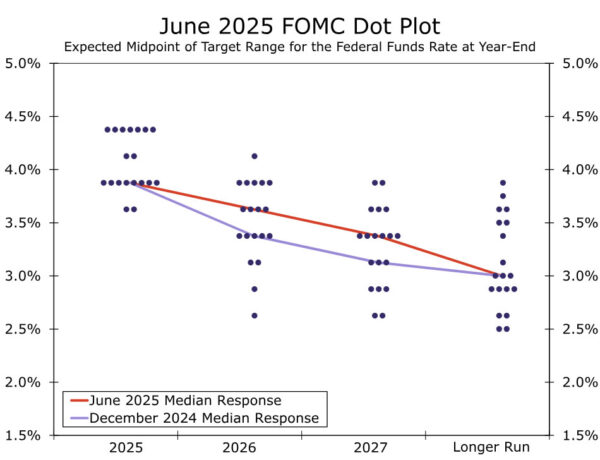

That said, dissents are not uncommon around policy turning points. A directional bias among Committee members to lower rates has been in place since the last rate reduction in December, even as there remains disagreement over the precise timing and magnitude (Figure 3). The more formal, vocal support by Waller and Bowman could slightly hasten the timing to which the Committee decides to next move rates lower, especially as Governor Waller has served as a bellwether for the Committee the past few years.

Committee members will not have to wait long for the picture to be filled in. Friday will bring the July employment report. Last year’s July job report also was released just days after the FOMC’s meeting, and it showed more pronounced softness in the labor market that started the FOMC down the path of eventually cutting the fed funds rate by 50 bps at its subsequent meeting in September. While Friday’s jobs report will not be the only major data release before the FOMC’s next meeting on September 17 (there will be one additional employment report and two more months of inflation data), we view a weaker employment report as a necessary condition for the FOMC to cut rates as soon as its next gathering (Figure 4). Our current forecast looks for the FOMC to cut the fed funds rate by 25 bps at its September, October and December meetings, with risks skewed toward pushing back the timing of those cuts. We intend to adjust our fed funds forecast, if necessary, after the dust has settled following Friday’s employment report.