Risk appetite remains solid in Europe, with the FTSE 100 hitting a fresh record high as traders look through escalating US trade actions. US equity futures are holding steady too, and markets are showing little fear that the widening scope of tariffs will derail global growth. The upbeat mood comes despite US President Donald Trump’s latest tariff letters targeting 21 countries and a surprise 50% duty on Brazilian goods.

Mining stocks are leading the FTSE advance, bolstered by surging copper prices and rising US premiums amid Trump’s looming 50% copper tariff set to take effect August 1. The global copper market has entered a state of dislocation, and traders are scrambling to secure US-bound supply. That’s feeding optimism for producers, for the near term at least, and adding fuel to equity gains across Europe’s commodity-heavy indexes.

The rally also found support from upbeat signals out of China, where a reported rise in construction machinery sales is viewed as a positive sign for the country’s industrial sector. The data suggests that domestic infrastructure activity remains resilient, offering a degree of insulation to global supply chains despite mounting trade headwinds.

Sentiment in the UK has also been buoyed by the early trade agreement secured with the US, allowing Britain to avoid the steepest tariffs imposed elsewhere. While uncertainty persists for other major economies—especially those among the 21 recipients of Trump’s tariff letters—London’s relative insulation is helping drive capital inflows and stock outperformance.

In currency markets, Dollar continues to dominate, picking up momentum again as trading enters US session. Aussie is the second strongest for the week so far, supported by risk-on flows, firm commodity prices, and RBA’s surprise decision to hold rates earlier. Swiss Franc is the third strongest, suggesting some investors are hedging against lingering volatility. On the flip side, Yen remains the weakest, followed by Kiwi and Euro. Sterling and Loonie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.92%. DAX is up 0.03%. CAC is up 0.32%. UK 10-year yield is down -0.011 at 4.595. Germany 10-year yield is up 0.008 at 2.684. Earlier in Asia, Nikkei fell -0.44%. Hong Kong HSI rose 0.57%. China Shanghai SSE rose 0.48%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield fell -0.01 to 1.497.

US initial jobless claims fall to 227k, below expectation 236k

US initial jobless claims fell -5k to 227k in the week ending July 5, below expectation of 236k. Four-week moving average of initial claims fell -6k to 236k.

Continuing claims rose 10k to 1965k in the week ending June 28, highest since November 13, 2021. Four-week moving average of continuing claims rose 3.5k to 1955k, highest since November 20, 2021.

BoJ regional report highlights business uncertainty amid tariff risks

BoJ’s regional branch managers reported that while higher US tariffs have yet to significantly dent Japan’s exports or factory activity, companies are starting to hold back on capital expenditure.

Uncertainty over US trade policy, driven by President Trump’s rapid and unpredictable tariff announcements, has made it difficult for firms to fully assess the potential economic impact. While concrete damage has not yet materialized, the lack of clarity is beginning to influence strategic planning. “Many regions saw companies voice concern about slumping demand from rising US sales prices and a slowdown in the global economy,” BoJ said.

Wage developments are another key theme in the survey. The outlook is split: some companies foresee the need to raise wages to attract and retain talent, while others are already hinting at bonus cuts should profit margins come under pressure.

Japan’s PPI slows to 2.9% yoy in June, stronger Yen helps ease import costs

Japan’s Producer Price Index rose 2.9% yoy in June, easing from May’s 3.3% yoy pace and in line with expectations. The slowdown reflects a moderation in upstream price pressures, as firms begin to benefit from a firmer Yen.

Yen-based import price index dropped -12.3% yoy from a year earlier, deepening from May’s -10.3% yoy fall and signaling that Japan’s currency rebound is dampening raw material costs. Food and beverage prices remained elevated with a 4.5% yoy increase, largely due to persistently high rice costs, though that was slightly softer than the prior month’s 4.7% yoy rise.

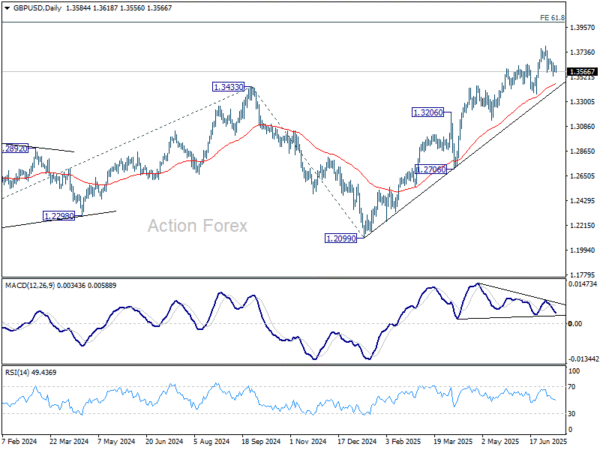

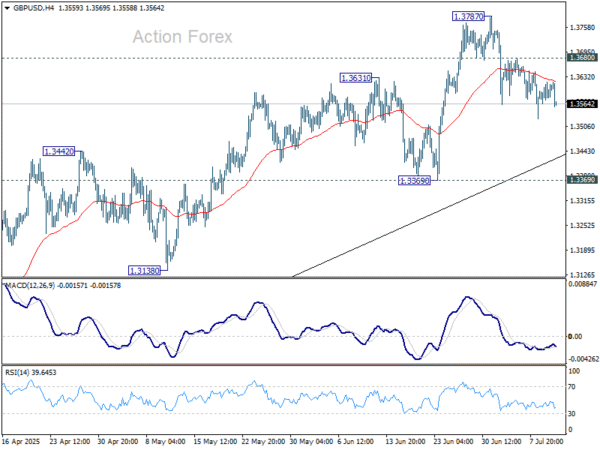

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3560; (P) 1.3590; (R1) 1.3616; More…

No change in GBP/USD’s outlook as corrective pullback from 1.3787 is still extending. Intraday bias stays neutral first. Downside is expected to be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.