A wave of optimism rippled through global markets Wednesday after the U.S. and Japan finalized a trade agreement slashing tariffs and easing trade tensions. The Nikkei jumped 3.51%, setting the tone across Asia, while European stocks and US futures are also trading higher. Hopes are growing that other trade partners, notably the EU, may also secure deals before the looming August tariff deadlines.

In currencies, risk-sensitive Kiwi and Aussie led gains, followed by Yen — itself a reflection of Japan’s improving trade outlook. On the other end, Euro, Swiss Franc, and Dollar lagged, consistent with an unwinding of safe-haven positions. Sterling and Loonie are positioning in the middle .

The core of the Japan deal includes a reduction of US tariffs on autos from 27.5% to 15%, and other goods from 25% to 15%. While still high, these levels are considered manageable and far better than the maximum threat levels. Investors are encouraged by the return of predictability, which had been absent during months of escalating trade rhetoric.

Yet, the threat of elevated tariffs still looms large. Canada faces potential 35% duties, and the EU could be hit with 30% unless a deal is reached. China remains under pressure as well, with the August 12 expiration of the 90-day truce fast approaching. If no resolution is found, tariffs could revert to a punishing 145% on U.S. goods and 125% on Chinese exports.

Despite these risks, traders are betting on progress. US Treasury Secretary Scott Bessent said talks with the EU are “going better than they had been”. But he emphasized that Japan’s favorable 15% rate was linked to a creative package involving equity stakes, credit guarantees, and investment pledges. EU negotiators will need to match that innovation to reach a similar outcome.

The European Commission, for its part, is continuing parallel preparations for retaliation. Trade Commissioner Maros Sefcovic is scheduled to speak with Commerce Secretary Howard Lutnick later today. Brussels will consolidate two proposed tariff lists worth EUR 93B into a single countermeasure plan for member approval. These measures could be enacted as early as August 7 if no deal is reached.

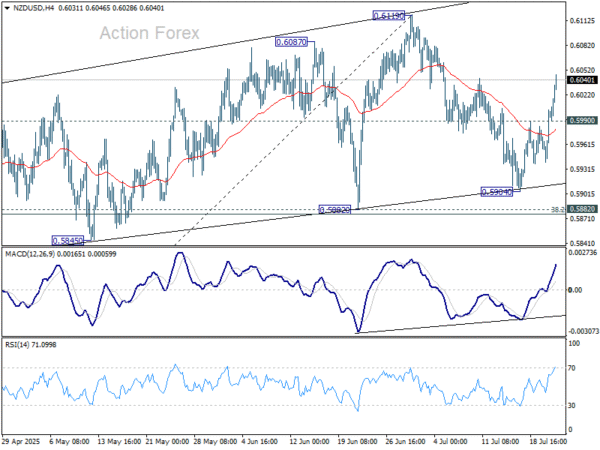

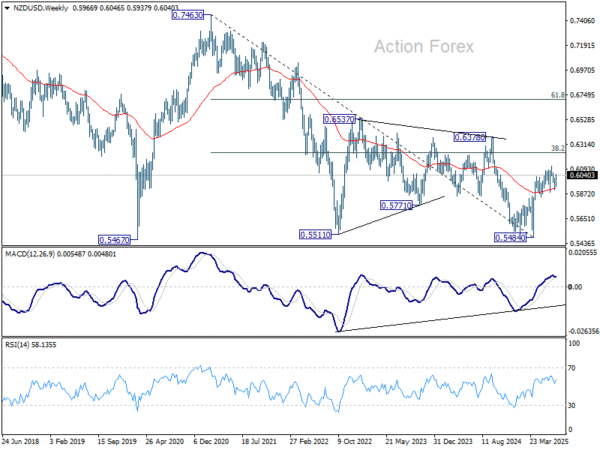

Technically, NZD/USD’s extended rebound and strong break of 55 4H EMA suggests that correction from 0.6119 has already completed at 0.5904 already. Further rise should now be seen to retest 0.6119 high first. Firm break there will resume whole rally from 0.5484. Next target is 38.2% retracement of 0.7463 to 0.5484 at 0.6240.

In Europe, at the time of writing, FTSE is up 0.49%. DAX is up 0.59%. CAC is up 1.11%. UK 10-year yield is up 0.043 at 4.618. Germany 10-year yield is up 0.019 at 2.611. Earlier in Asia, Nikkei rose 3.51%. Hong Kong HSI rose 1.62%. China Shanghai SSE rose 0.01%. Singapore Strait Times rose 0.55%. Japan 10-year JGB yield rose 0.09 to 1.597.

BoJ’s Uchida see moderate growth and temporarily sluggish inflation

BoJ Deputy Governor Shinichi Uchida said in a speech today that Japan’s economy is likely to “moderate” amid slowing global growth, with underlying inflation remaining “sluggish temporarily”. He added that downside risks dominate the outlook, particularly due to high uncertainty surrounding global trade policy and its spillover effects on both domestic and external demand.

Still, Uchida maintained that if the Bank’s baseline outlook holds, gradual rate hikes will continue. With real interest rates deeply negative, the BoJ is positioned to adjust its accommodative stance, but only as long as the economic and inflation path improves as expected.

He also highlighted the crosscurrents in Japan’s inflation profile—cost-push pressures from food remain elevated, while demand-side forces are weak. How businesses adjust wages and prices in response to these forces will be central to determining the sustainability of price growth.

Australia Westpac leading index falls to 0.03%, signals weak H2

Australia’s Westpac Leading Index slipped from 0.11% to just 0.03% in May, continuing a six-month slide that points to weakening momentum heading into the second half of 2025. The index, which provides a guide to economic activity three to nine months ahead, has lost altitude from 0.33% in December, with five of eight components dragging—particularly commodity prices, consumer sentiment, and hours worked.

Westpac noted that the shift from modestly above-trend growth to an “around trend” signal marks a clear step-down in economic momentum. The bank now expects the economy to expand by only 1.7% in 2025, a slight pickup from 1.3% in 2024, but still well below historical averages.

With the RBA set to meet on August 11–12, the Leading Index adds to the case for renewed policy easing. Westpac sees the June quarter CPI, due next week, as the key swing factor. A benign reading would likely clear the way for a 25bp cut in August, followed by another in November and two further cuts in H1 2026 as the central bank gradually loosens policy amid persistent growth headwinds.

AUD/USD Mid-Day Report

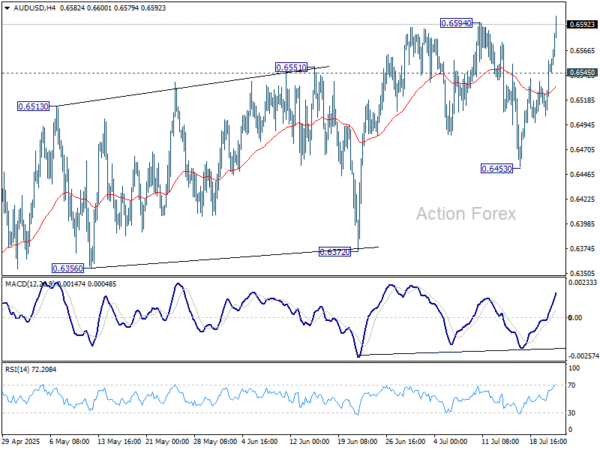

Daily Pivots: (S1) 0.6521; (P) 0.6539; (R1) 0.6575; More…

AUD/USD’s break of 0.6594 confirms resumption of whole rise form 0.5913. Intraday bias is back on the upside. Further rally should be seen to 0.6713 fibonacci level. On the downside, below 0.6545 minor support will turn intraday bias neutral again. But near term outlook will continue to stay bullish as long as 0.6453 support holds.

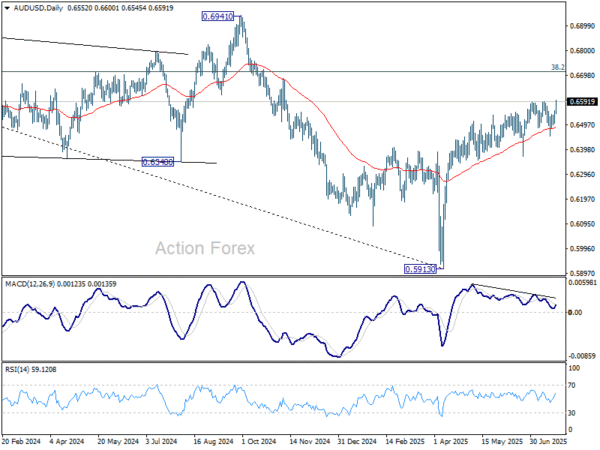

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).