Dollar remains broadly firm in early US session after a round of stronger-than-expected data reaffirmed the resilience of the US economy. However, gains are being capped as traders digest lingering political risks, including uncertainty over the status of Fed Chair Jerome Powell, and wait for further clarity from upcoming sentiment data. U.S. futures are flat, reflecting a more cautious tone across broader markets.

The Powell firing speculation has temporarily faded, following President Trump’s denial. Still, the issue could re-emerge at any moment, making it a latent risk for Dollar bulls. That’s prompting traders to hesitate before chasing the greenback higher despite the solid economic prints. Meanwhile, tomorrow’s University of Michigan consumer sentiment and inflation expectations data will be closely watched for signs of how Trump’s renewed tariff campaign is starting to impact consumers.

In FX rankings this week so far, Dollar is the top performer, followed by Loonie and Sterling. At the bottom end, Aussie has slumped following soft jobs data that prompted markets to price in a higher chance of an RBA rate cut in August. Kiwi and Swiss Franc are also underperforming, while Euro and Yen sit in the middle of the pack.

On the trade front, Japan is accelerating efforts to avoid a damaging 25% US tariff due to take effect August 1. Japan’s top trade negotiator Ryosei Akazawa spoke with U.S. Commerce Secretary Howard Lutnick today in a call described by Tokyo as substantive. Talks will continue, and Japan has reaffirmed its desire to strike a deal without compromising its core economic interests.

Japanese Prime Minister Ishiba is scheduled to meet U.S. Treasury Secretary Scott Bessent in Tokyo on Friday. The meeting will coincide with Bessent’s visit to Osaka for the national day at the World Expo. Akazawa will also attend and host the US delegation. Diplomatic channels are clearly active, but time is running short before tariffs take hold.

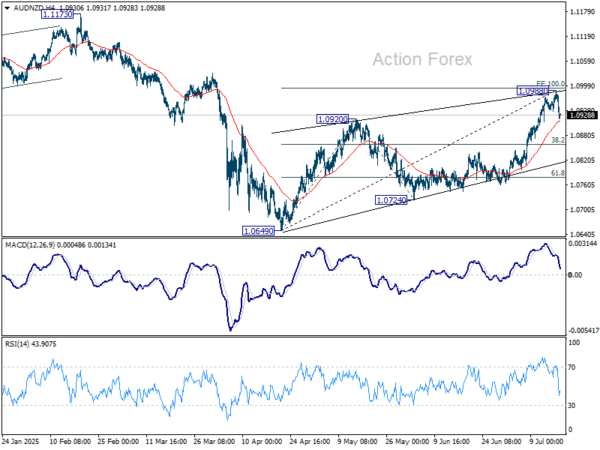

Technically, for AUD/NZD, focus is on 55 4H EMA (now at 1.0914) with today’s decline. Sustained break there should confirm short term topping at 1.0988, after missing 100% projection of 1.0649 to 1.0920 from 1.0724 at 1.0995. Deeper fall should then be seen to 38.2% retracement of 1.0649 to 1.0988 at 1.0859. Further break there will argue that rise from 1.0649 has completed as a three-wave corrective move.

In Europe, at the time of writing, FTSE is up 0.41%. DAX is up 1.08%. CAC is up 1.12%. UK 10-year yield is up 0.023 at 4.663. Germany 10-year yield is down -0.002 at 2.693. Earlier in Asia, Nikkei rose 0.60%. Hong Kong HSI fell -0.08%. China Shanghai SSE rose 0.37%. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield fell -0.017 to 1.559.

US retail sales rise 0.6% mom in June, ex-auto sales up 0.5% mom

US retail sales rose 0.6% mom to USD 7201.B in June, well above expectation of 0.2% mom. Ex-auto sales rose 0.5% mom to USD 583.3B, above expectation of 0.3% mom. Ex-gasoline sales rose 0.7% mom to USD 669.8B. Ex-auto& gasoline sales rose 0.6% mom to USD 533.0B. Total sales for the April through June period were up 4.1% from the same period a year ago.

US initial jobless claims fall to 221k vs exp 234k

US initial jobless claims fell -7k to 221k in the week ending July 12, below expectation of 234k. Four-week moving average of initial claims fell -6k to 230k. Continuing claims rose 2k to 1956k. Four-week moving average of continuing claims rose 5k to 1958k, highest since November 20, 2021.

Eurozone CPI finalized at 2% in June, services remain main driver

Eurozone CPI was finalized at 2.0% yoy in June, slightly higher than May’s 1.9% yoy. Core CPI (ex energy, food, alcohol & tobacco) held steady at 2.3% for the second straight month.

Services contributed the bulk of annual Eurozone inflation (+1.51 percentage points), followed by food, alcohol and tobacco (+0.59 pp). Energy continued to exert a mild drag, subtracting -0.25 pp.

At the broader EU level, CPI rose to 2.3% yoy from 2.2% yoy the prior month. Cyprus and France saw sub-1% inflation, while Eastern European nations led the upside—Romania at 5.8% and Estonia at 5.2%. Inflation rose in 22 out of 27 EU states.

UK payrolled employment slips again, wage growth slows further

UK payrolled employment fell by -41k in June, marking a second straight monthly contraction. Though May’s drop was revised to a milder -24k from an initial -109k, the overall picture still points to a softening labor market. Claimant count rose more than expected by 25.8k. Unemployment rate in the three months to May edged higher from 4.6% to 4.7%.

Wage growth also lost some momentum, with median monthly pay rising 5.6% yoy in June, down from May’s 5.7% yoy. Average earnings growth in the three months to May slowed to 5.0% both with and without bonuses, with the latter still slightly hotter than the 4.9% expected.

Aussie unemployment rate surges to 4.3% as full-time jobs slide

Australia’s June jobs report came in well short of expectations, with only a 2k increase in employment and a sharp divergence between full-time and part-time work. Full-time employment plunged by -38.2k while part-time roles rose 40.2k. Unemployment rate rose to 4.3%, defying forecasts for it to hold at 4.1%, while participation rate remained unchanged at 67.0%.

According to the ABS, the rise in joblessness was driven by a 34k increase in the number of unemployed Australians. ABS labor head Sean Crick added that full-time hours worked declined -1.3% in the month, suggesting further weakness ahead. Despite a marginal rise in total hours worked of 0.1% mom, the data add to signs that the labor market is losing momentum.

Japan auto exports to US plunge -26.7% yoy as carmakers cut prices

Japan logged a trade surplus of JPY 153B in June, with exports down -0.5% yoy and imports up 0.2% yoy. The most striking detail was a sharp -11.4% yoy drop in exports to the US, the steepest decline since February 2021. Imports from the US also fell, declining -2.0% yoy.

Automobile shipments to the US fell -26.7% by value, while auto parts (-15.5% yoy) and pharmaceuticals (-40.9% yoy) also saw double-digit drops. Still, a 3.4% yoy rise in car export volumes suggests Japanese automakers are slashing prices and absorbing costs to maintain market share.

On a seasonally adjusted basis, exports dipped -0.4% mom while imports fell -1.0%, leaving a JPY 235B trade deficit.

The report comes just weeks before a 25% reciprocal US tariff on Japanese goods takes effect on August 1. That is one percentage point higher than the 24% rate first announced on “Liberation Day” in April.

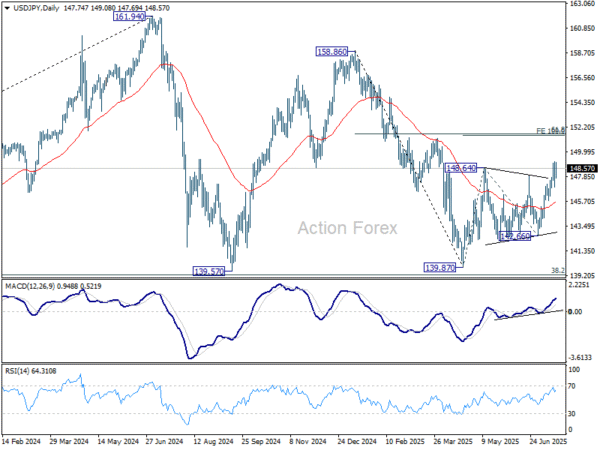

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.80; (P) 148.00; (R1) 149.08; More…

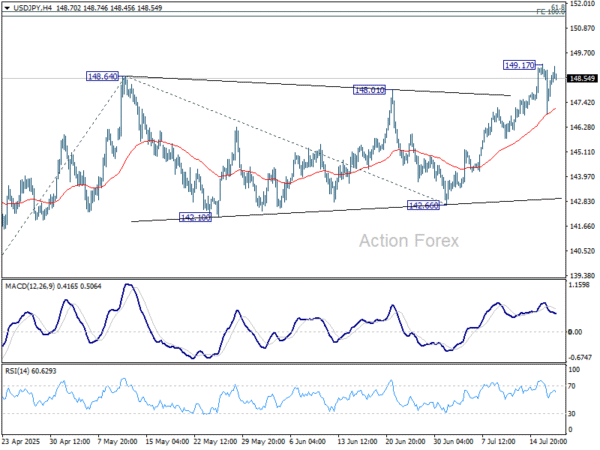

Intraday bias in USD/JPY stays neutral and more consolidations could be seen below 149.17. Downside should be contained by 55 D EMA (now at 145.56). Break of 149.17 will resume the whole rise from 139.87 to 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.