Aussie rallied sharply on Tuesday after RBA unexpectedly held its cash rate steady at 3.85%, defying widespread expectations for a 25bps cut. While a majority of economists had penciled in an easing move, the 6-3 vote revealed deep divisions within the Board. It’s unclear whether RBA’s decision was influenced at the last minute by escalating global trade risks. The US has begun sending formal letters to key trade partners with new tariff schedules, creating significant uncertainty for export-dependent economies like Australia. Yet, broader Asian markets appeared relatively calm. Equity indexes across the region posted modest gains

On the trade front, US President Donald Trump confirmed that 14 countries will face new blanket tariffs starting August 1. Signed letters detailed levies ranging from 25% to 40%. Trump’s executive order also pushed back the original July 9 deadline by three weeks, offering a narrow window for countries to negotiate bilateral deals.

The list of countries receiving tariff notices is sweeping and includes several key US trading partners: Japan, South Korea, Malaysia, Kazakhstan, South Africa, Laos, Myanmar, Tunisia, Bosnia and Herzegovina, Indonesia, Bangladesh, Serbia, Cambodia, and Thailand. The rates vary—25% for Japan, South Korea, Malaysia, Kazakhstan, and Tunisia; 30% for South Africa and Bosnia; 32% for Indonesia; 35% for Bangladesh and Serbia; 36% for Cambodia and Thailand; and 40% for Laos and Myanmar. The letters also warned that goods rerouted through third countries to evade tariffs would be penalized.

It’s surprising that close US allies Japan and South Korea are also at the center of the storm, now facing 25% tariffs. Japan confirmed receipt of a proposal offering a potential reprieve if negotiations proceed swiftly. Prime Minister Ishiba said revisions to the letter remain possible depending on Tokyo’s response. South Korea echoed a similar stance, viewing the delay as a chance to resolve tariff concerns amicably.

The European Union was excluded from the list of affected countries. EU sources confirmed no tariff letters were received, and the bloc remains focused on finalizing a deal by mid-week. European Commission President Ursula von der Leyen’s recent “good exchange” with Trump was cited as a positive sign, though officials remain divided over the depth of any agreement.

In FX markets, Aussie leads gains for the day so far, followed by Kiwi and Euro. Dollar lags behind, alongside Yen and Loonie. Sterling and the Swiss Franc are trading mid-pack.

In Asia, at the time of writing, Nikkei is up 0.23%. Hong Kong HSI is up 0.78%. China Shanghai SSE is up 0.58%. Singapore Strait Times is up 0.47%. Japan 10-year JGB yield is up 0.05 at 1.488. Overnight, DOW fell -0.94%. S&P 500 fell -0.79%. NASDAQ fell -0.92%. 10-year yield jumped 0.047 to 4.395.

RBA skips July cut, prefers to wait a little more for clarity

RBA held its cash rate target at 3.85%, opting not to deliver the widely expected 25bps cut. The decision, passed by a 6-3 majority, reflected cautious optimism as the central bank noted more balanced inflation risks and a still-resilient labor market. However, the Board stopped short of declaring victory on inflation and flagged considerable uncertainty in the domestic and global outlook.

In its statement, RBA said it could afford to “wait for a little more information” to ensure inflation is sustainably heading toward its 2.5% target. The Board remains concerned about both demand and supply-side uncertainty, particularly in light of volatile global trade policy. RBA stressed that monetary policy remains “well-positioned” to respond quickly if conditions deteriorate.

RBA also issued a measured warning on the risks stemming from U.S. tariffs and global trade policy shifts, noting that while extreme outcomes may be avoided, the uncertainty itself could weigh on demand. Financial markets have rebounded on hopes of compromise, but the RBA highlighted the risk that firms and households could delay spending amid the policy fog.

Australia’s NAB business confidence rises to 5, conditions rebound to 9

Australia’s business sentiment improved sharply in June, with NAB Business Confidence rising from 2 to 5, its highest trend level in over a year. Business Conditions surged from 0 to 9 after weakening for five straight months. The rebound was broad-based, with trading conditions jumping from 5 to 15, profitability returning to positive territory from -5 at 4, and employment conditions edging up from to 3.

On the pricing side, signals were mixed. Labour cost growth eased slightly from 1.6% to 1.5% (quarterly equivalent), while purchase costs rose from 1.2% to 1.5%. Final product price growth ticked up from 0.5% to 0.6%, although retail price growth slowed to 0.6%, hinting at easing consumer price pressures despite supply-side stickiness.

NAB’s Gareth Spence said the data suggest momentum may be picking up into the second half of 2025. “While we know the monthly survey can be volatile, the hope is at least some of these trends will be sustained,” he noted, calling the jump in both confidence and conditions a positive surprise amid ongoing global uncertainty.

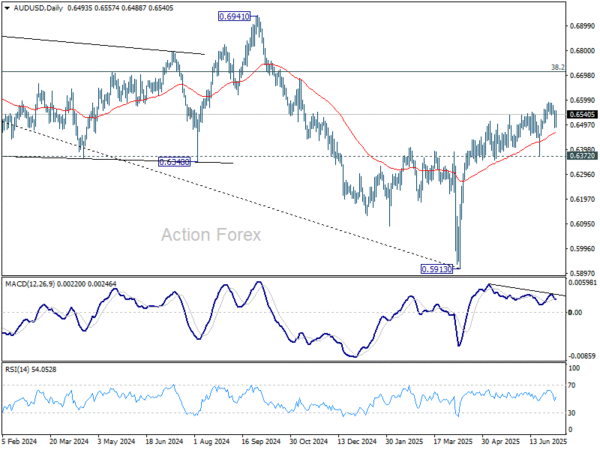

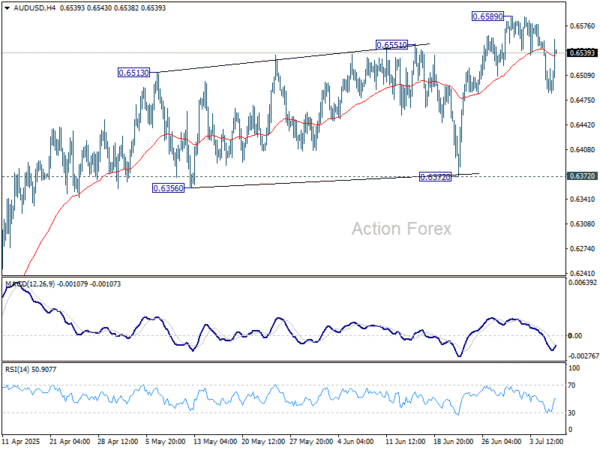

AUD/USD Daily Report

Daily Pivots: (S1) 0.6463; (P) 0.6513; (R1) 0.6541; More…

AUD/USD rebounded notably today but stays below 0.6589 resistance. Intraday bias stays neutral and more consolidations could still be seen. Overall, further rally is still expected as long as 0.6372 support holds. On the upside, firm break of 0.6589 will resume the rise from 0.5913 and target 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).